Fill a Valid Business Credit Application Form

Fill a Valid Business Credit Application Form

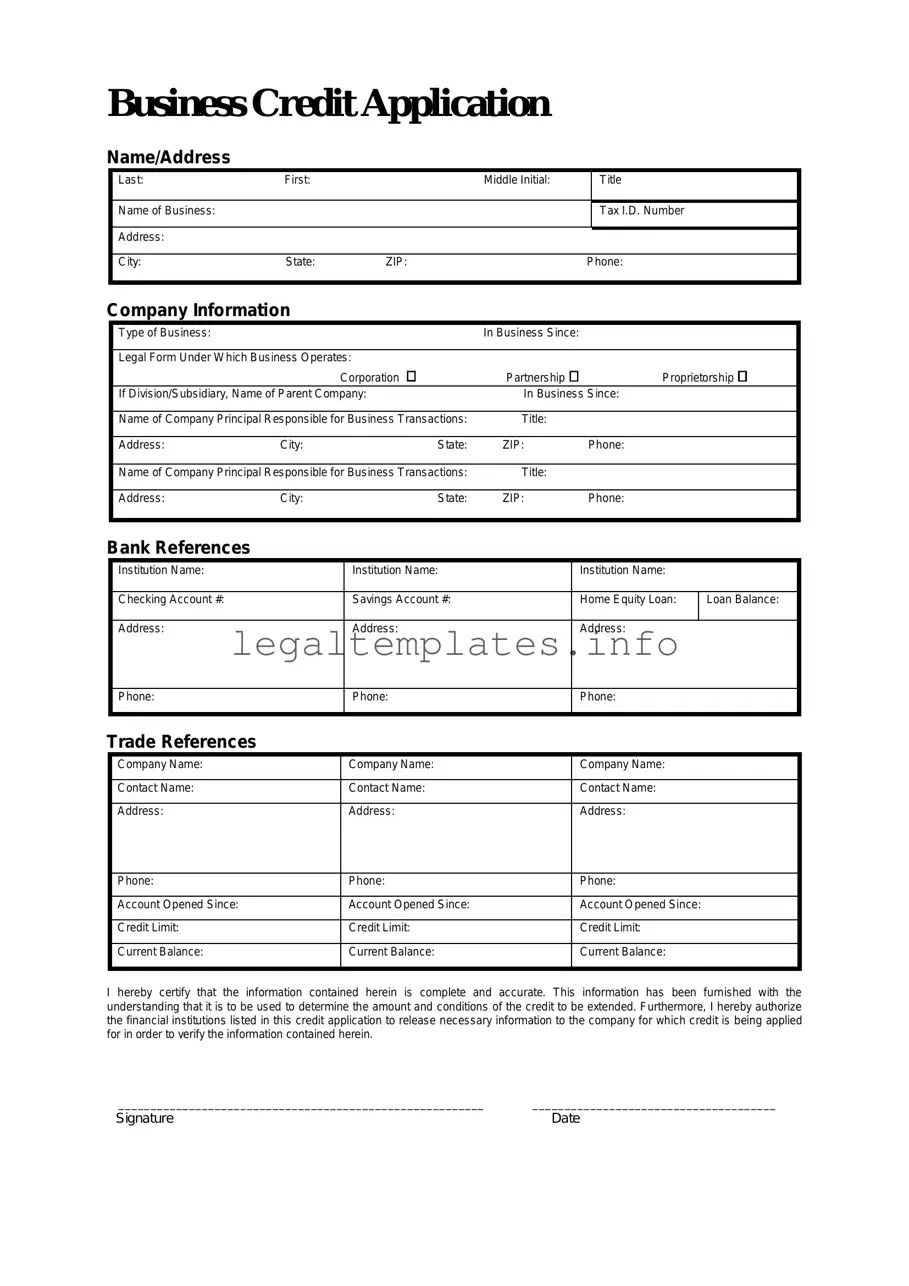

In the world of commerce and finance, the Business Credit Application form plays a pivotal role in facilitating the extension of credit from lenders to businesses. This document, meticulously crafted, encompasses a broad array of information critical for credit assessment. It serves as the foundation upon which lenders evaluate the creditworthiness of a business, scrutinizing details ranging from basic identification of the business, such as name and address, to more intricate financial data including credit references and financial statements. Furthermore, the form often entails a section dedicated to the terms and conditions of the credit agreement, setting clear expectations for both the lender and borrower. This enables businesses to access the requisite funds for growth and operational needs, while providing lenders with a structured approach to assess risk. Through the careful collection and analysis of the information provided in the Business Credit Application form, lenders are able to make informed decisions, underpinning the financial dynamics of lender-borrower relationships in the business landscape.

Business Credit Application

Name/Address

Last: |

First: |

|

Middle Initial: |

|

Title |

|

|

|

|

|

|

Name of Business: |

|

|

|

|

Tax I.D. Number |

|

|

|

|

|

|

Address: |

|

|

|

|

|

|

|

|

|

|

|

City: |

State: |

ZIP: |

|

Phone: |

|

|

|

|

|

|

|

Company Information

|

Type of Business: |

|

|

|

In Business Since: |

|

|

|

|

|

|

|

|

|

|

||

|

Legal Form Under Which Business Operates: |

|

|

|

|

|||

|

|

|

Corporation |

Partnership |

Proprietorship |

|

||

|

If Division/Subsidiary, Name of Parent Company: |

In Business Since: |

|

|||||

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

|

|

Bank References |

|

|

|

|

|

|

|

|

|

Institution Name: |

|

|

Institution Name: |

|

Institution Name: |

||

|

|

|

|

|

|

|

|

|

|

Checking Account #: |

|

|

Savings Account #: |

|

Home Equity Loan: |

ILoan Balance: |

|

|

Address: |

|

|

Address: |

|

Address: |

|

|

Phone:

Phone:

Phone:

Trade References

Company Name: |

Company Name: |

Company Name: |

|

|

|

Contact Name: |

Contact Name: |

Contact Name: |

|

|

|

Address: |

Address: |

Address: |

|

|

|

Phone: |

Phone: |

Phone: |

|

|

|

Account Opened Since: |

Account Opened Since: |

Account Opened Since: |

|

|

|

Credit Limit: |

Credit Limit: |

Credit Limit: |

|

|

|

Current Balance: |

Current Balance: |

Current Balance: |

|

|

|

I hereby certify that the information contained herein is complete and accurate. This information has been furnished with the understanding that it is to be used to determine the amount and conditions of the credit to be extended. Furthermore, I hereby authorize the financial institutions listed in this credit application to release necessary information to the company for which credit is being applied for in order to verify the information contained herein.

_________________________________________________________ ______________________________________

Signature |

Date |

| Fact Number | Fact Detail |

|---|---|

| 1 | A Business Credit Application is used by businesses to request credit from other businesses or lenders. |

| 2 | It typically includes the requesting company's business details, such as legal name, address, and type of business entity. |

| 3 | The form usually asks for the names and details of the principals or owners of the business. |

| 4 | Financial information, including bank references and trade references, are often required to assess creditworthiness. |

| 5 | Credit terms such as payment terms, credit limit requested, and interest rates are typically specified in the application. |

| 6 | The application may include a section for personal guarantees by the business owners, especially in smaller or newer businesses. |

| 7 | State-specific laws may govern the application process, including the information that must be disclosed and the manner of evaluation. |

| 8 | Submitting a Business Credit Application often authorizes the lender to perform a credit check on the business and its principals. |

| 9 | Approval or rejection of the application is based on the lender's assessment of the business's creditworthiness and financial stability. |

Filling out a Business Credit Application is a critical step for businesses seeking credit from suppliers or lenders. This procedure involves providing detailed information about the business, its financial health, and its owners or principals. A well-prepared application can streamline the approval process, enabling businesses to secure the credit they need for operations and growth. Below is a guide on how to complete the form properly.

Once the Business Credit Application form is filled out completely and accurately, it should be submitted according to the instructions provided by the credit issuer. This might include mailing, faxing, or submitting the information through an online portal. After submission, the next steps generally involve the issuer reviewing the application, conducting a credit check, and then communicating their decision. The process can vary in length, so it's essential to follow up if you haven't received a response within the timeframe specified by the issuer.

What is a Business Credit Application form?

A Business Credit Application form is a document that businesses use when applying for credit with another company. It typically requests information about the business seeking credit, including company details, financial information, and trade references. This form helps the creditor assess the creditworthiness of the applicant.

Who should use a Business Credit Application form?

Any business that wishes to establish a line of credit with a supplier or vendor should use a Business Credit Application form. It's also used by companies that provide goods or services on credit terms to other businesses. This includes manufacturers, wholesalers, and B2B service providers.

What information do I need to complete a Business Credit Application form?

To complete a Business Credit Application form, you will need to provide detailed information about your business. This includes your legal business name, contact information, business type (e.g., LLC, corporation), years in operation, and ownership details. You'll also need to provide financial information such as bank references and trade references that can vouch for your business's creditworthiness.

How can a Business Credit Application form impact my business?

Completing a Business Credit Application form can have a significant impact on your business. It can determine whether you are granted credit, which may be essential for your operational cash flow. Successfully obtaining credit means you can acquire goods or services necessary for your business operations while managing payment terms favorably. On the other hand, a poorly completed application or a decision not to grant credit could restrict your ability to grow or sustain your business operations.

Is it safe to share sensitive financial information on a Business Credit Application form?

While it is necessary to share financial information on a Business Credit Application form, it's crucial to ensure that the form is submitted through secure channels. Verify the credibility of the creditor and review their privacy policies to understand how your information will be used and protected. If possible, submit the form through encrypted email, a secure online portal, or in person to minimize the risk of your sensitive information being compromised.

Filling out a Business Credit Application form is a common step for businesses seeking to establish a line of credit with suppliers or lenders. Unfortunately, mistakes in this process can lead to delays, a lack of trust from potential creditors, or even the denial of credit. One frequent error is the failure to provide complete information. Applicants often overlook sections or fields, thinking them irrelevant or unnecessary. This omission can signal a lack of attention to detail to the creditor.

Another common mistake is not double-checking the information for accuracy. Typographical errors, especially in critical details such as the business name, address, or tax identification numbers, can render the application invalid or cause significant delays. It's crucial to proofread every piece of information before submission.

Some businesses err by not thoroughly explaining the nature of their business or its financial health. Creditors rely on a clear understanding of what the business does and its financial stability to make informed lending decisions. Vague or incomplete descriptions can hamper the credit evaluation process.

A significant misstep is failing to provide the required financial documentation. Documents such as balance sheets, income statements, and cash flow statements provide a snapshot of the company's financial health. When businesses neglect to include these documents, or if they submit outdated or inaccurate financials, creditors might question the viability of the business.

Businesses often underestimate the importance of the personal credit history of the owner(s) in the credit application process. A common mistake is not authorizing the credit check or not disclosing relevant personal credit history information when required. This oversight can lead to an automatic rejection of the application.

Another oversight is not specifying the credit terms sought. Without this information, creditors cannot adequately assess the request's feasibility or align it with their lending capabilities. Leaving this section blank or being too vague can significantly impede the application's progress.

Ignoring the importance of references is another blunder. Suppliers or other commercial credit references can vouch for the business's creditworthiness and reliability. Failure to provide this information can leave the creditor with unanswered questions about the company's track record.

Not being upfront about previous credit rejections or financial issues is a serious mistake. Applicants might feel tempted to hide past financial struggles, but this can lead to problems later in the process. Full transparency is always the best policy.

Applicants sometimes wrongly believe that once the form is submitted, the process is out of their hands. They neglect to follow up with the creditor, which can be perceived as disinterest or lack of commitment. Proactive communication is key to facilitating the evaluation process.

Last but not least, businesses often treat the credit application as a mere formality and fail to understand its legal implications. Every piece of information provided must be accurate and honest, as discrepancies can lead to legal consequences or the termination of the credit agreement. An attentive and truthful approach to filling out the form is essential.

In the realm of commercial operations, a Business Credit Application form is a cornerstone document utilized to evaluate the creditworthiness of a business that is seeking credit from another entity. This assessment, however, is rarely reliant on the credit application alone. A suite of additional documents is often required to paint a comprehensive picture of the financial health and credibility of the applying business. Each of these documents serves a specific purpose, contributing crucial details necessary for making informed decisions regarding credit agreements.

These documents, when presented alongside a Business Credit Application form, enable creditors to conduct a thorough analysis of a prospective borrower's financial health and operating performance. Understanding the purpose and the type of information each document provides can significantly impact the success of a business's credit application. By meticulously preparing and presenting these documents, businesses can enhance their credibility and increase their chances of securing the desired credit facilities.

The Business Credit Application form shares similarities with a Personal Credit Application form in its purpose of evaluating creditworthiness, but focuses on the financial health and crediting history of a business rather than an individual. Both documents collect detailed financial information, references, and consent for a credit check to inform lenders' decisions but are tailored to the distinct contexts of individuals versus businesses.

Similar to a Loan Application form, a Business Credit Application seeks to gather the essential financial and operational information of a company to determine its eligibility for credit. While a Loan Application may be broader in scope, encompassing terms like interest rates and repayment schedules, both forms serve the fundamental role of initiating a lending agreement based on evaluated risk and creditworthiness.

A Business Plan bears resemblance to the Business Credit Application in that it provides a detailed overview of a company’s operations, financial status, and growth projections. However, while a business plan is a comprehensive document aimed at giving investors or partners a snapshot of a company's future, the credit application's primary focus is on current financial health as it pertains to credit eligibility.

Vendor Credit Application forms are closely related to Business Credit Applications as both are used by companies to obtain financing or credit terms from suppliers or financial institutions. However, the Vendor Credit Application is specifically tailored to transactions between businesses and their suppliers, detailing terms like payment periods and purchase limits, which are not typically addressed in a general business credit application.

Trade References, often a component within a Business Credit Application, are standalone documents that detail a company’s payment history with other businesses. While trade references serve as evidence of a company’s reliability and financial stability, a Business Credit Application uses this information as part of a broader evaluation of creditworthiness.

The Guarantor Agreement Form is another document with a similar objective to that of a Business Credit Application in ensuring financial risk is mitigated for the lender. This agreement involves a third-party guarantor who promises to assume the debt obligation if the borrower defaults, providing an additional layer of security not unlike the thorough financial vetting of a business credit application.

A Credit Report Authorization is akin to a section commonly found in Business Credit Applications, where the applicant authorizes the lender to perform a credit check. This standalone authorization is critical for conducting due diligence, verifying the creditworthiness of an applicant before extending credit, similar to practices in the business credit application process.

Lastly, the Financial Statement closely mirrors the financial disclosure aspect of a Business Credit Application, providing a snapshot of a business's financial condition through detailed reports such as balance sheets, income statements, and cash flow statements. While a financial statement is a broader financial document, the business credit application utilizes this financial data to assess the credit risk and financial health of a company seeking credit.

When the time comes to apply for business credit, careful attention to the application process is crucial. A well-prepared application can be the difference between acceptance and rejection. To aid in this process, here are ten dos and don'ts to keep in mind when filling out a Business Credit Application form.

Do:When businesses seek to establish a line of credit with another company, the Business Credit Application form becomes a crucial document in the process. However, several misconceptions surround its usage, functions, and implications. Understanding these misconceptions is essential for both creditors and debtors to ensure clear, productive financial relationships.

Clearing up these misconceptions helps both parties approach credit relationships with the right expectations and prepares them for a more streamlined, understanding-driven process. Properly managing and understanding the components and implications of the Business Credit Application can foster healthier financial interactions between businesses.

Filling out a Business Credit Application is a critical step for businesses looking to establish a credit line or terms with a supplier. Here are key takeaways to ensure the process is handled correctly:

Approaching the Business Credit Application process with thoroughness and attention to detail can significantly influence the success of your application. It is a foundational step toward securing the financial flexibility your business needs to grow and thrive.

Power of Attorney Dmv - Instrumental for those needing a proxy to take care of vehicle-related tasks.

Free Printable Puppy Health Guarantee - Lists the vaccinations given to the puppy by the breeder and provides a vaccination history record at the time of delivery.

Da Form 2166-9-1a Fillable Pdf - Completing the DA 2166 9 1 form requires input from multiple review officers, including a rater, senior rater, and optionally a supplementary reviewer, ensuring a comprehensive evaluation.