Fill a Valid Broker Price Opinion Form

Fill a Valid Broker Price Opinion Form

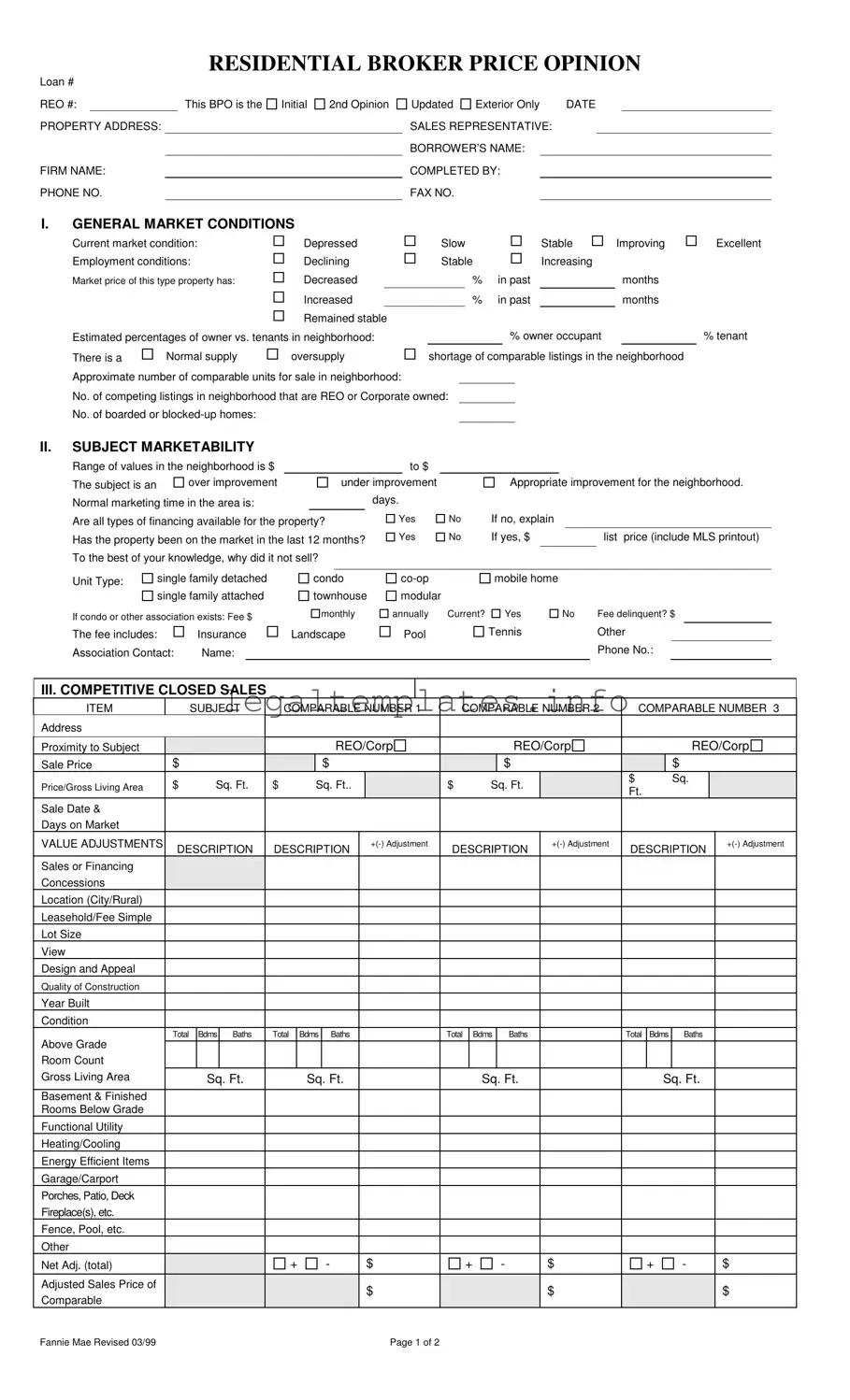

In the realm of residential real estate assessments, the Broker Price Opinion (BPO) form emerges as a pivotal document, bridging the gap between comprehensive appraisals and the immediate market insights that only real estate professionals can provide. Tailored for a myriad of scenarios such as loan origination, REO (Real Estate Owned) evaluations, or when a quick, informed estimate is necessary, the form encompasses an array of critical components. It commences by capturing the essence of the property in question, detailing its address, the involved firm, and the contact information of both the sales representative and the individual completing the form. A thorough investigation follows, dissecting current market conditions, employment trends, and a comparative analysis of homeowners versus tenants in the neighborhood, offering a nuanced understanding of the property's positioning within its local milieu. The form delves deeper, evaluating the subject's marketability, from its comparative value within the neighborhood to the intricacies of its financing availability, thereby laying the groundwork for an informed pricing strategy. Beyond market analysis, the BPO also demands a comprehensive competitive review, juxtaposing the subject property against similar sold and listed properties to deduce a nuanced value adjustment. This adjustment considers a myriad of factors ranging from sales concessions to the physical attributes of the properties compared. Lastly, the form transitions into strategizing the marketing approach, outlining necessary repairs to enhance marketability, and concluding with a valuation section that crystallizes the property's market value, completing a holistic overview essential for lenders, investors, and homeowners alike.

RESIDENTIAL BROKER PRICE OPINION

Loan #

REO #:This BPO is the

PROPERTY ADDRESS:

FIRM NAME:

PHONE NO.

Initial

2nd Opinion

Updated Exterior Only |

DATE |

|||

SALES REPRESENTATIVE: |

|

|

|

|

BORROWER’S NAME: |

|

|

|

|

COMPLETED BY: |

|

|

|

|

FAX NO. |

|

|

|

|

I.GENERAL MARKET CONDITIONS

Current market condition: |

Depressed |

Slow |

|

Stable |

Improving |

||

Employment conditions: |

Declining |

Stable |

|

Increasing |

|

||

Market price of this type property has: |

Decreased |

|

|

% |

in past |

|

months |

|

Increased |

|

|

% |

in past |

|

months |

|

Remained stable |

|

|

|

|

|

|

Estimated percentages of owner vs. tenants in neighborhood: |

|

|

% owner occupant |

|

|||

There is a |

Normal supply |

oversupply |

shortage of comparable listings in the neighborhood |

||||

Approximate number of comparable units for sale in neighborhood: |

|

|

|

|

|

||

No. of competing listings in neighborhood that are REO or Corporate owned:

No. of boarded or

Excellent

% tenant

II.SUBJECT MARKETABILITY

Range of values in the neighborhood is $ |

|

|

|

|

|

to $ |

|

|

|

|

|

|

|

|

The subject is an |

over improvement |

|

|

under improvement |

|

Appropriate improvement for the neighborhood. |

||||||||

Normal marketing time in the area is: |

|

|

|

|

days. |

|

|

|

|

|

|

|||

Are all types of financing available for the property? |

Yes |

No |

If no, explain |

|

|

|

||||||||

Has the property been on the market in the last 12 months? |

Yes |

No |

If yes, $ |

|

|

list price (include MLS printout) |

||||||||

To the best of your knowledge, why did it not sell? |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||||

Unit Type: |

single family detached |

|

condo |

|

mobile home |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

single family attached |

|

townhouse |

modular |

|

|

|

|

|

|

||||

If condo or other association exists: Fee $

monthly

annually Current?

Yes

No |

Fee delinquent? $ |

The fee includes:

Association Contact:

Insurance

Name:

Landscape

Pool

Tennis |

Other |

|

Phone No.: |

III. COMPETITIVE CLOSED SALES

ITEM |

|

|

SUBJECT |

|

COMPARABLE NUMBER 1 |

|

COMPARABLE NUMBER 2 |

|

COMPARABLE NUMBER 3 |

|||||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

||||||||

Sale Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|||

Price/Gross Living Area |

$ |

|

Sq. Ft. |

$ |

|

Sq. Ft.. |

|

|

$ |

|

|

Sq. Ft. |

|

|

$ |

|

|

|

Sq. |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

Ft. |

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Sale Date & |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

|

DESCRIPTION |

|

|

DESCRIPTION |

|

DESCRIPTION |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

Bdms |

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|

Total |

|

Bdms |

|

Baths |

|

|

Total |

Bdms |

Baths |

|

|

|

||||||

Above Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

Sq. Ft. |

|

|

Sq. Ft. |

|

|

|

|

|

|

Sq. Ft. |

|

|

|

|

|

Sq. Ft. |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Adj. (total) |

|

|

|

|

|

+ |

- |

|

|

$ |

|

+ |

- |

|

$ |

|

+ |

|

|

- |

|

$ |

|

|||||||||

Adjusted Sales Price of |

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fannie Mae Revised 03/99 |

|

|

|

|

|

|

|

|

|

|

|

|

Page 1 of 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REO# |

Loan # |

IV. MARKETING STRATEGY

Minimal Lender Required Repairs |

V. REPAIRS

Occupancy Status: Occupied

Repaired Most Likely Buyer:

Vacant

Unknown

Unknown

Owner occupant

Investor

Investor

Itemize ALL repairs needed to bring property from its present “as is” condition to average marketable condition for the neighborhood. Check those repairs you recommend that we perform for most successful marketing of the property.

$

$

$

$

$

$

$

$

$

$

|

|

|

|

GRAND TOTAL FOR ALL REPAIRS $ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. COMPETITIVE LISTINGS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

ITEM |

|

|

SUBJECT |

COMPARABLE NUMBER 1 |

COMPARABLE NUMBER. 2 |

COMPARABLE NUMBER. 3 |

||||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

|

|

REO/Corp |

|||||||||||||

List Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

||

Price/Gross Living Area |

$ |

|

Sq.Ft. |

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

|||||||||||

Data and/or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Verification Sources |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

DESCRIPTION |

|

+ |

DESCRIPTION |

|

DESCRIPTION |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Above Grade |

Total |

Bdms |

Baths |

Total |

Bdms |

Baths |

|

|

|

Total |

Bdms |

|

Baths |

|

Total |

Bdms |

|

Baths |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

Sq. Ft. |

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

||||||||||||||

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Net Adj. (total) |

|

|

|

|

+ |

- |

|

|

|

$ |

|

|

+ |

- |

- |

|

$ |

|

|

+ |

- |

|

$ |

|

|

|

||

Adjusted Sales Price |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

of Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. THE MARKET VALUE (The value must fall within the indicated value of the Competitive Closed Sales).

Market Value |

Suggested List Price |

AS IS REPAIRED

30 Quick Sale Value

Last Sale of Subject, Price |

Date |

COMMENTS (Include specific positives/negatives, special concerns, encroachments, easements, water rights, environmental concerns, flood zones, etc. Attach addendum if additional space is needed.)

Signature: |

|

Date: |

Fannie Mae Revised 03/99 |

Page 2 of 2 |

CMS Publishing Company 1 800 |

| Fact Name | Detail |

|---|---|

| Purpose of Form | Used to give an opinion on the property's market value |

| Type of Properties Assessed | Includes a range from single family homes to condos and co-ops |

| Market Conditions Assessment | Evaluates current market and employment conditions, and neighborhood occupancy rates |

| Marketability and Improvements | Assesses whether the subject property is an appropriate, over, or under improvement within its neighborhood |

| Financing Availability | Indicates if all types of financing are available for the property |

| Competitive Market Analysis | Includes comparison with similar recently sold properties and adjustments for differences |

| Repairs and Marketing Strategy | Outlines necessary repairs and suggests strategies for marketing the property |

| Governing Law(s) | Based on Fannie Mae guidelines (Revised 03/99) |

Filling out a Broker Price Opinion (BPO) form is a structured process that requires attention to detail and an understanding of the property in question. This form is instrumental for professionals in assessing the value of a residential property. Each section is designed to capture specific details about the property's market conditions, marketability, competitive listings, and overall value. Following the steps below will ensure a comprehensive evaluation and enable informed decision-making.

Completing the Broker Price Opinion form requires a thorough analysis and understanding of the property and its surrounding market. By methodically addressing each section, professionals can provide a comprehensive and accurate assessment, which is crucial for decision-making processes.

What is a Broker Price Opinion (BPO) and when is it used?

A Broker Price Opinion (BPO) is an evaluation of a property's market value performed by a real estate broker or agent. It provides an estimate of the price for which a property might sell under current market conditions. BPOs are commonly used by banks, mortgage lenders, and financial institutions to assess the value of a property in situations such as loan originations, refinancing, or in foreclosure and REO (Real Estate Owned) transactions. They are often seen as a cost-effective alternative to a formal appraisal.

How is the market value of a property determined in a BPO?

In a BPO, the market value of a property is determined through a combination of methods. The broker or agent conducting the BPO reviews current market conditions, including employment and general economic conditions, and compares the subject property to similar, recently sold homes in the area, known as comparables or comps. Adjustments are made for differences between the subject property and comps, such as location, size, and condition. The BPO form also considers the rate of properties' prices increasing or decreasing in the area, the estimated percentage of owner-occupied homes, and the supply and demand for comparable listings.

What types of repairs and improvements are considered in the BPO form?

The BPO form includes an assessment of the property's condition and itemizes repairs needed to bring it to an average marketable condition for the neighborhood. This includes both cosmetic improvements and necessary repairs to address any defects or damages. The broker or agent recommends repairs that could enhance the property's marketability, thereby potentially increasing its value or reducing its time on the market. The form lists specific reparative actions, associated costs, and identifies the repairs recommended for the most successful marketing of the property.

How does a BPO address financing availability for a property?

The BPO form investigates and documents the availability of financing for the property in question. Availability of financing can significantly impact a property's marketability and, consequently, its value. The form specifically inquires whether all types of financing are available for the property, which is crucial information for potential buyers. If some financing options are not available, the reasons are explored and documented. This component of the BPO can influence the suggested listing price and marketing strategy for the property.

Filling out a Broker Price Opinion (BPO) form requires attention to detail and an understanding of the property market. However, errors can occur which might affect the accuracy of the valuation. One common mistake is the inaccurate assessment of general market conditions. Individuals often overlook or misinterpret local market trends such as changes in employment conditions, supply and demand dynamics, and the percentage of owner-occupied versus tenant-occupied homes. These elements are crucial for setting the context of the valuation.

Another error involves incorrect evaluation of the subject property's marketability. Specifically, whether a property is considered an over improvement or under improvement in comparison to others in the neighborhood can significantly influence its perceived value. Additionally, estimations regarding the typical time on the market for similar properties, and the availability of various types of financing for potential buyers, must be precise to ensure a realistic valuation.

Thirdly, incorrectly filling out the competitive closed sales section can lead to a skewed valuation. This section demands accurate comparison of the subject property against others that have recently sold in the area, requiring careful adjustment for differences in factors such as sale price, location, property size, and condition. Neglecting to make these adjustments accurately can result in an unreliable final valuation.

A fourth mistake is failing to adequately assess and list necessary repairs and their costs. Whether a property is occupied, vacant, or in a state of disrepair affects its appeal to potential buyers and its market value. Overlooking significant repairs or underestimating their costs can lead to unrealistic expectations about the property's marketable condition and value.

Fifth, inaccuracies in the competitive listings section can also lead to errors in valuation. This requires a current and detailed understanding of similar properties on the market, including their listing price and how long they have been for sale. Incorrect or outdated data in this section undermines the valuation's relevance and accuracy.

Sixth, the valuation adjustment section is another area prone to error. This part of the form requires making adjustments to the comparable sales prices based on differences between the subject property and each comparable sale. Misjudging the impact of these differences can either inflate or deflate the perceived value of the property.

Seventh, participants often neglect to provide a comprehensive analysis in the comments section. This section is critical for noting any factors that might affect the property's value that aren't covered elsewhere on the form, such as legal issues, environmental concerns, and rights or restrictions associated with the property. Omitting these details can lead to a valuation that does not fully reflect the property’s unique characteristics and constraints.

Lastly, failing to suggest a realistic marketing strategy and list price, based on an accurate assessment of the property’s as-is and repaired values, is a common oversight. This information is essential for lenders or investors who rely on the BPO for making informed decisions regarding the property. Without a viable marketing approach and a reasonable list price, the BPO's utility is significantly diminished.

When completing a Broker Price Opinion (BPO), professionals often need additional information to ensure accuracy and completeness. This necessitates the inclusion of various other forms and documents that complement the BPO by providing detailed insights or clarifications about the property and market conditions. Understanding these supplementary documents can enhance the reliability of the BPO.

Together, these documents provide a comprehensive overview of the property and help ensure that the Broker Price Opinion reflects the true value and condition of the property. They are essential tools for anyone involved in real estate transactions, offering critical insights beyond what is visible on the surface.

The Comparative Market Analysis (CMA) is similar to the Broker Price Opinion (BPO) form as both provide an estimate of a property's value based on current market conditions. Like the BPO, the CMA compares the subject property to similar properties in the area that have recently been sold, are currently on the market, or were on the market but did not sell. This comparison helps in understanding what potential buyers might be willing to pay for a property. Both documents are essential for setting a competitive and fair market price.

Appraisal Reports share similarities with the BPO form by evaluating a property's market value through detailed inspections and comparisons to similar properties. An appraiser conducts an on-site visit to examine the property's condition and then assesses its value by considering several factors, such as location, condition, and sales of comparable homes in the area. However, unlike BPOs, which are often performed by real estate agents, appraisals can only be conducted by licensed professionals.

The Property Condition Report highlights a property's physical state, similarly to how the BPO form includes a section for repairs needed to bring the property to marketable condition. This report provides detailed information about the property's structure, systems, and components, identifying any defects or maintenance issues. Both documents serve as critical tools for potential investors or buyers to understand the condition of the property before making decisions.

An Inspection Report, much like the BPO's section on property condition and needed repairs, identifies any issues with the property that could affect its value. Conducted by a professional home inspector, this report covers the property's major systems and structural components. Buyers often use this report to renegotiate the purchase price or request repairs based on the findings, making it an influential document in the buying process.

The Home Equity Report is somewhat similar to the BPO in that it determines the current value of a property for a homeowner interested in assessing their equity or considering a home equity loan or line of credit. This report takes into account recent market trends and comparable sales, helping homeowners understand how much of their mortgage has been paid off relative to the market value of their home.

Listing Agreements incorporate key elements found in the BPO form, such as property details and recommended listing price, forming a contract between a property owner and a real estate agent. This agreement authorizes the agent to list, market, and sell the property on behalf of the owner. The agreed-upon price is often informed by a BPO or similar market analysis to ensure the listing price is competitive within the current market.

The Pre-listing Package, similar to the BPO, contains comprehensive information about a property and its market conditions aimed at potential sellers. It often includes a comparative market analysis, marketing strategy, and suggested listing price, helping sellers make informed decisions about listing their property. This package ensures that sellers have all necessary information to enter the market confidently.

The Purchase Agreement, while primarily a legal document outlining the terms and conditions of a property sale, sometimes reflects the valuation found in a BPO, especially in terms of the agreed selling price. This agreement signifies the buyer's intent to purchase the property at a specified price, which ideally aligns with the current market value as determined by the BPO or a similar valuation tool.

Loan Servicing Reports can resemble the BPO form in the context of assessing a property’s value during mortgage servicing activities such as mortgage refinancing or loan modifications. These reports often require an up-to-date valuation of the property to ensure the modified loan values are in alignment with the property's current market value, safeguarding the interests of both the lender and borrower.

Finally, the Real Estate Owned (REO) Property Report, like the BPO, assesses the value of bank-owned properties that failed to sell at foreclosure auctions. These reports focus on determining the best possible price to list these properties on the market, considering their condition and local market conditions. Banks often use BPOs to inform the pricing strategy for REO properties, aiming to recuperate as much of the unpaid loan balance as possible.

When it comes to completing the Broker Price Opinion (BPO) form, accuracy and attention to detail are paramount. This document plays a crucial role in the real estate valuation process, and as such, requires a careful approach. To navigate this task effectively, here are six do's and don'ts to keep in mind:

Do:By following these guidelines, you'll be better equipped to complete the Broker Price Opinion form with accuracy and integrity, ultimately contributing to a smoother real estate transaction process.

There are several misconceptions about the Broker Price Opinion (BPO) form that often lead to confusion among those not familiar with real estate valuation processes. Understanding these misconceptions can help clarify the purpose and the limitations of a BPO.

By understanding these misconceptions, individuals can better appreciate the role and scope of Broker Price Opinions in real estate transactions and the valuation process. It’s crucial to recognize the specific context in which a BPO is being used to assess its impact accurately.

Filling out a Broker Price Opinion (BPO) form requires detailed attention to various aspects of the property and market conditions to ensure an accurate assessment of the property's value. Here are four key takeaways that are essential when working with a BPO form:

Effectively utilizing the BPO form involves a meticulous assessment of the property within its market context, analyzing comparable sales and current listings, and evaluating the property's physical condition and repair needs. By collecting and synthesizing this information, the form aids in establishing a well-informed opinion of the property's value.

Downloadable Free Printable Spanish Job Application Form - The form asks candidates if there are any days they are unavailable to work and to provide details if applicable.

Army Sworn Statement Form - It contains safeguards for integrity, including witness signatures and oaths administered by authorized individuals.