Fill a Valid Fl Dr 312 Form

Fill a Valid Fl Dr 312 Form

Understanding the intricacies of estate management and tax obligations can be a daunting task, particularly for those navigating the process in the state of Florida. The Affidavit of No Florida Estate Tax Due, known as Florida Form DR-312, serves as a critical document for personal representatives of estates. This form is essential when an estate does not owe Florida estate tax under Chapter 198, Florida Statutes, and a federal estate tax return is not required, simplifying the administration of the estate. Designed to be filed with the clerk of the circuit court where the decedent owned property, the DR-312 form is a declaration by the personal representative that, to the best of their knowledge, the estate is exempt from these taxes. This affidavit not only assures the state that the estate has no Florida estate tax due but also acts to remove the Department of Revenue’s estate tax lien, streamlining the process for the personal representative. Additionally, the document provides guidelines on when and how to file, who qualifies as a personal representative, and what circumstances require its use. Its execution is crucial for ensuring compliance with state tax laws and facilitating the efficient distribution of the decedent's estate, making it a fundamental aspect of estate administration in Florida.

Affidavit of No Florida Estate Tax Due

Rule

Effective 01/21

Page1 of 2

(This space available for case style of estate probate proceeding) |

(For official use only) |

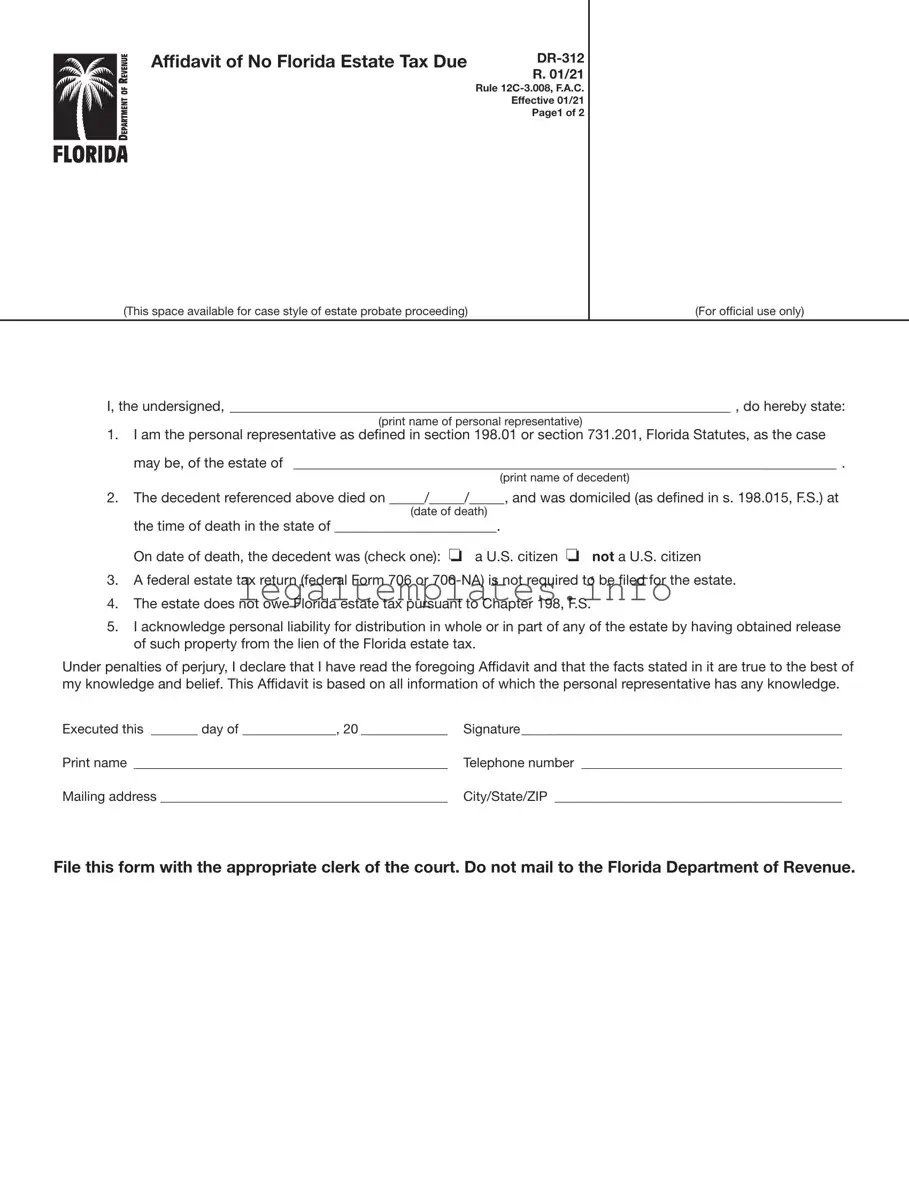

I, the undersigned, _______________________________________________________________________ , do hereby state:

(print name of personal representative)

1.I am the personal representative as defined in section 198.01 or section 731.201, Florida Statutes, as the case may be, of the estate of _____________________________________________________________________________ .

(print name of decedent)

2.The decedent referenced above died on _____/_____/_____, and was domiciled (as defined in s. 198.015, F.S.) at

(date of death)

the time of death in the state of _______________________.

On date of death, the decedent was (check one): o a U.S. citizen o not a U.S. citizen

3.A federal estate tax return (federal Form 706 or

4.The estate does not owe Florida estate tax pursuant to Chapter 198, F.S.

5.I acknowledge personal liability for distribution in whole or in part of any of the estate by having obtained release of such property from the lien of the Florida estate tax.

Under penalties of perjury, I declare that I have read the foregoing Affidavit and that the facts stated in it are true to the best of my knowledge and belief. This Affidavit is based on all information of which the personal representative has any knowledge.

Executed this _______ day of ______________, 20 _____________ |

Signature________________________________________________ |

Print name _______________________________________________ |

Telephone number _______________________________________ |

Mailing address ___________________________________________ |

City/State/ZIP ___________________________________________ |

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

R. 01/21

Page 2 of 2

Instructions for Completing Form

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

General Information

If Florida estate tax is not due and a federal estate tax return (federal Form 706 or

Form

The

Where to File Form

Form

When to Use Form

Form

and a federal estate tax return (federal Form 706 or

Federal thresholds for filing federal Form 706 only: (For informational purposes only. Please confirm with Form 706 instructions.)

Date of Death |

Dollar Threshold |

(year) |

for Filing Form 706 |

|

(value of gross estate) |

|

|

2000 and 2001 |

$675,000 |

|

|

2002 and 2003 |

$1,000,000 |

|

|

2004 and 2005 |

$1,500,000 |

|

|

For 2006 and forward |

|

go to the IRS website at |

|

www.irs.gov to obtain |

|

thresholds. |

|

|

|

For thresholds for filing federal Form

If an administration proceeding is pending for an estate, Form

To Contact Us

Information, forms, and tutorials are available on the Department’s website floridarevenue.com

If you have any questions, or need assistance, call Taxpayer Services at

To find a taxpayer service center near you, go to: floridarevenue.com/taxes/servicecenters

For written replies to tax questions, write to: Taxpayer Services - Mail Stop

5050 W Tennessee St Tallahassee FL

Subscribe to Receive Email Alerts from the Department.

Subscribe to receive an email when Tax Information Publications and proposed rules are posted to the Department’s website. Subscribe today at floridarevenue.com/dor/subscribe.

Reference Material

Rule Chapter

| Fact Name | Description |

|---|---|

| Form Purpose | The DR-312 form is utilized by personal representatives to declare that no Florida estate tax is due and a federal estate tax return is not required for the estate in question. |

| Governing Laws | This form is governed by Rule 12C-3.008 of the Florida Administrative Code (F.A.C.) and the relevant provisions of Chapter 198, Florida Statutes (F.S.). |

| Who Should Use It | Personal representatives, including those in actual or constructive possession of an estate's property, should complete this form when a federal Form 706 or 706-NA is not required and the estate owes no Florida estate tax. |

| Where and When to File | The form must be recorded with the clerk of the circuit court in the county or counties where the decedent owned property, not sent to the Florida Department of Revenue. It is meant for use when an estate is not subject to Florida estate tax under Chapter 198, F.S., and a federal estate tax return is not required. |

Embarking on the task of completing the Florida DR-312 form, Affidavit of No Florida Estate Tax Due, requires attentive accuracy and a focused understanding of the deceased's estate. This form plays a crucial role for personal representatives or individuals who are managing the assets of someone who has passed away, facilitating the process to officially declare that the estate is not subject to Florida estate tax and thus, removing the department's tax lien. Below lies a detailed guide, structured to aid in the step-by-step completion of this form, ensuring that all the necessary procedures are meticulously followed.

Upon completion, individuals must proceed to file the form in the correct jurisdiction, adhering to the provided instructions. This task marks an important step in managing the estate, ensuring compliance with state requirements, and moving forward in the estate settlement process.

What is the purpose of the Florida Form DR-312?

The Florida Form DR-312, also known as the Affidavit of No Florida Estate Tax Due, is a legal document used to declare that no Florida estate tax is owed on an estate. It is necessary when an estate is not subject to Florida estate tax under Chapter 198, F.S., and when a federal estate tax return is not required. This affidavit helps in the removal of the Department of Revenue's estate tax lien on the decedent's property.

Who needs to file the DR-312 form?

The form must be completed and filed by the personal representatives of the decedent's estate. This includes any person who is in actual or constructive possession of the estate's assets. The definition of "personal representative" in Chapter 198, F.S., encompasses executors, administrators, and others in control of the estate's assets.

When should the DR-312 form be used?

The DR-312 form should be used when an estate is not obligated to pay Florida estate tax under Chapter 198, F.S., and a federal estate tax return (federal Form 706 or 706-NA) is not necessary. It is important to note that this form cannot be utilized for estates that are required to file a federal Form 706 or 706-NA.

Where should the form be filed?

The form must be recorded directly with the clerk of the circuit court in the county or counties where the decedent owned property. It is essential not to send this form to the Florida Department of Revenue but rather to ensure it is duly recorded in the public records of the relevant county or counties.

What is the process for completing the DR-312 form?

To complete the DR-312 form, personal representatives must fill in specific details about the decedent and the estate, acknowledge their understanding of their liabilities, and declare under penalties of perjury that the information provided is accurate. The form requires information such as the name of the decedent, the date of death, and confirmation that a federal estate tax return is not required.

How can someone obtain help or more information about the DR-312 form?

For assistance or more information about the DR-312 form, individuals can visit the Florida Department of Revenue's website at floridarevenue.com. Taxpayer Services can also be contacted for help Monday through Friday, excluding holidays, at 850-488-6800. Additionally, written inquiries can be sent to the department as described in the instructions for the form.

Filling out the FL DR 312 form, "Affidavit of No Florida Estate Tax Due," is an important step in settling an estate in Florida, yet it's often where mistakes are made. One common error occurs when individuals fail to accurately describe their role. The form specifically requires identification as the personal representative, a term that includes anyone in actual or constructive possession of the estate. Failing to recognize the breadth of this definition can lead to inaccuracies in the affidavit.

Another frequent mistake is concerning the decedent’s domicile information. A clear understanding of domicile—as defined in section 198.015, F.S.—is crucial. The form asks for confirmation that the decedent was domiciled in a specific state at the time of death. Misinterpretation or incorrect information here can significantly impact the filing.

The question of U.S. citizenship is also a common stumbling block. The form asks whether the decedent was a U.S. citizen at the time of death, with options to check "yes" or "no." This detail affects the necessity of a federal estate tax return and subsequently the requirement for this affidavit. Overlooking or misinterpreting this could inaccurately represent the estate's tax obligations.

An additional area where errors happen is in addressing the requirement for a federal estate tax return. The form explicitly states that if a federal Form 706 or 706-NA is not required, then this affidavit should be completed. However, individuals often misunderstand or overlook the prerequisites stated in the instructions for these federal forms, leading to filing mistakes.

Another repetitive issue is not providing accurate or complete information regarding the estate's tax obligations under Chapter 198, F.S. The affirmation that the estate owes no Florida estate tax is a significant declaration, requiring utmost attention to the estate’s financial details. Inaccuracies here could result in legal and financial repercussions.

Misunderstandings about personal liability for distribution also arise. The form necessitates acknowledgment of personal liability in the event of premature distribution of the estate. This is a crucial legal statement that some may not fully grasp, potentially leading to personal financial risk.

Finally, a common oversight involves the proper filing of the completed form. The DR-312 must be recorded directly with the clerk of the circuit court in the county or counties where the decedent owned property, not sent to the Florida Department of Revenue. This specific instruction is often missed, delaying the settlement process.

When navigating the complexities of estate management in Florida, particularly after a loved one's passing, understanding which documents to gather can be a formidable part of the process. The Affidavit of No Florida Estate Tax Due, also known as Form DR-312, plays a crucial role for those managing estates not subject to Florida estate tax. However, this form is only a single component of a broader array of documents typically required to comprehensively handle an estate's legal and financial affairs. Below is a list of other vital forms and documents often used alongside Form DR-312, each serving its unique purpose in the estate administration process.

Each of these documents contributes to the proper management and closure of an estate, ensuring that legal requirements are met, and the decedent's wishes are honored. Whether used to validate the absence of estate tax liability with Form DR-312, distribute assets among heirs, or settle the decedent's debts, these documents collectively help streamline the complex process of estate administration. Understanding and obtaining the right documents is a critical step toward achieving a smooth and compliant estate settlement.

The Affidavit of No Florida Estate Tax Due (Form DR-312) shares similarities with other legal and tax documents that affirms or declares certain facts. One example is the Affidavit of Heirship, which is used primarily in estate proceedings to identify the heirs of a deceased person. This affidavit, like the DR-312, serves as a sworn statement regarding family relationships and helps to facilitate the transfer of property to heirs when there is no will.

Another similar document is the Small Estate Affidavit, a form that allows for the assets of the deceased to be distributed without formal probate. This document, akin to the DR-312, is typically used when the value of the estate falls below a certain threshold, thereby simplifying the legal process involved in distributing the deceased's property.

The Federal Tax Form 706, which is referred to in the DR-312 form, is another example. This form is for the United States Estate (and Generation-Skipping Transfer) Tax Return, required by the IRS when a deceased person's estate exceeds certain value thresholds. The DR-312 explicitly mentions Form 706 as part of its criteria, highlighting a connection in their use regarding estate tax responsibilities.

Additionally, the Transfer on Death (TOD) Deed or Affidavit is a document that allows individuals to name beneficiaries to receive property upon the death of the owner, bypassing probate. This document's purpose resonates with the DR-312's objective in facilitating smoother transfer of assets, though the DR-312 focuses on tax implications.

Similarly, a Release of Lien document, used in various contexts including tax liens, mortgage liens, and mechanic's liens, shares the goal of the DR-312 in removing a specific lien – in this case, the lien of the Florida estate tax on the property of the deceased.

The trust certification or affidavit of trust may also be considered akin to the DR-312. This legal document verifies the existence of a trust and the trustee's authority without revealing the full details of the trust. Like the DR-312, it is used to simplify and confirm legal authority in financial and legal transactions.

The Nonresident Alien's Estate Tax Return (Form 706-NA) is another specific form that has similarities with the DR-312 for estates belonging to deceased nonresidents not citizens of the United States. While Form 706-NA is used to declare estate values for tax purposes on a federal level, the DR-312 is used at the state level in Florida to affirm that no estate tax is due.

A Declaration Under Probate Code, another common affidavit used in estate planning and settlement, affirms various facts under the probate code, similar to the DR-312’s function of affirming no estate tax liability under Florida law.

Lastly, the Executor’s/ Administrator’s Deed mirrors the intent behind Form DR-312 by facilitating the transfer of property from an estate under an executor's or administrator’s authority. While the DR-312 helps clear the way for such transfers by confirming that no estate tax is due, the Executor’s/Administrator’s Deed is the mechanism by which the property is legally transferred.

When dealing with the Form DR-312, Affidavit of No Florida Estate Tax Due, there are several do's and don'ts to ensure the process is handled accurately and efficiently. This form is essential for declaring that an estate owes no Florida estate tax and for releasing the estate from related liens. Here are eight crucial points to consider:

Adhering to these guidelines will facilitate a smoother process in declaring an estate free of Florida estate tax through Form DR-312. Remember, accurate and thorough completion of the form is essential to avoid any potential issues with the state tax regulations.

Understanding the complexities of estate management often involves navigating through various legal forms, chief among them being Florida's DR-312, known as the "Affidavit of No Florida Estate Tax Due." This document plays a crucial role in the probate process for Florida residents, yet it's commonly misunderstood. Here are five misconceptions surrounding the DR-312 form and the truths behind them.

Many people believe that every estate must file a DR-312 form, which is not the case. This form is specifically required when an estate is not subject to Florida estate tax under Chapter 198, F.S., and a federal estate tax return is not necessary. Essentially, it is used for estates that fall below certain federal thresholds, making it unnecessary for every estate.

A common error is thinking this form should be sent to the Florida Department of Revenue. The instructions explicitly state that the DR-312 must be filed with the clerk of the circuit court in the county where the decedent owned property. It is a document intended for court records, not the tax authority.

Though the affidavit serves as evidence of non-liability for Florida estate taxes, and is designed to remove the Department’s tax lien, it's not an instant guarantee. Completing it correctly and having it recorded are necessary steps, but they're part of a broader process that may require further validation or documentation.

While it is always advisable to seek legal guidance when dealing with estate affairs, the DR-312 form has been designed for straightforward cases where no Florida estate tax is due, and no federal estate return is necessary. It requires basic information about the decedent and the estate, aiming to be accessible for personal representatives.

The affidavit makes provisions for both U.S. citizens and non-U.S. citizens, thereby debunking the myth that it's exclusively for American citizens' estates. It considers the domicile of the decedent at the time of death, which caters to a broader range of estates including those of non-U.S. citizens.

In summary, the DR-312 form is a vital document for specific estates in Florida, designed to simplify the probate process for those that meet certain criteria. Understanding its purpose, requirements, and how it fits into the larger estate management process can help avoid common pitfalls and ensure smoother proceedings.

Understanding the Affidavit of No Florida Estate Tax Due, also known as Form DR-312, is crucial for personal representatives handling estates in Florida. Here are key takeaways to ensure its proper completion and use:

Handling the responsibilities of a personal representative requires attention to legal forms like the DR-312. Whether managing an estate that crosses the federal threshold for estate taxes or navigating the specifics of Florida law, keeping these key points in mind will guide you through the process with clarity and compliance.

Cg 2010 - This endorsement is a common requirement in construction contracts, leasing agreements, and other commercial arrangements involving physical operations.

Act of Donation of a Movable - It makes the process of donating vehicles, land, or other significant assets as seamless as possible for both parties involved.

Health Insurance Marketplace Statement - For families with more than one health insurance policy, a separate 1095-A form is provided for each policy.