Fill a Valid Gift Letter Form

Fill a Valid Gift Letter Form

When a loved one decides to generously contribute towards a significant milestone in your life, such as the purchase of a new home or starting a business, they may choose to give you a financial gift. This act of generosity, while simple in intention, carries with it a degree of bureaucratic oversight when the institutions that oversee our financial lives become involved. To navigate this landscape, the Gift Letter form becomes an indispensable tool. This document serves not only as a record of the gift, ensuring transparency and honesty between parties, but also as a crucial piece of evidence for financial institutions and tax authorities, who require proof that the funds are indeed a gift and not a loan that needs to be repaid. The major aspects of this form include the declaration of the gift amount, the relationship between the giver and the recipient, and any conditions attached to the gift. Ensuring this form is accurately completed and duly signed helps in making significant financial steps smoother and more secure, affording peace of mind to all involved parties.

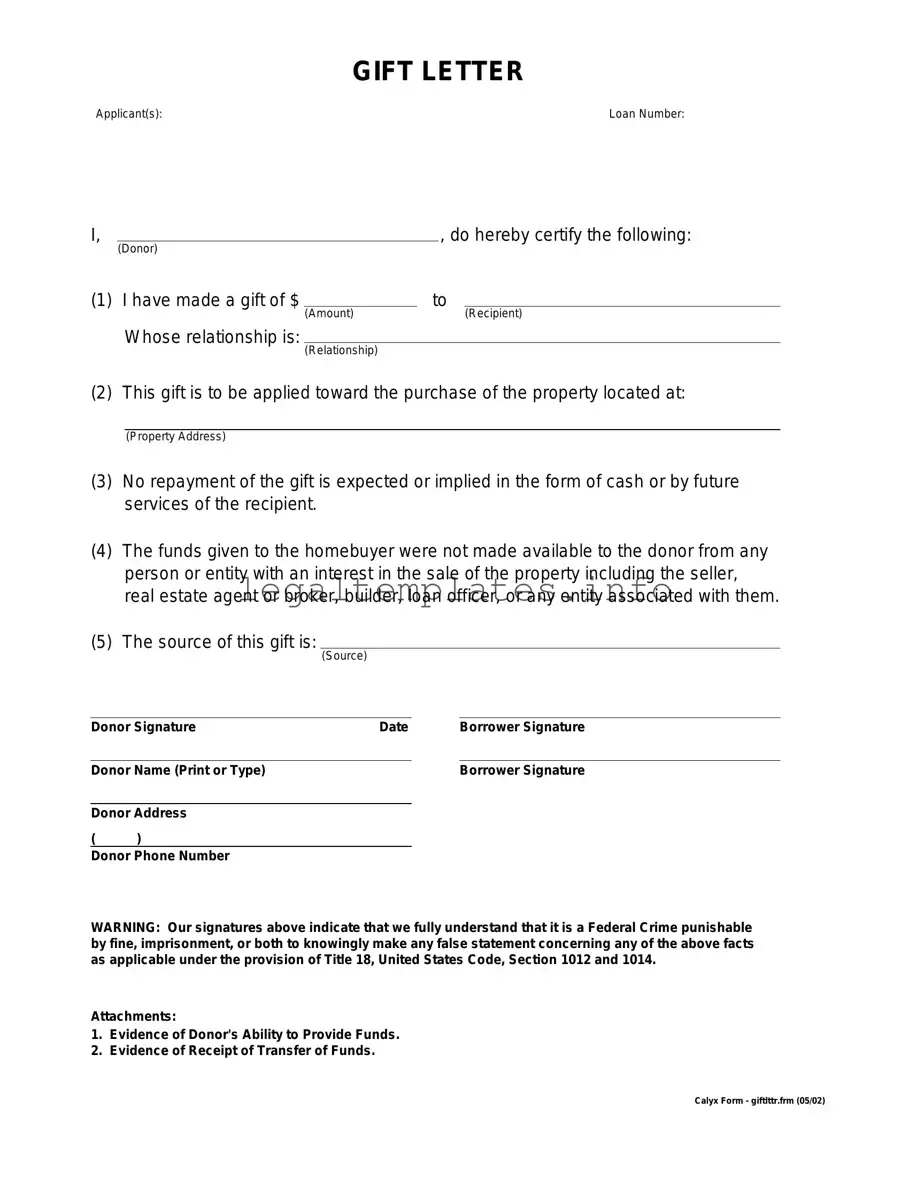

GIFT LETTER

Applicant(s): |

Loan Number: |

I, |

|

|

, do hereby certify the following: |

||

|

(Donor) |

|

|

|

|

(1) I have made a gift of $ |

|

to |

|

||

|

|

(Amount) |

|

|

(Recipient) |

|

Whose relationship is: |

|

|

|

|

|

|

(Relationship) |

|

|

|

(2) This gift is to be applied toward the purchase of the property located at:

(Property Address)

(3)No repayment of the gift is expected or implied in the form of cash or by future services of the recipient.

(4)The funds given to the homebuyer were not made available to the donor from any person or entity with an interest in the sale of the property including the seller, real estate agent or broker, builder, loan officer, or any entity associated with them.

(5)The source of this gift is:

(Source)

Donor Signature |

Date |

Borrower Signature |

||

|

|

|

|

|

Donor Name (Print or Type) |

|

|

Borrower Signature |

|

|

|

|

|

|

Donor Address |

|

|

|

|

( |

) |

|

|

|

Donor Phone Number

WARNING: Our signatures above indicate that we fully understand that it is a Federal Crime punishable by fine, imprisonment, or both to knowingly make any false statement concerning any of the above facts as applicable under the provision of Title 18, United States Code, Section 1012 and 1014.

Attachments:

1.Evidence of Donor's Ability to Provide Funds.

2.Evidence of Receipt of Transfer of Funds.

Calyx Form - giftlttr.frm (05/02)

| Fact Name | Description |

|---|---|

| Purpose of the Gift Letter | The Gift Letter form is used to provide proof that funds received by a homebuyer from a family member or friend are indeed a gift and not a loan that needs to be repaid. This clarification helps lenders determine the buyer's true financial situation. |

| Components of the Gift Letter | Typically, a Gift Letter will include the donor’s name, relationship to the recipient, the gift amount, the date of the gift, and a statement that no repayment is expected or required. |

| Governing Laws | While Gift Letters are used throughout the United States, the requirements can vary by state due to different governing laws. However, most lenders follow guidelines set by federal mortgage agencies like Fannie Mae, Freddie Mac, FHA, VA, or USDA. |

| Importance for Mortgage Approval | Lenders scrutinize a homebuyer's financial background to ensure the ability to repay the home loan. A Gift Letter helps in verifying part of the funds the buyer will use, potentially making it easier to qualify for a mortgage by confirming the financial gift's authenticity. |

When individuals provide a substantial gift to another person, usually a family member, for purposes such as assisting in the purchase of a home, a Gift Letter form may be required by financial institutions. This form serves as evidence that the funds being transferred are indeed a gift and not a loan to be repaid. Completing this document accurately is crucial for ensuring the recipient’s mortgage application process proceeds smoothly. Below are the steps to properly fill out a Gift Letter form.

Once finished, review the document for accuracy and completeness. This letter, when submitted alongside the necessary financial paperwork, helps illustrate the financial background of the gift and its implications for the recipient's financial standing. It's important to keep a copy for personal records before submitting it to the required financial institution or mortgage lender.

What is a Gift Letter?

A Gift Letter is a document that clearly states that money given by one person to another is a gift, meaning it does not have to be repaid. This form is often used when a family member gives money towards the purchase of a home, ensuring that the lender understands the funds are not an additional loan.

When do I need a Gift Letter?

You might need a Gift Letter during the mortgage application process. If you're receiving financial help towards your down payment or closing costs from someone, your lender will likely require this letter to prove that the assistance is not a loan.

Who can provide a gift according to the Gift Letter?

Typically, gifts can be provided by family members, such as parents, grandparents, siblings, or close relatives. Some lenders may also accept gifts from non-relatives under certain conditions. It's important to check with your lender for their specific requirements.

What information should be included in a Gift Letter?

A Gift Letter should clearly identify the donor and recipient, the relationship between them, the exact amount of the gift, a statement that no repayment is expected or required, and the purpose of the gift. It should also include the signatures of both the donor and recipient.

Is there a specific format for a Gift Letter?

While there's no one mandatory format, a Gift Letter should be clear and contain all necessary information to satisfy lender requirements. Many lenders have their own form or preferred format, so it's wise to check with them first.

Can a Gift Letter affect my taxes?

For the donor, large gifts may have implications for gift taxes. The recipient usually does not have to worry about taxes, as gifts are not considered taxable income. However, it's a good idea to consult with a tax professional to understand any potential tax implications.

Does the donor need to prove the source of the gift funds?

Yes, lenders often require donors to provide evidence of where the gift money came from. This can include bank statements or other financial documents. It helps lenders ensure the money is indeed a gift and not a loan in disguise.

How does a Gift Letter protect the recipient?

A Gift Letter helps assure the lender that the recipient has the financial support needed to complete the home purchase without risking additional debt. It's a safeguard that clarifies the nature of the support as a gift, not a loan.

Can a Gift Letter be rescinded?

Once a gift is given and the letter is signed, it's typically not possible to rescind the gift, given it’s supposed to indicate the transfer of funds with no expectation of repayment. Any change of heart or circumstances would involve legal aspects beyond the scope of a simple Gift Letter.

One common mistake people make when filling out the Gift Letter form is not specifying the relationship between the giver and the recipient. This detail is crucial because it provides context for the transaction and helps to establish that the gift is legitimate. Financial institutions often scrutinize gift letters to ensure there are no expectations of repayment, and understanding the relationship helps in assessing the genuineness of the gift. Without this information, the gift could be misconstrued as a loan, potentially complicating the recipient's financial assessments.

Another error frequently encountered is failing to provide the exact amount of the gift. Being vague or imprecise about the amount can raise red flags with lenders or other interested parties. It is essential to clearly state the exact figure being gifted to ensure transparency and to aid in the proper documentation of funds. This precise amount confirms that the donor has the financial capacity to make the gift and that the recipient has received a specific sum that could influence their financial situation, for instance, in the calculation of their mortgage affordability.

A third mistake often found in Gift Letter forms is not including the statement that the gift does not have to be repaid. This is a critical component of the letter, as it distinguishes a gift from a loan. Without this declaration, there could be ambiguity about whether the recipient is expected to repay the sum, potentially affecting their debt-to-income ratio. Lenders, in particular, require clarity on this issue to accurately assess an applicant's creditworthiness and financial responsibilities.

Lastly, many overlook the necessity of having the letter properly dated and signed. The date of the gift can be important for tax purposes, as well as for aligning with the timeline of the recipient's financial activities, such as the purchase of a home. The signature authenticates the letter, making it a valid document. An undated or unsigned letter lacks legal standing, which can lead to questions about its validity and the authenticity of the information provided.

When managing transactions or arrangements that include a gift, especially in the realm of finance or real estate, the Gift Letter form is a crucial document. However, a Gift Letter rarely stands alone. Several other forms and documents often accompany it to ensure completeness, compliance, and clarity in the transaction. Understanding these additional documents can provide a broader perspective on the process and requirements involved. Here's a list of 10 forms and documents that are commonly used alongside a Gift Letter.

Navigating through the process of receiving or giving a gift with financial implications involves more than just signing a Gift Letter. The associated documents ensure that all aspects of the transaction are transparent, legal, and in the best interest of all parties involved. Whether you're buying a home or dealing with another significant transaction, understanding these documents can empower you to proceed with confidence and clarity.

The Affidavit of Gift is a document closely related to the Gift Letter form, sharing the primary purpose of legally documenting the transfer of an item or money from one individual to another without any expectation of payment. Both serve to clarify the nature of the transaction, ensuring it is recognized as a gift by legal and financial entities, particularly important for tax purposes. The affidavit, however, typically requires notarization, providing an additional layer of verification and formalization compared to the more straightforward Gift Letter.

A Promissory Note bears similarities to a Gift Letter in the sense that both involve the transfer of money between parties. However, while a Gift Letter asserts that the funds are provided without expectation of return, a Promissory Note details the borrower's promise to repay the lender. This key difference outlines the nature of the agreement between the parties, making one a document of generosity and the other a legal obligation for repayment, complete with specified terms including, but not limited to, repayment schedule, interest rate, and consequences of non-payment.

The Deed of Gift is another document similar to a Gift Letter, often used in the transfer of real estate or significant personal property. It details the voluntary transfer of property ownership from one individual to another without payment, much like the Gift Letter does for personal or monetary gifts. The Deed of Gift, however, is more complex and formal, usually requiring legal assistance to ensure its validity and often needing to be recorded with local government offices, a step not typically required for a Gift Letter.

The Loan Agreement shares a conceptual relationship with the Gift Letter by outlining terms under which money or property is transferred from one party to another. Unlike a Gift Letter, which declares that the transfer is not a loan and has no expectation of repayment, a Loan Agreement specifies the conditions under which the loaned amount is to be repaid, including interest rates, payment schedule, and the duration of the loan. This contract establishes a binding obligation for repayment, contrasting with the Gift Letter's purpose to document a no-strings-attached transfer.

When filling out a Gift Letter form, it's essential to navigate the process with care and attention. Here are guidelines to ensure the process is both smooth and compliant.

Do:When it comes to the Gift Letter form, many misunderstandings can lead individuals astray. It's essential to clear up these misconceptions to ensure that both donors and recipients navigate the process smoothly and with full awareness of its implications. Below, several common misconceptions are addressed, shedding light on the realities of using a Gift Letter form.

Only family members can provide gifts requiring a Gift Letter. Contrary to what many believe, gifts can come from various sources, not just immediate family members. The key factor is the lender's policy, which may extend eligibility to distant relatives, fiancés, or even close family friends, provided there's no expected repayment.

All gifts must be disclosed and accompanied by a Gift Letter. Not every gift towards a large purchase, like a home, necessarily requires a Gift Letter. Generally, lenders look for significant, unexplained deposits in your account. Smaller gifts that don't drastically alter your financial picture may not need documentation.

A Gift Letter needs to disclose the source of the donor's funds. This is a common misconception. While a Gift Letter must confirm that the funds are indeed a gift, not a loan, and spell out the donor's name, relationship, and the gift amount, it typically does not require the donor to disclose where their money comes from.

Gifting funds is a way to avoid taxes. While gifting can indeed be a strategy in tax planning, it's oversimplified to say it helps avoid taxes. The IRS has annual and lifetime exclusions for gifts, but gifts exceeding these amounts may require filing a gift tax return, although the tax itself might not always be due.

The recipient is responsible for taxes on gifted amounts. Actually, the responsibility for any applicable gift tax falls on the donor, not the recipient. However, most gifts fall under the annual exclusion limit set by the IRS, meaning no tax is due at all.

Gift Letters are only used for mortgage purposes. While it's true that Gift Letters are commonly associated with real estate transactions, they can also be used for other large gifts requiring formal documentation, such as contributing towards a car or even significant personal loans.

Once a Gift Letter is submitted, the funds are free to use without restriction. While the Gift Letter does indicate that the funds are not to be repaid, lenders may impose certain conditions on how the gift money is used, particularly in real estate transactions. For instance, they may require the funds to be used solely for down payments or closing costs.

Understanding the nuances surrounding the Gift Letter can empower individuals to make informed decisions, ensuring that generosity doesn't inadvertently lead to complications down the road.

When considering the process of utilizing a Gift Letter form, there are several crucial aspects to bear in mind. This document plays a pivotal role in the financial transactions, particularly in instances such as home buying, where proof of non-repayable funds is essential. Here are key takeaways for effectively filling out and using the Gift Letter form:

Failing to thoroughly and accurately complete a Gift Letter form can lead to complications, including tax liabilities or challenges in the approval processes for loans or other financial products. It’s a document that simplifies the process of proving that financial assistance is indeed a gift, making it a critical component in various financial and legal contexts.

Act of Donation of a Movable - The Louisiana Act of Donation form is an invaluable tool for making donations within the family, especially for succession planning.

How to Remove a Property Lien in Texas - State Bar of Texas provided form for legally nullifying a lien against a property after debt settlement.