Fillable Deed of Trust Document

Fillable Deed of Trust Document

In the world of property transactions, where securing financing and establishing legal safeguarding measures are paramount, the Deed of Trust form plays a pivotal role. This document not only outlines the agreement between a borrower and lender but also involves a neutral third party, ensuring that the lender's interests are protected should there be a default on the loan. Essentially, it serves as a form of collateral, holding the property in trust until the loan is fully repaid. Beyond its primary function, the form encompasses key provisions like the power of sale clause, which grants the trustee the authority to sell the property in the event of a default, and the reconveyance clause, which details the process for transferring the property title back to the borrower upon fulfillment of the loan terms. Understanding the nuances and implications of each section can empower parties involved in a transaction to navigate the process with confidence and clarity, making the Deed of Trust form an indispensable tool in real estate and lending transactions.

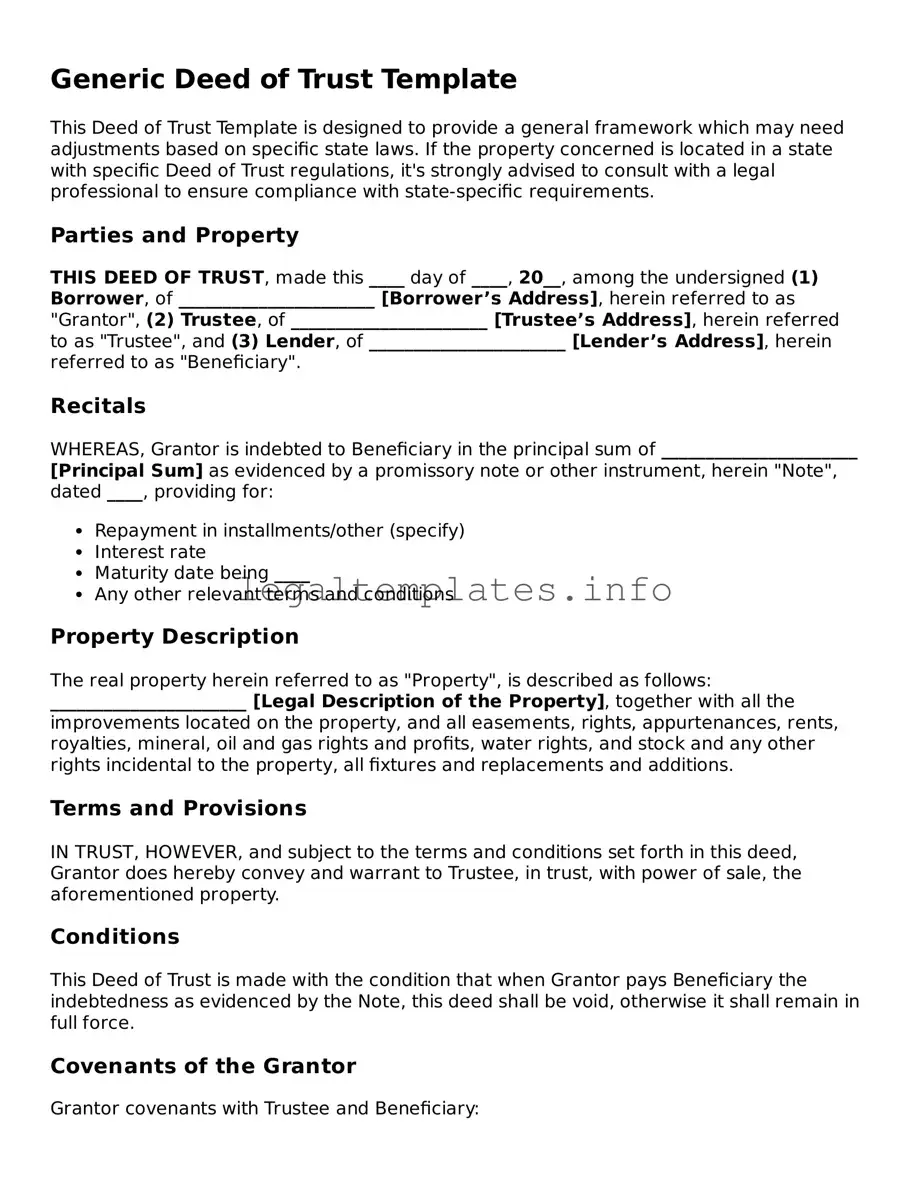

Generic Deed of Trust Template

This Deed of Trust Template is designed to provide a general framework which may need adjustments based on specific state laws. If the property concerned is located in a state with specific Deed of Trust regulations, it's strongly advised to consult with a legal professional to ensure compliance with state-specific requirements.

Parties and Property

THIS DEED OF TRUST, made this ____ day of ____, 20__, among the undersigned (1) Borrower, of ______________________ [Borrower’s Address], herein referred to as "Grantor", (2) Trustee, of ______________________ [Trustee’s Address], herein referred to as "Trustee", and (3) Lender, of ______________________ [Lender’s Address], herein referred to as "Beneficiary".

Recitals

WHEREAS, Grantor is indebted to Beneficiary in the principal sum of ______________________ [Principal Sum] as evidenced by a promissory note or other instrument, herein "Note", dated ____, providing for:

Property Description

The real property herein referred to as "Property", is described as follows: ______________________ [Legal Description of the Property], together with all the improvements located on the property, and all easements, rights, appurtenances, rents, royalties, mineral, oil and gas rights and profits, water rights, and stock and any other rights incidental to the property, all fixtures and replacements and additions.

Terms and Provisions

IN TRUST, HOWEVER, and subject to the terms and conditions set forth in this deed, Grantor does hereby convey and warrant to Trustee, in trust, with power of sale, the aforementioned property.

Conditions

This Deed of Trust is made with the condition that when Grantor pays Beneficiary the indebtedness as evidenced by the Note, this deed shall be void, otherwise it shall remain in full force.

Covenants of the Grantor

Grantor covenants with Trustee and Beneficiary:

Additional Provisions

In addition to the above, the following provisions shall apply:

[Insert any additional provisions here]

Execution

IN WITNESS WHEREOF, the parties have caused this Deed of Trust to be executed as of the day and year first above written.

______________________ [Signature of the Borrower]

______________________ [Signature of the Trustee]

______________________ [Signature of the Lender]

| Fact Number | Description |

|---|---|

| 1 | A Deed of Trust is a document that secures a loan on real property. |

| 2 | It involves three parties: the borrower (trustor), the lender (beneficiary), and a neutral third party (trustee). |

| 3 | The trustee holds the legal title to the property until the borrower repays the loan. |

| 4 | In the event of default, the trustee has the power to sell the property to pay off the loan. |

| 5 | Deed of Trust is used instead of a mortgage in some states like California, Texas, and Virginia. |

| 6 | The governing law is typically the law of the state where the property is located. |

| 7 | Recording the Deed of Trust with the county recorder's office is necessary to perfect the deed against claims from third parties. |

| 8 | Foreclosure processes vary by state; Deed of Trust states often allow for a non-judicial foreclosure process. |

When embarking on the significant journey of securing a loan for purchasing or refinancing real estate, a Deed of Trust often becomes an essential document in many states in the United States. Serving as a pivotal agreement, it involves three parties: the borrower, the lender, and the trustee, laying out the legal framework that protects the lender's interest in the property until the loan is paid in full. While the process might seem daunting, accurately completing the Deed of Trust is a crucial step. Here’s how to navigate through the form:

Completing the Deed of Trust form is a meticulous process that requires close attention to detail to ensure every part of the agreement is accurately reflected and legally binding. By following the steps outlined, individuals can navigate this process more confidently, understanding their role and responsibilities within this pivotal real estate transaction.

What is a Deed of Trust?

A Deed of Trust is a document that secures a loan on real property. It involves three parties: the borrower (trustor), the lender (beneficiary), and a neutral third party (trustee) who holds the title until the loan is repaid. In the event of a default, the trustee has the authority to sell the property to satisfy the debt.

How does a Deed of Trust differ from a Mortgage?

While both are used to secure a loan on real estate, a Deed of Trust involves a third party, the trustee, unlike a mortgage that typically involves only the borrower and the lender. Additionally, in case of default, a Deed of Trust allows for a quicker foreclosure process through a trustee's sale, avoiding the traditional court process required for a mortgage foreclosure.

Who can serve as a trustee in a Deed of Trust?

Typically, a trustee is a neutral third party, often a title company, attorney, or other entity agreed upon by both the lender and borrower. The trustee must be able to impartially conduct a sale of the property if necessary, adhere to state laws, and fulfill the duties outlined in the Deed of Trust.

Is it possible to modify a Deed of Trust?

Yes, but modifications must be agreed upon by all the involved parties. These modifications might include changes in the loan terms, payment schedule, or other significant amendments. Any changes should be documented in writing and, depending on state law, may need to be recorded with the local county recorder’s office.

What happens if the borrower defaults under a Deed of Trust?

If the borrower defaults, the trustee has the authority to sell the property through a non-judicial foreclosure process. This process is typically faster than a judicial foreclosure, as it does not require court intervention. The specifics of the process and the borrower's rights to remedy the default before sale vary by state law.

Can a borrower sell a property under a Deed of Trust?

Yes, a borrower can sell their property even if there is an active Deed of Trust. However, the loan secured by the Deed of Trust must be paid off at or before closing, either with the sale proceeds or by the borrower. Any unpaid balance must be resolved for the deed to be released, clearing the title for the new owner.

What is a reconveyance in the context of a Deed of Trust?

A reconveyance is the process of transferring the property title back to the borrower (trustor) once the loan is fully repaid. The trustee performs a reconveyance by recording a deed of reconveyance with the county recorder’s office, which releases the lender's interest in the property and clears the title.

How is a Deed of Trust terminated?

A Deed of Trust is terminated when the loan it secures is fully repaid. Upon full repayment, the trustee records a deed of reconveyance with the local county recorder’s office, officially removing the lien from the property title and terminating the Deed of Trust.

Are there any state-specific regulations for Deeds of Trust?

Yes, the use of Deeds of Trust and the laws governing them vary significantly by state. For example, some states allow for a non-judicial foreclosure process under a Deed of Trust, while others require a judicial process. It is crucial to consult with a legal professional familiar with the specific laws and regulations in your state when dealing with a Deed of Trust.

One common mistake people make when filling out the Deed of Trust form is not verifying the exact legal description of the property. This description is crucial and must match the one listed in official property records exactly. Any discrepancies can lead to significant issues down the line, such as delays in the process or questions about the property's rightful ownership. Ensuring this information is accurate and aligns with official records is essential for the deed to be legally binding and effective.

Another error often seen is failing to include all necessary parties in the document. The Deed of Trust should list every individual or entity with a legal interest in the property, including co-owners, trustees, and beneficiaries. Many people overlook this detail, mistakenly believing only the primary owner needs to be named. This omission can result in legal complications, potentially disqualifying the document from being recognized officially or causing disputes among parties with an interest in the property.

A third mistake involves not having the document notarized. In many jurisdictions, a Deed of Trust must be notarized to be considered valid. This step is more than a formality; it's a legal requirement that confirms the identities of the signatories and attests to the voluntary nature of their signatures. Skipping this step can render the entire document null and void, stripping it of any legal weight and preventing it from being recorded officially.

Lastly, individuals often neglect to file the completed Deed of Trust with the relevant county recorder’s office. Filing is a critical step that officially logs the document into public record, making it a part of the property’s legal history. Failure to file means the Deed of Trust might not be recognized in legal challenges or when the property is sold. This oversight can lead to disputes over property rights and complicate future transactions involving the property.

When it comes to securing a real estate transaction, a Deed of Trust is a significant document but it seldom acts alone. To ensure a transparent, legal, and thorough process, several other forms and documents accompany the Deed of Trust. These documents work collectively to protect the interests of all parties involved, offering a structured framework for the agreement's terms, conditions, and provisions. Below is a closer look at some of these essential documents.

Accompanied by these additional forms and documents, the Deed of Trust becomes part of a comprehensive legal framework that ensures all aspects of the property transaction are duly recorded and acknowledged. For buyers, sellers, and lenders, understanding and managing these documents is crucial for a smooth real estate transaction that safeguards everyone's interests.

A Mortgage Agreement closely mirrors the Deed of Trust in its fundamental purpose of binding a borrower to repay a loan used to purchase a property. However, the primary distinction is in the parties involved; while a Deed of Trust necessitates a third-party trustee who holds the title until the debt is paid, a Mortgage Agreement directly involves only the lender and the borrower. Despite this difference, both documents serve as legal instruments to secure a loan on real property, allowing for foreclosure if the borrower defaults on the payment terms.

Similar in intent to a Deed of Trust, a Promissory Note is an essential document within the realm of financing and loans. It represents a borrower's promise to repay a specific amount of money to the lender over a set period, often including interest. While a Promissory Note details the financial obligations of the borrower to the lender, it does not, by itself, create a lien on the property. However, when paired with a Deed of Trust or Mortgage, it becomes a powerful legal tool ensuring the borrower's adherence to the repayment schedule.

The Land Contract shares similarities with a Deed of Trust, particularly in its facilitation of the purchase of real estate without a traditional mortgage loan. Under a Land Contract, the seller provides financing to the buyer directly, allowing the buyer to make payments over time. Until the full purchase price is paid, the seller retains legal title to the property, serving a role akin to that of the trustee in a Deed of Trust. This arrangement concludes once the buyer completes all payments, transitioning full ownership to them, similar to how a Deed of Trust is extinguished once the debt is repaid.

Lastly, a Security Agreement shares a conceptual framework with a Deed of Trust, especially in terms of securing a loan through collateral. While a Deed of Trust uses real property as collateral, a Security Agreement can encompass a broader range of assets, including personal property, vehicles, or equipment. The agreement grants the lender a security interest in the specified collateral, providing a recourse in the event of default. Despite their differences in the nature of collateral, both documents ensure the lender's interests are protected and can be legally pursued in case of non-repayment.

When preparing a Deed of Trust, it is important to proceed with care to ensure the document accurately reflects the agreement between the parties involved. Below are key dos and don'ts to consider:

Dos:

Double-check the legal description of the property. This description is crucial for identifying the property and must be accurate.

Ensure all parties involved in the transaction are correctly identified by their full legal names to prevent any confusion regarding the identities of the trustor, trustee, and beneficiary.

Clearly specify the loan amount. This should be the exact amount borrowed that the deed of trust is securing.

Include all necessary terms of the loan, such as the interest rate, payment schedule, maturity date, and any requirements or obligations.

Sign and notarize the document. The deed of trust must be signed by the trustor in front of a notary to be legally binding.

Record the deed of trust with the county recorder's office where the property is located. This public recording is essential for establishing the legal standing of the deed.

Don'ts:

Omit any parties involved in the agreement. Each relevant party must be explicitly mentioned for the deed to be enforceable.

Forget to specify any pertinent details of the loan agreement. Lack of clarity can lead to disputes or legal issues.

Use vague language. It's crucial that the terms are spelled out clearly to avoid ambiguity and misunderstanding.

Leave spaces blank. If a section does not apply, mark it as “N/A” instead of leaving it empty to prevent unauthorized additions.

Fail to check for compliance with state and local laws. Each jurisdiction may have specific requirements or restrictions for deeds of trust.

Ignore the requirement for a notary. A deed of trust generally needs to be notarized to be considered valid and enforceable.

When it comes to securing real estate transactions, a Deed of Trust often plays a pivotal role. However, several misconceptions surround its function and importance, leading to confusion. Let's debunk some common myths:

Understanding the nuances of a Deed of Trust not only helps in making informed decisions but also in navigating the complexities of real estate transactions more effectively.

Understanding the nuances of the Deed of Trust form can significantly impact the process of securing and managing real estate financing. Below are key takeaways to consider when dealing with a Deed of Trust:

By understanding these key aspects, parties can effectively navigate the complexities of Deed of Trust forms, ensuring that their interests are protected and legal obligations are clear.

Deed of Gift Form - Documenting a gift through this form eliminates ambiguity, cementing the transfer's validity and the parties' understanding.

What Is Deed in Lieu - The document layout and content may vary depending on state laws, making it essential to consult with legal professionals before drafting.