Fillable Business Bill of Sale Document

Fillable Business Bill of Sale Document

When embarking on the journey of buying or selling a business, a critical document that serves as the cornerstone of the transaction is the Business Bill of Sale form. This essential piece of paperwork not only verifies the transfer of ownership but also outlines the specific terms and conditions of the sale. Detailing everything from the purchase price to the inventory included, and the responsibilities of each party involved, this form acts as a formal receipt as well. It's important for both buyers and sellers to understand the implications and requirements of this document, as it plays a pivotal role in ensuring the legality and smooth transition of the business. Crafting a comprehensive Business Bill of Sale form requires a clear understanding of what must be included to protect all parties involved and to comply with state laws. Notably, the form serves as a binding agreement once both parties sign, underscoring its importance in the transaction process.

Business Bill of Sale

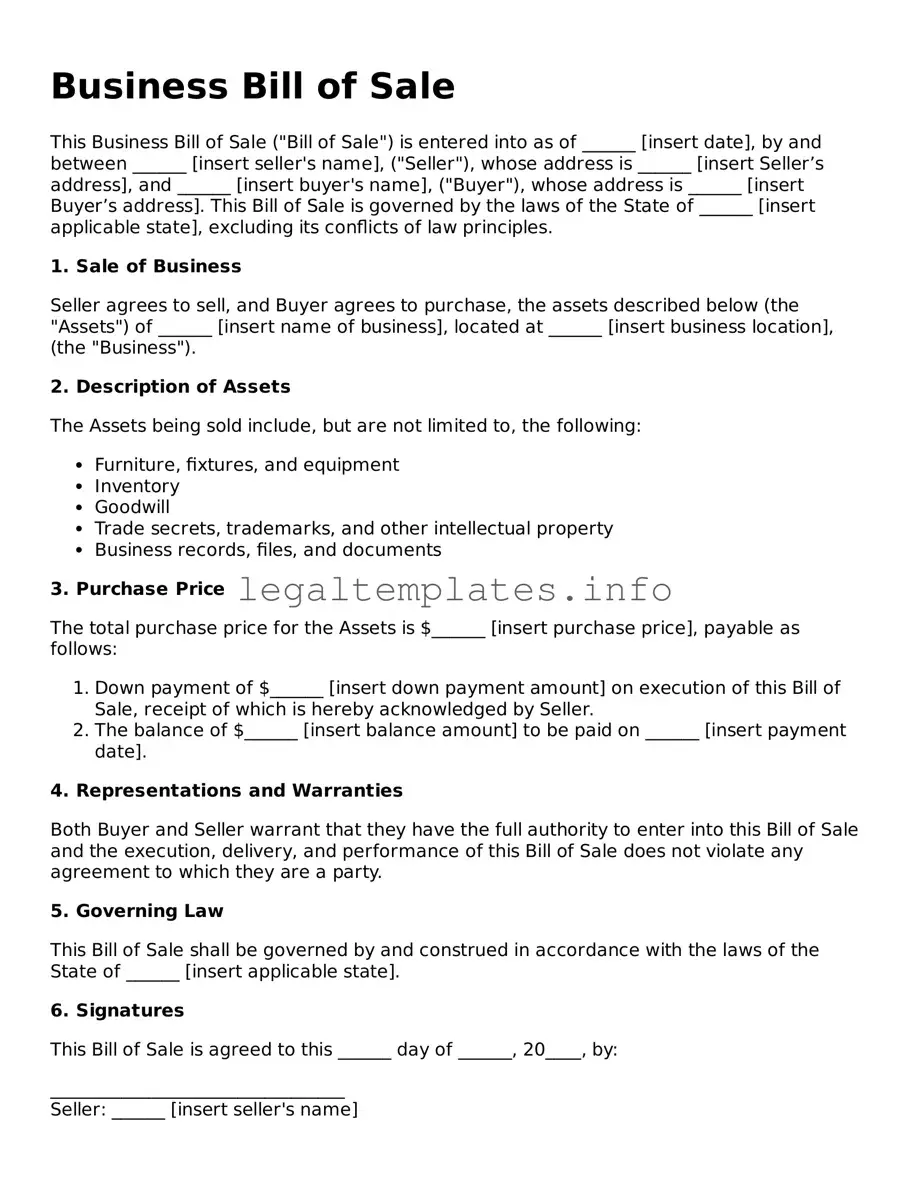

This Business Bill of Sale ("Bill of Sale") is entered into as of ______ [insert date], by and between ______ [insert seller's name], ("Seller"), whose address is ______ [insert Seller’s address], and ______ [insert buyer's name], ("Buyer"), whose address is ______ [insert Buyer’s address]. This Bill of Sale is governed by the laws of the State of ______ [insert applicable state], excluding its conflicts of law principles.

1. Sale of Business

Seller agrees to sell, and Buyer agrees to purchase, the assets described below (the "Assets") of ______ [insert name of business], located at ______ [insert business location], (the "Business").

2. Description of Assets

The Assets being sold include, but are not limited to, the following:

3. Purchase Price

The total purchase price for the Assets is $______ [insert purchase price], payable as follows:

4. Representations and Warranties

Both Buyer and Seller warrant that they have the full authority to enter into this Bill of Sale and the execution, delivery, and performance of this Bill of Sale does not violate any agreement to which they are a party.

5. Governing Law

This Bill of Sale shall be governed by and construed in accordance with the laws of the State of ______ [insert applicable state].

6. Signatures

This Bill of Sale is agreed to this ______ day of ______, 20____, by:

_________________________________

Seller: ______ [insert seller's name]

_________________________________

Buyer: ______ [insert buyer's name]

| Fact Name | Description |

|---|---|

| Purpose | The Business Bill of Sale form is used to document the transfer of ownership of a business from the seller to the buyer. |

| Components | It typically includes information such as the names of the buyer and seller, a description of the business being sold, the sale price, and the date of sale. |

| Significance | This form serves as a legal record of the transaction and can be used to settle disputes or discrepancies that may arise post-sale. |

| Governing Law | While generally governed by the Uniform Commercial Code (UCC) as adopted by most states, specific requirements can vary by state laws. |

Completing a Business Bill of Sale is straightforward when you know what to do next. This document is essential for both the seller and buyer, marking the official transfer of business ownership. It's a critical step in ensuring all parties have a clear record of the sale, detailing what was purchased, the sale price, and any other relevant terms. To fill out this form correctly, follow these steps, and make sure to have all the necessary information on hand.

Once the form is filled out, ensure that both parties receive a copy for their records. This document will serve as proof of the sale and transfer of ownership, so it's important to keep it safe and accessible. With these steps completed, the transaction is formally documented, providing clarity and protection for all involved.

What is a Business Bill of Sale?

A Business Bill of Sale is a document that serves as a formal agreement in the sale of a business between two parties, the seller and the buyer. It acts as evidence that the business' ownership has been transferred from the seller to the buyer and outlines the details of the transaction, including the sale price, a description of the assets being sold, and the date of sale.

Why is a Business Bill of Sale important?

This document is crucial because it legally documents the transfer of ownership. It protects both the buyer and the seller by specifying the terms and conditions of the sale, preventing misunderstandings or disputes. It can also be used for tax purposes, to obtain financing, or to register the sale with the relevant government agencies.

What information should be included in a Business Bill of Sale?

The document should include the names and contact information of the buyer and seller, a detailed description of the business being sold, the sale price, payment terms, any warranties or guarantees, and the date of sale. It may also include terms related to non-competition and confidentiality agreements.

Is a Business Bill of Sale the same as a purchase agreement?

No, they are not the same. A Business Bill of Sale is a record of the sale that confirms the transfer of ownership after the transaction has been completed. A purchase agreement is a contract that outlines the terms and conditions of the sale before it is finalized. The purchase agreement may include provisions that must be met for the sale to be completed.

Do I need a lawyer to draft a Business Bill of Sale?

While it's not legally required to have a lawyer draft a Business Bill of Sale, it is highly recommended. A lawyer can ensure that the document meets all legal requirements, accurately reflects the agreement between the buyer and seller, and addresses any specific issues related to the business sale. This can prevent legal problems down the road.

Can a Business Bill of Sale be used for selling part of a business?

Yes, a Business Bill of Sale can be used for selling a portion of a business. The document should specify exactly what part of the business is being sold, including any assets or interests. It’s crucial to clearly define the scope of the sale to prevent any misunderstandings or disputes.

What happens if a Business Bill of Sale is not used?

Not using a Business Bill of Sale can lead to serious risks, such as disputes over ownership, issues with the IRS, or problems with proving the legitimacy of the sale. Without this formal document, the buyer may have difficulty proving ownership or may face challenges in obtaining financing or insurance for the business.

Is a witness or notarization required for a Business Bill of Sale?

Requirements can vary by state, but generally, having a witness or notarization can add an extra layer of protection and authenticity to the document. It is advisable to check local laws or consult with a legal professional to understand the specific requirements in your state.

When filling out a Business Bill of Sale form, individuals often overlook the precise details required for accurate completion. One common mistake is not specifying the full legal names of both the buyer and the seller. This detail is crucial as it legally identifies the parties involved in the transaction. Without it, the document may not provide the legal protection or clarity needed should disputes arise.

Another frequent error is failing to adequately describe the business being sold. The description should include not only the name of the business but also any pertinent details such as its location, assets included in the sale, and the operational scope. Vague descriptions can lead to misunderstandings and potentially, legal complications if there is ambiguity regarding what was intended to be included in the sale.

Incorrect or incomplete financial information is also a significant pitfall. It is vital to clearly specify the sale price, payment terms, and any other financial arrangements such as a payment plan or escrow details. Errors or omissions in this area can result in disputes or delays in completing the sale. Additionally, it's important to outline any existing liabilities or obligations that will be assumed by the buyer.

Omitting the date of the sale is another common mistake. The effective date is crucial as it marks when the ownership officially changes hands and can also affect tax obligations. Without a clearly defined date, it may be difficult to enforce the terms of the sale or determine the responsibilities of each party.

Many individuals neglect to include warranties or representations made by the seller regarding the condition of the business. This section can protect the buyer by ensuring that they are aware of any issues or limitations of the business being purchased. Failing to document these representations can leave the buyer vulnerable to unanticipated problems.

Not specifying the governing law is a mistake that can lead to legal ambiguities. The Business Bill of Sale should indicate which state's laws will govern the document. This clarification can prove essential if legal issues arise, ensuring that both parties are aware of the jurisdiction that will interpret the document's terms.

A lack of signatures is a surprisingly common oversight. Both the buyer and the seller must sign the Business Bill of Sale for it to be legally binding. If the document is not properly signed, it may not be enforceable, potentially invalidating the sale.

Failing to acknowledge the importance of witnesses or notarization is another error. Depending on the jurisdiction, having the signatures witnessed or the document notarized can add an additional layer of authenticity and may be necessary for the document to be legally recognized.

Finally, individuals often forget to make and distribute copies of the Business Bill of Sale to all involved parties, including their legal counsel. Keeping a record is essential for tax purposes, future disputes, or simply for personal record-keeping. Without accessible copies, verifying the transaction's details could become challenging.

When transferring ownership of a business, the Business Bill of Sale form plays a crucial role. However, it rarely stands alone in the process. Other forms and documents are often required to ensure a smooth, legally sound transition. These documents can vary based on the nature of the business, the state in which it operates, and the specifics of the transaction. Below is a list of ten common documents that are typically used in conjunction with a Business Bill of Sale to safeguard the interests of both buyer and seller and to comply with legal requirements.

Collectively, these documents play a significant role in ensuring that all aspects of the business sale are properly documented and legally binding. They not only provide a record of the sale but also help to clarify the responsibilities and expectations of each party involved in the transaction. Ensuring that all necessary documents are in order can facilitate a smoother transition, help avoid misunderstandings, and provide protection for both parties. When in doubt, consulting with a legal expert can help navigate the complexities of business transfers and ensure that all legal requirements are met.

The Business Bill of Sale form shares similarities with the Asset Purchase Agreement, as both are used in the context of a sale and purchase transaction. However, an Asset Purchase Agreement is broader, detailing the sale and transfer of assets from one business to another, including tangible and intangible assets, liabilities, and sometimes even employees. The Business Bill of Sale is typically focused on the transfer of ownership for specific assets, serving as a receipt for the transaction.

Similar to the Warranty Deed in real estate transactions, the Business Bill of Sale provides assurances from the seller to the buyer regarding the ownership and status of the assets being sold. While a Warranty Deed guarantees clear title to real property, affirming there are no liens or encumbrances, the Business Bill of Sale reassures the buyer of the legitimate transfer of ownership for personal or business property, free from any undisclosed liabilities.

The Quitclaim Deed is another document that echoes the purpose of the Business Bill of Sale, but in the realm of real estate. Unlike the Business Bill of Sale, which transfers ownership of business assets with a guarantee of clear title, the Quitclaim Deed transfers property rights with no guarantees—simply transferring whatever interest the seller has in the property, if any. Both documents finalize the transfer of property, albeit with different levels of seller liability.

The Bill of Sale form, for personal property, is akin to the Business Bill of Sale but on a smaller scale. While the former often pertains to the sale of individual items, like a car or a boat, the latter encompasses a broader range of assets, potentially including an entire business. Both serve as legal evidence of a transaction, detailing the goods sold, the sale price, and the parties involved, providing proof of transfer and receipt of payment.

A Promissory Note also shares commonalities with the Business Bill of Sale, as both are integral in transactions involving valuable considerations. However, the Promissory Note is essentially a financial instrument, representing a written promise by one party to pay another a definite sum of money either on demand or at a future date. While the Business Bill of Sale confirms the transfer of goods or business assets, a Promissory Note involves the commitment to pay, thus facilitating transactions that may not be immediate cash exchanges.

The General Agreement is another document closely related to the Business Bill of Sale, as it can encompass various aspects of a business transaction. This document outlines the terms and conditions agreed upon by two parties, potentially including the sale of business assets. However, the General Agreement is more versatile, covering a range of agreements beyond the sale of assets, such as partnerships, nondisclosure terms, and more, making it broader in scope but less specific in function.

Like the Business Bill of Sale, the Sales and Purchase Agreement (SPA) is used in transactions involving the sale of goods or assets. However, the SPA is more comprehensive, often including detailed terms of the sale, warranties, indemnities, dispute resolution mechanisms, and conditions precedent that must be satisfied before the transaction can complete. It is applicable in both the sale of individual assets and whole businesses, making it a more detailed contract that governs the entirety of the transaction process.

A Receipt, in its most basic form, is similar to the Business Bill of Sale as it acknowledges the receipt of payment and serves as proof of a transaction. However, a Receipt is generally more simplistic, providing minimal details such as the amount paid and the date of payment. In contrast, the Business Bill of Sale contains more detailed information regarding the assets being transferred, the parties to the transaction, and any warranties or representations made by the seller.

The Loan Agreement shares a transactional kinship with the Business Bill of Sale but focuses on the terms under which one party lends money to another. The Loan Agreement details interest rates, repayment schedules, and the consequences of default, making it crucial for borrowing and lending money. Unlike the Business Bill of Sale, which finalizes the transfer of ownership for assets, a Loan Agreement governs the conditions under which financial assets are temporarily transferred.

Finally, an Employment Contract, while primarily focused on the conditions of employment between an employer and an employee, can occasionally intersect with the purposes of the Business Bill of Sale during business acquisition scenarios. It outlines roles, responsibilities, compensation, and confidentiality agreements but may require adjustments or renewals in the event of a business sale, especially if the business's assets, including contracts with key employees, are part of the sale. This demonstrates how even documents centered on human resources can relate to the transfer of business ownership.

When completing a Business Bill of Sale form, it's important to follow a set of dos and don'ts to ensure the document is accurate, legal, and binding. Below, find essential guidelines to consider:

Do:Ensure all parties' names are spelled correctly and match their legal identification. Mistakes can lead to questions about the document's validity.

Provide a detailed description of the business being sold, including assets, inventory, and any intellectual property. This clarity can prevent disputes over what is included in the sale.

Include the sale price and the payment method. Whether it’s a lump sum or installment payments, detailing the financial agreement helps safeguard against future misunderstandings.

List any warranties or representations being made about the business. Clear communication about the state of the business at the time of sale is crucial.

Have the document reviewed by a lawyer. Legal advice can prevent future legal issues by ensuring the document complies with local laws and is correctly executed.

Leave any blanks on the form. Unfilled sections can lead to confusion or manipulation of the document after signing.

Forget to get the document notarized, if required. Notarization adds a layer of verification and authenticity, making the document more legally sound.

Overlook the importance of obtaining signatures from all parties. Without the appropriate signatures, the document may be considered invalid.

Delay in making copies of the signed document for all parties. Everyone involved should have a copy for their records to ensure transparency and future reference.

Regarding the Business Bill of Sale form, there are common misconceptions that need clarification. This document plays a crucial role in the sale of a business, serving as a record that the transaction occurred and detailing the specifics of what was bought and sold. Understanding its importance and how it functions can help prevent potential issues down the line.

Misconception #1: It's Only Necessary for Large Transactions. Many people believe that a Business Bill of Sale form is only necessary for large, high-value transactions. However, it's crucial for all sizes of transactions to ensure clarity and legal proof of the sale, protecting both buyer and seller.

Misconception #2: It's the Same as a Receipt. Though it may serve a similar function as a receipt, showing proof of purchase, a Business Bill of Sale contains more detailed information about the sale, including warranties and the specifics of what's being transferred, beyond just the price.

Misconception #3: It's Legally Binding Immediately upon Signing. While signing the document is a critical step, certain jurisdictions may require additional steps, such as notarization or registration, to make it fully legally binding.

Misconception #4: Any Template Will Do. It's essential to use a template that is comprehensive and tailored to the specifics of your transaction. Generic templates might not cover all legal bases or include necessary details, which can lead to disputes.

Misconception #5: It's Only Concerned with Physical Assets. A Business Bill of Sale can also encompass intangible assets, like intellectual property and goodwill, not just physical items like equipment or inventory.

Misconception #6: It Must Be Filed with the Government. While it's a critical document, not all jurisdictions require a Business Bill of Sale to be filed with the government. Nevertheless, it's important to retain it for records and possibly for tax purposes.

Misconception #7: It Transfers Liability. A Business Bill of Sale transfers ownership of assets, but not necessarily any existing liabilities or debts associated with the business, unless explicitly stated.

Misconception #8: Only the Buyer Needs a Copy. Both the buyer and the seller should retain a copy of the Business Bill of Sale. It protects both parties and serves as proof of transfer and terms of sale, important for both legal and tax considerations.

It's vital to approach the creation and execution of a Business Bill of Sale with care and attention to detail, ensuring it accurately reflects the transaction and complies with relevant laws. By understanding and addressing these common misconceptions, both parties can help safeguard their interests and ensure a smoother transaction process.

When transferring ownership of assets in a business transaction, a Business Bill of Sale form plays a pivotal role. Its proper completion and usage ensure a smooth and legally sound transfer of assets from seller to buyer. Here are key takeaways to consider:

Ultimately, a well-prepared Business Bill of Sale safeguards the interests of both buyer and seller, serving as a definitive record of the transaction and the transfer of ownership. It`s a key component of the business sale process that cannot be overlooked.

Golf Cart Title - It ensures that all the necessary legal steps are followed in the transfer of the golf cart, aligning with state regulations.