Fill a Valid IRS 1120 Form

Fill a Valid IRS 1120 Form

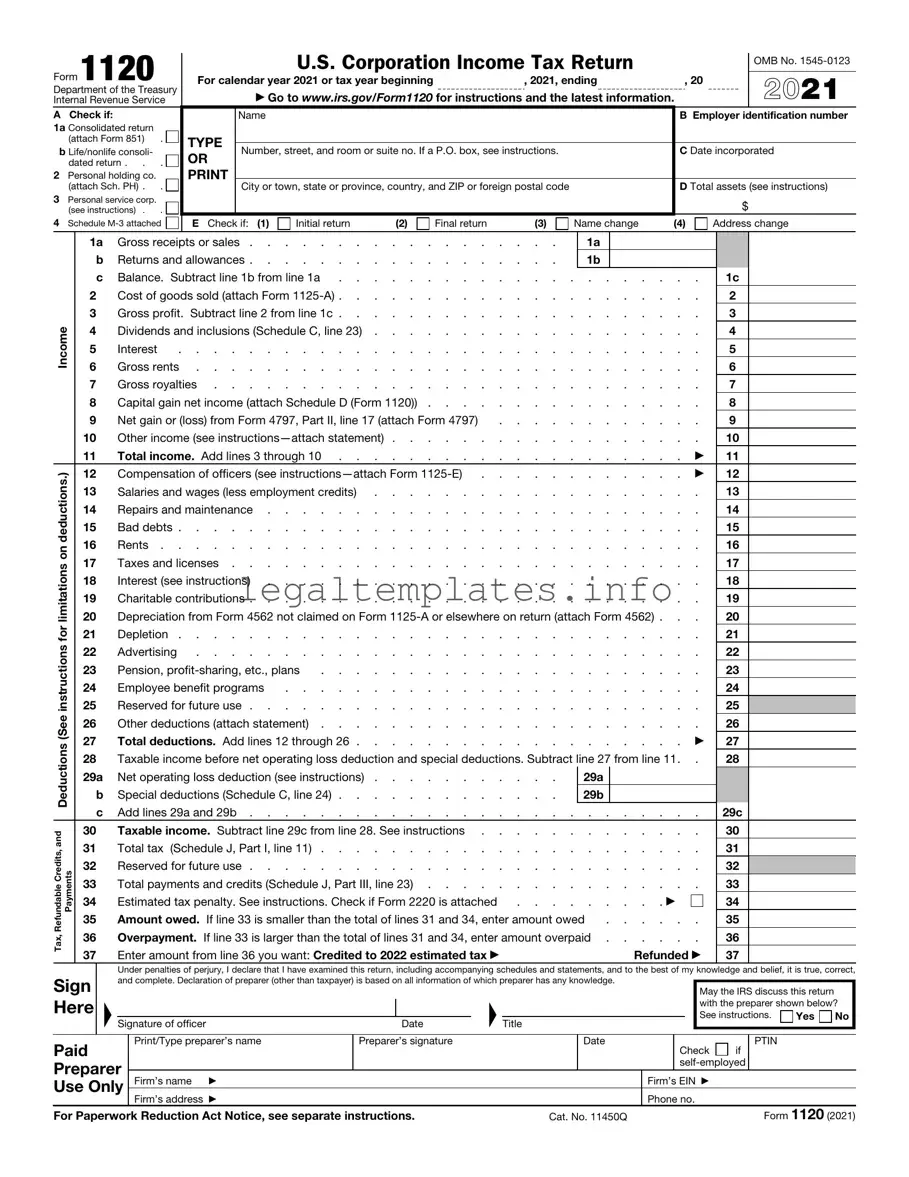

Navigating the complexities of corporate taxes in the United States can seem like a daunting task, especially when it comes to understanding the pivotal documents and forms required for compliance. Among these, the IRS 1120 form stands out as a critical filing requirement for U.S. corporations. This form serves as the primary vehicle through which companies report their income, gains, losses, deductions, and credits to the Internal Revenue Service. Its significance lies not only in its role in determining the income tax liability of a corporation but also in its function as a detailed record of a company’s financial activities over the fiscal year. With sections dedicated to everything from gross receipts to dividends and deductions, the 1120 form provides a comprehensive snapshot of a corporation’s financial health, making it an essential part of the annual tax filing process. For corporate entities aiming to stay in good standing with tax laws, mastering the intricacies of this form is paramount, reinforcing the necessity of a clear and thorough understanding of its components and requirements.

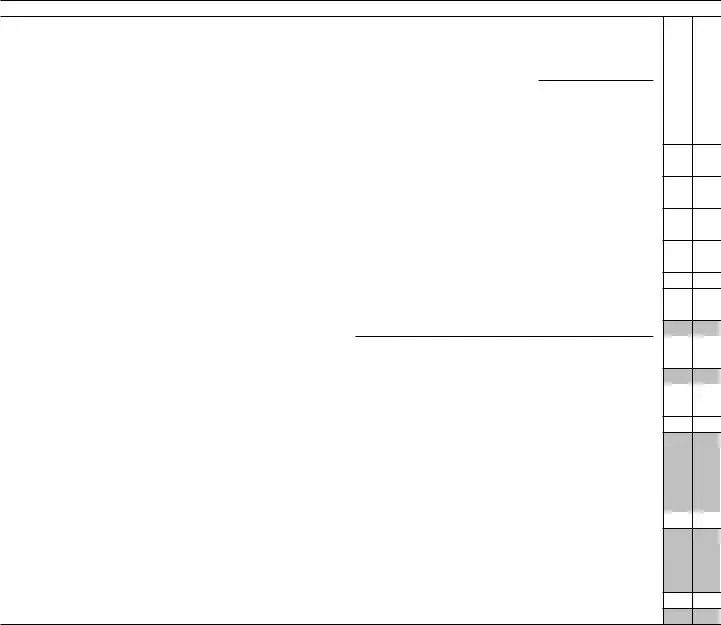

Form 1120

Department of the Treasury

Internal Revenue Service

A Check if:

1a Consolidated return (attach Form 851) .

b Life/nonlife consoli- dated return . . .

2Personal holding co. (attach Sch. PH) . .

3Personal service corp. (see instructions) . .

4 Schedule

|

|

U.S. Corporation Income Tax Return |

|

|

OMB No. |

||||

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

For calendar year 2021 or tax year beginning |

|

, 2021, ending |

, 20 |

|

2021 |

||||

|

▶ Go to www.irs.gov/Form1120 for instructions and the latest information. |

|

|||||||

|

Name |

|

|

|

|

|

B Employer identification number |

||

TYPE |

|

|

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

C Date incorporated |

|||||||

OR |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

D Total assets (see instructions) |

|||||||

|

|

||||||||

|

|

|

|

|

|

|

|

$ |

|

E Check if: (1) |

Initial return |

(2) |

Final return |

(3) |

Name change |

(4) |

Address change |

||

|

1a |

|

Gross receipts or sales |

|

. . . |

. |

|

1a |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

b |

|

Returns and allowances |

|

. . . |

. |

|

1b |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

c |

|

Balance. Subtract line 1b from line 1a |

|

. . . . . . . . . . . . |

1c |

|

|

||||||||||||||||||||

|

2 |

|

|

Cost of goods sold (attach Form |

|

. . . . . . . . . . . . |

2 |

|

|

|

|||||||||||||||||||

|

3 |

|

|

Gross profit. Subtract line 2 from line 1c |

|

. . . . . . . . . . . . |

3 |

|

|

|

|||||||||||||||||||

Income |

4 |

|

|

Dividends and inclusions (Schedule C, line 23) |

|

. . . . . . . . . . . . |

4 |

|

|

|

|||||||||||||||||||

5 |

|

|

Interest |

. . . . . . . . . . . . . . . . . . |

|

. . . . . . . . . . . . |

5 |

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

6 |

|

|

Gross rents |

|

. . . . . . . . . . . . |

6 |

|

|

|

|||||||||||||||||||

|

7 |

|

|

Gross royalties |

|

. . . . . . . . . . . . |

7 |

|

|

|

|||||||||||||||||||

|

8 |

|

|

Capital gain net income (attach Schedule D (Form 1120)) . . . . |

|

. . . . . . . . . . . . |

8 |

|

|

|

|||||||||||||||||||

|

9 |

|

|

Net gain or (loss) from Form 4797, Part II, line 17 (attach Form 4797) |

|

. . . . . . . . . . . . |

9 |

|

|

|

|||||||||||||||||||

|

10 |

|

|

Other income (see |

|

. . . . . . . . . . . . |

10 |

|

|

|

|||||||||||||||||||

|

11 |

|

|

Total income. Add lines 3 through 10 |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

11 |

|

|

|

|||||||||||

deductions.) |

12 |

|

|

Compensation of officers (see |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

12 |

|

|

|

|||||||||||

13 |

|

|

Salaries and wages (less employment credits) |

|

. . . . . . . . . . . . |

13 |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

14 |

|

|

Repairs and maintenance |

|

. . . . . . . . . . . . |

14 |

|

|

|

|||||||||||||||||||

|

15 |

|

|

Bad debts |

|

. . . . . . . . . . . . |

15 |

|

|

|

|||||||||||||||||||

on |

16 |

|

|

Rents |

|

. . . . . . . . . . . . |

16 |

|

|

|

|||||||||||||||||||

17 |

|

|

Taxes and licenses |

|

. . . . . . . . . . . . |

17 |

|

|

|

||||||||||||||||||||

limitations |

|

|

|

|

|

|

|||||||||||||||||||||||

20 |

|

|

Depreciation from Form 4562 not claimed on Form |

20 |

|

|

|

||||||||||||||||||||||

|

18 |

|

|

Interest (see instructions) |

|

. . . . . . . . . . . . |

18 |

|

|

|

|||||||||||||||||||

|

19 |

|

|

Charitable contributions |

|

. . . . . . . . . . . . |

19 |

|

|

|

|||||||||||||||||||

for |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

21 |

|

|

Depletion |

|

. . . . . . . . . . . . |

21 |

|

|

|

||||||||||||||||||||

instructions |

25 |

|

|

Reserved for future use |

|

. . . . . . . . . . . . |

25 |

|

|

|

|||||||||||||||||||

|

22 |

|

|

Advertising |

|

. . . . . . . . . . . . |

22 |

|

|

|

|||||||||||||||||||

|

23 |

|

|

Pension, |

. . . . . . . . . . |

|

. . . . . . . . . . . . |

23 |

|

|

|

||||||||||||||||||

|

24 |

|

|

Employee benefit programs |

. . . . . . . . . . . . |

|

. . . . . . . . . . . . |

24 |

|

|

|

||||||||||||||||||

(See |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 |

|

|

Other deductions (attach statement) |

|

. . . . . . . . . . . . |

26 |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

Deductions |

27 |

|

|

Total deductions. Add lines 12 through 26 |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

27 |

|

|

|

|||||||||||

28 |

|

|

Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11. . |

28 |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||

|

29a |

|

Net operating loss deduction (see instructions) |

|

. . . |

. |

|

29a |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

b |

|

Special deductions (Schedule C, line 24) |

|

. . . |

. |

|

29b |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

c |

|

Add lines 29a and 29b |

|

. . . . . . . . . . . . |

29c |

|

|

||||||||||||||||||||

and |

30 |

|

|

Taxable income. Subtract line 29c from line 28. See instructions . |

|

. . . . . . . . . . . . |

30 |

|

|

|

|||||||||||||||||||

31 |

|

|

Total tax |

(Schedule J, Part I, line 11) |

|

. . . . . . . . . . . . |

31 |

|

|

|

|||||||||||||||||||

Credits,Refundable Payments |

|

|

|

|

|

|

|||||||||||||||||||||||

32 |

|

|

Reserved for future use |

|

. . . . . . . . . . . . |

32 |

|

|

|

||||||||||||||||||||

|

33 |

|

|

Total payments and credits (Schedule J, Part III, line 23) . . . . |

|

. . . . . . . . . . . . |

33 |

|

|

|

|||||||||||||||||||

|

34 |

|

|

Estimated tax penalty. See instructions. Check if Form 2220 is attached |

. . |

. |

. . |

. . |

. |

. ▶ |

|

|

|

34 |

|

|

|

||||||||||||

|

35 |

|

|

Amount owed. If line 33 is smaller than the total of lines 31 and 34, enter amount owed |

. . . . . . |

35 |

|

|

|

||||||||||||||||||||

Tax, |

36 |

|

|

Overpayment. If line 33 is larger than the total of lines 31 and 34, enter amount overpaid |

36 |

|

|

|

|||||||||||||||||||||

37 |

|

|

Enter amount from line 36 you want: Credited to 2022 estimated tax ▶ |

|

|

|

|

|

|

|

Refunded ▶ |

37 |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Sign |

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, |

||||||||||||||||||||||||||

|

|

and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|

|

|

May the IRS discuss this return |

|

||||||||||||||||||||

Here |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

with the preparer shown below? |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions. |

Yes |

No |

||

|

|

|

▲Signature of officer |

|

|

|

Date |

▲ |

|

Title |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

|

Print/Type preparer’s name |

|

|

Preparer’s signature |

|

|

|

|

|

Date |

|

|

|

|

|

Check |

if |

PTIN |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Firm’s name ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s EIN ▶ |

|

|

|

|

|||||||||

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Firm’s address ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Phone no. |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

For Paperwork Reduction Act Notice, see separate instructions. |

|

|

|

Cat. No. 11450Q |

|

|

|

|

|

|

|

Form 1120 (2021) |

|||||||||||||||||

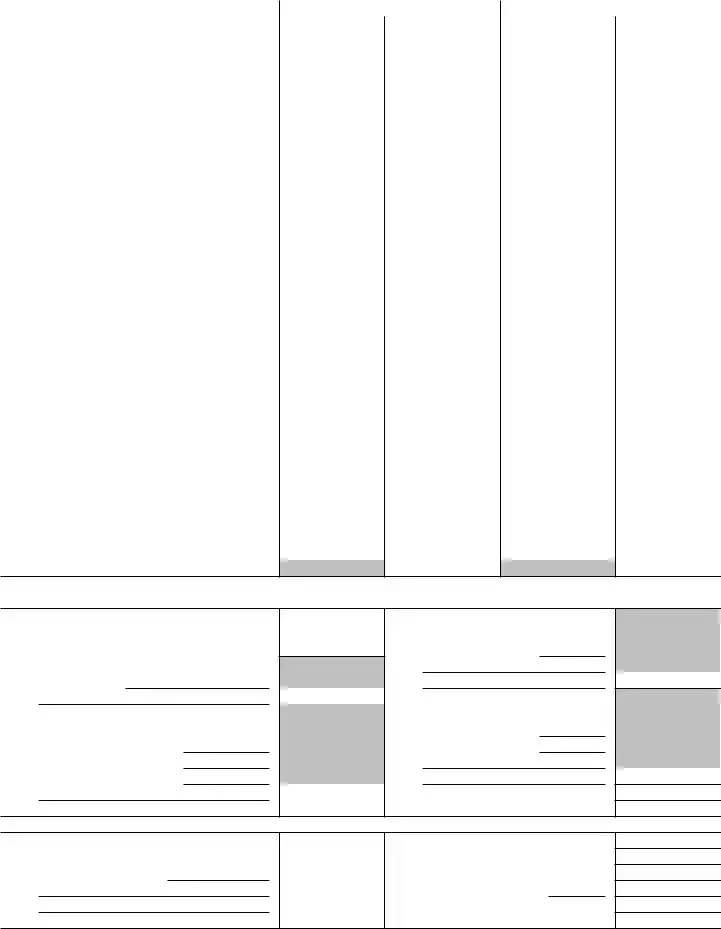

Form 1120 (2021) |

|

|

Page 2 |

|

Schedule C |

Dividends, Inclusions, and Special Deductions (see |

(a) Dividends and |

(b) % |

(c) Special deductions |

|

instructions) |

inclusions |

(a) × (b) |

|

|

|

|||

1Dividends from

stock) |

50 |

2Dividends from

|

stock) |

65 |

|

|

See |

3 |

Dividends on certain |

instructions |

4 |

Dividends on certain preferred stock of |

23.3 |

5 |

Dividends on certain preferred stock of |

26.7 |

6 |

Dividends from |

50 |

7 |

Dividends from |

65 |

8 |

Dividends from wholly owned foreign subsidiaries |

100 |

|

|

See |

9 |

Subtotal. Add lines 1 through 8. See instructions for limitations |

instructions |

10Dividends from domestic corporations received by a small business investment

|

company operating under the Small Business Investment Act of 1958 |

100 |

11 |

Dividends from affiliated group members |

100 |

12 |

Dividends from certain FSCs |

100 |

13

|

corporation (excluding hybrid dividends) (see instructions) |

|

100 |

|

|

14 |

Dividends from foreign corporations not included on line 3, 6, 7, 8, 11, 12, or 13 |

|

|

||

|

(including any hybrid dividends) |

|

|

|

|

15 |

Reserved for future use |

|

|

|

|

16a |

Subpart F inclusions derived from the sale by a controlled foreign corporation (CFC) of |

|

|

||

|

the stock of a |

100 |

|

||

|

(see instructions) |

|

|

||

b |

Subpart F inclusions derived from hybrid dividends of tiered corporations (attach Form(s) |

|

|

||

|

5471) (see instructions) |

|

|

|

|

c |

Other inclusions from CFCs under subpart F not included on line 16a, 16b, or 17 (attach |

|

|

||

|

Form(s) 5471) (see instructions) |

|

|

||

17 |

Global Intangible |

18 |

|

19 |

|

20 |

Other dividends |

21 |

Deduction for dividends paid on certain preferred stock of public utilities . . . . |

22 |

Section 250 deduction (attach Form 8993) |

23Total dividends and inclusions. Add column (a), lines 9 through 20. Enter here and on page 1, line 4 . . . . . . . . . . . . . . . . . . . . . .

24 |

Total special deductions. Add column (c), lines 9 through 22. Enter here and on page 1, line 29b |

Form 1120 (2021)

Form 1120 (2021) |

|

|

|

|

|

Page 3 |

|

Schedule J |

Tax Computation and Payment (see instructions) |

|

|

|

|

|

|

Part |

|

|

|

|

|

||

1 |

Check if the corporation is a member of a controlled group (attach Schedule O (Form 1120)). See instructions |

▶ |

|

|

|||

2 |

Income tax. See instructions |

. . . . |

. . . |

2 |

|

||

3 |

Base erosion minimum tax amount (attach Form 8991) |

. . . . |

. . . |

3 |

|

||

4 |

Add lines 2 and 3 |

. . . . |

. . . |

4 |

|

||

5a |

Foreign tax credit (attach Form 1118) |

5a |

|

|

|

|

|

b |

Credit from Form 8834 (see instructions) |

5b |

|

|

|

|

|

c |

General business credit (attach Form 3800) |

5c |

|

|

|

|

|

d |

Credit for prior year minimum tax (attach Form 8827) |

5d |

|

|

|

|

|

e |

Bond credits from Form 8912 |

5e |

|

|

|

|

|

6 |

Total credits. Add lines 5a through 5e |

. . . . |

. . . |

6 |

|

||

7 |

Subtract line 6 from line 4 |

. . . . |

. . . |

7 |

|

||

8 |

Personal holding company tax (attach Schedule PH (Form 1120)) |

. . . . |

. . . |

8 |

|

||

9a |

Recapture of investment credit (attach Form 4255) |

9a |

|

|

|

|

|

b |

Recapture of |

9b |

|

|

|

|

|

c |

Interest due under the |

|

|

|

|

|

|

|

Form 8697) |

9c |

|

|

|

|

|

d |

Interest due under the |

9d |

|

|

|

|

|

e |

Alternative tax on qualifying shipping activities (attach Form 8902) |

9e |

|

|

|

|

|

f |

Interest/tax due under section 453A(c) and/or section 453(l) |

9f |

|

|

|

|

|

g |

Other (see |

9g |

|

|

|

|

|

10 |

Total. Add lines 9a through 9g |

. . . . |

. . . |

10 |

|

||

11 |

Total tax. Add lines 7, 8, and 10. Enter here and on page 1, line 31 |

. . . . |

. . . |

11 |

|

||

Part

12 Reserved for future use . . . . . . . . . . . . . . . . . . . . . . . . . . .

12

Part

13 |

2020 overpayment credited to 2021 |

. . . . . . . . |

13 |

|

|

||

14 |

2021 estimated tax payments |

. . . . . . . . |

14 |

|

|

||

15 |

2021 refund applied for on Form 4466 |

. . . . . . . . |

15 |

( |

) |

||

16 |

Combine lines 13, 14, and 15 |

. . . . . . . . |

16 |

|

|

||

17 |

Tax deposited with Form 7004 |

. . . . . . . . |

17 |

|

|

||

18 |

Withholding (see instructions) |

. . . . . . . . |

18 |

|

|

||

19 |

Total payments. Add lines 16, 17, and 18 |

. . . . . . . . |

19 |

|

|

||

20 |

Refundable credits from: |

|

|

|

|

|

|

a |

Form 2439 |

|

20a |

|

|

|

|

b |

Form 4136 |

|

20b |

|

|

|

|

c |

Reserved for future use |

|

20c |

|

|

|

|

d |

Other (attach |

|

20d |

|

|

|

|

21 |

Total credits. Add lines 20a through 20d |

. . . . . . . . |

21 |

|

|

||

22 |

Reserved for future use |

. . . . . . . . |

22 |

|

|

||

23 |

Total payments and credits. Add lines 19 and 21. Enter here and on page 1, line 33 . |

. . . . . . . . |

23 |

|

|

||

|

|

|

|

|

|

|

Form 1120 (2021) |

Form 1120 (2021) |

Page 4 |

Schedule K Other Information (see instructions)

1 |

Check accounting method: a |

Cash |

b |

Accrual |

c |

Other (specify) ▶ |

2See the instructions and enter the: a Business activity code no. ▶

b Business activity ▶ c Product or service ▶

3 Is the corporation a subsidiary in an affiliated group or a

If “Yes,” enter name and EIN of the parent corporation ▶

4At the end of the tax year:

aDid any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or

corporation’s stock entitled to vote? If “Yes,” complete Part I of Schedule G (Form 1120) (attach Schedule G) . . . . . .

bDid any individual or estate own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all

classes of the corporation’s stock entitled to vote? If “Yes,” complete Part II of Schedule G (Form 1120) (attach Schedule G) .

5At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of stock entitled to vote of any foreign or domestic corporation not included on Form 851, Affiliations Schedule? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (iv) below.

Yes No

(i)Name of Corporation

(ii)Employer

Identification Number

(if any)

(iii)Country of Incorporation

(iv)Percentage Owned in Voting

Stock

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (iv) below.

(i)Name of Entity

(ii)Employer

Identification Number

(if any)

(iii)Country of Organization

(iv)Maximum

Percentage Owned in Profit, Loss, or Capital

6During this tax year, did the corporation pay dividends (other than stock dividends and distributions in exchange for stock) in

excess of the corporation’s current and accumulated earnings and profits? See sections 301 and 316 . . . . . . . .

If “Yes,” file Form 5452, Corporate Report of Nondividend Distributions. See the instructions for Form 5452. If this is a consolidated return, answer here for the parent corporation and on Form 851 for each subsidiary.

7At any time during the tax year, did one foreign person own, directly or indirectly, at least 25% of the total voting power of all classes of the corporation’s stock entitled to vote or at least 25% of the total value of all classes of the corporation’s stock? .

For rules of attribution, see section 318. If “Yes,” enter:

(a) Percentage owned ▶ |

and (b) Owner’s country ▶ |

(c)The corporation may have to file Form 5472, Information Return of a 25%

8 Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . . . ▶

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

9Enter the amount of

10Enter the number of shareholders at the end of the tax year (if 100 or fewer) ▶

11If the corporation has an NOL for the tax year and is electing to forego the carryback period, check here (see instructions) ▶

If the corporation is filing a consolidated return, the statement required by Regulations section

12Enter the available NOL carryover from prior tax years (do not reduce it by any deduction reported on

page 1, line 29a.) . . . . . . . . . . . . . . . . . . . . . . . . . ▶ $

Form 1120 (2021)

Form 1120 (2021) |

Page 5 |

Schedule K Other Information (continued from page 4)

13 |

Are the corporation’s total receipts (page 1, line 1a, plus lines 4 through 10) for the tax year and its total assets at the end of the |

Yes No |

|

||

|

tax year less than $250,000? |

|

|

If “Yes,” the corporation is not required to complete Schedules L, |

|

|

distributions and the book value of property distributions (other than cash) made during the tax year ▶ $ |

|

14 |

Is the corporation required to file Schedule UTP (Form 1120), Uncertain Tax Position Statement? See instructions . . . . |

|

|

If “Yes,” complete and attach Schedule UTP. |

|

15a |

Did the corporation make any payments in 2021 that would require it to file Form(s) 1099? |

|

b |

If “Yes,” did or will the corporation file required Form(s) 1099? |

|

16During this tax year, did the corporation have an

own stock? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17During or subsequent to this tax year, but before the filing of this return, did the corporation dispose of more than 65% (by value)

of its assets in a taxable,

18Did the corporation receive assets in a section 351 transfer in which any of the transferred assets had a fair market basis or fair

market value of more than $1 million? . . . . . . . . . . . . . . . . . . . . . . . . . . .

19During the corporation’s tax year, did the corporation make any payments that would require it to file Forms 1042 and

20 Is the corporation operating on a cooperative basis?. . . . . . . . . . . . . . . . . . . . . . .

21During the tax year, did the corporation pay or accrue any interest or royalty for which the deduction is not allowed under section

267A? See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If “Yes,” enter the total amount of the disallowed deductions ▶ $

22Does the corporation have gross receipts of at least $500 million in any of the 3 preceding tax years? (See sections 59A(e)(2)

and (3)) . |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

If “Yes,” complete and attach Form 8991.

23Did the corporation have an election under section 163(j) for any real property trade or business or any farming business in effect

|

during the tax year? See instructions |

24 |

Does the corporation satisfy one or more of the following? See instructions |

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense. If “Yes,” complete and attach Form 8990.

25 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

|

If “Yes,” enter amount from Form 8996, line 15 . . . . ▶ $ |

26Since December 22, 2017, did a foreign corporation directly or indirectly acquire substantially all of the properties held directly or indirectly by the corporation, and was the ownership percentage (by vote or value) for purposes of section 7874 greater than 50% (for example, the shareholders held more than 50% of the stock of the foreign corporation)? If “Yes,” list the ownership

percentage by vote and by value. See instructions . . . . . . . . . . . . . . . . . . . . . . .

Percentage: By Vote |

By Value |

Form 1120 (2021)

Form 1120 (2021) |

|

|

|

|

|

|

|

|

|

|

|

|

Page 6 |

||

Schedule L |

|

Balance Sheets per Books |

|

|

Beginning of tax year |

|

|

End of tax year |

|

||||||

|

|

|

Assets |

|

|

|

|

(a) |

|

(b) |

|

(c) |

|

|

(d) |

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

||||

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less allowance for bad debts . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

3 |

Inventories |

|

|

|

|

|

|

|

|

|

|||||

4 |

U.S. government obligations |

. . . . . |

|

|

|

|

|

|

|

|

|

|

|||

5 |

|

|

|

|

|

|

|

|

|

|

|||||

6 |

Other current assets (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

||||

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

||||

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

||||

10a |

Buildings and other depreciable assets . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depreciation . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

11a |

Depletable assets |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depletion . . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

|

|||||

13a |

Intangible assets (amortizable only) |

. . . |

|

|

|

|

|

|

|

|

|

|

|||

b |

Less accumulated amortization . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

15 |

Total assets |

|

|

|

|

|

|

|

|

|

|||||

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|||||

16 |

Accounts payable |

|

|

|

|

|

|

|

|

|

|

||||

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

|

|

||||

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

|

|

||||

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

|

|

||||

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

|

|

||||

22 |

Capital stock: |

a Preferred stock . . . . |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

b Common stock . . . . |

|

|

|

|

|

|

|

|

|

|

||

23 |

Additional |

|

|

|

|

|

|

|

|

|

|

||||

24 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

25 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

26 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

27 |

Less cost of treasury stock |

|

|

|

|

( |

) |

|

|

( |

) |

||||

28 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

|

|||||

Schedule

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books |

7 |

Income recorded on books this year |

|

2 |

Federal income tax per books |

|

|

not included on this return (itemize): |

3 |

Excess of capital losses over capital gains . |

|

|

|

4Income subject to tax not recorded on books this year (itemize):

|

|

|

8 |

|

Deductions on this return not charged |

5 |

Expenses recorded on books this year not |

|

against book income this year (itemize): |

||

|

deducted on this return (itemize): |

a |

Depreciation . . $ |

||

a |

Depreciation . . . . $ |

b |

Charitable contributions $ |

||

bCharitable contributions . $

cTravel and entertainment . $

|

|

|

9 |

Add lines 7 and 8 |

6 |

Add lines 1 through 5 |

10 |

Income (page 1, line |

|

Schedule

1 |

Balance at beginning of year |

5 |

Distributions: a Cash |

||

2 |

Net income (loss) per books |

|

|

|

b Stock . . . . |

3 |

Other increases (itemize): |

|

|

|

c Property . . . . |

|

|

|

6 |

Other decreases (itemize): |

|

|

|

|

7 |

Add lines 5 and 6 |

|

4 |

Add lines 1, 2, and 3 |

8 |

Balance at end of year (line 4 less line 7) |

||

Form 1120 (2021)

| Fact Name | Description |

|---|---|

| Form Designation | The IRS Form 1120 is designated for C Corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service. |

| Purpose | Its primary purpose is to determine the entity's income tax liability. |

| Filing Requirement | All U.S. based C Corporations are required to file Form 1120, unless they are exempt under specific IRS rules. |

| Due Date | The form is typically due by April 15 following the end of the corporation's fiscal year. For corporations with a fiscal year ending on December 31, the due date is April 15 of the following year. |

| Extension Availability | Corporations can apply for a six-month extension to file Form 1120, which moves the deadline to October 15th. |

| Penalties for Late Filing | Failure to file or late filing may result in penalties, which are calculated based on the tax due and the length of the delay. |

| State Variability | While Form 1120 is a federal form, many states require corporations to file a separate income tax return, governed by individual state laws and regulations. |

After a corporation has compiled all necessary financial statements and reports for the year, the next step involves filing an IRS 1120 form. This document, crucial for corporate tax compliance, reports the income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Completing this form accurately ensures the corporation meets its tax obligations and avoids potential penalties. Here are the sequential steps to guide you through the process of filling out the IRS 1120 form.

Once the IRS 1120 form is properly submitted, your corporation has fulfilled a critical component of its annual tax obligations. It is advisable to consult with a tax professional or accountant during this process to ensure accuracy and compliance with current tax laws and regulations. This professional guidance can provide peace of mind and prevent future complications with the Internal Revenue Service.

What is the IRS 1120 form used for?

The IRS form 1120 is utilized by corporations to report their income, gains, losses, deductions, and credits, as well as to calculate their federal income tax liability. It is a critical tax document for C corporations operating in the United States, distinguishing their tax responsibilities from their shareholders.

Who needs to file IRS Form 1120?

All domestic corporations, including C corporations, are required to file the IRS Form 1120. This is irrespective of whether they have taxable income or not during the tax year. However, S corporations, which pay taxes differently, must file Form 1120S instead.

When is the deadline to file Form 1120?

Typically, Form 1120 must be filed by the 15th day of the fourth month following the end of the corporation's fiscal year. For corporations that follow the calendar year, the deadline is April 15th. If the due date falls on a weekend or a legal holiday, the deadline is shifted to the next business day.

What information do I need to complete Form 1120?

Completing Form 1120 requires detailed financial information about the corporation. This includes gross income, cost of goods sold, dividends, interest, rents, royalties, and all deductions such as salaries, taxes, and interest. Additionally, information on foreign transactions, loans to shareholders, and officer compensation is necessary.

Are there penalties for filing Form 1120 late?

Yes, corporations that fail to file Form 1120 by the due date, including extensions, may face penalties. The penalty generally equates to 5% of the unpaid tax for each month or part of a month that the return is late, not exceeding 25% of the unpaid tax. Furthermore, interest is charged on any unpaid tax from the due date until the tax is paid in full.

Can I file Form 1120 electronically?

Yes, the IRS encourages corporations to file Form 1120 electronically for faster processing. Electronic filing is available through IRS-approved software providers. Filing electronically also allows for quicker confirmation that the IRS has received the form. Additionally, corporations with total assets of $10 million or more are required to file electronically.

What happens if I make a mistake on Form 1120?

If you discover an error after submitting Form 1120, you should file an amended return using Form 1120X as soon as possible. The filed amendment will allow you to correct errors related to income, deductions, credits, or tax calculations. It's important to address errors promptly to avoid potential interest and penalties.

Filling out the IRS 1120 form, the U.S. Corporation Income Tax Return, requires careful attention to detail and a clear understanding of taxable income, deductions, and credits to accurately report a corporation's financial activities for the year. Mistakes made during this process can lead to audits, penalties, or missed opportunities for reduced tax liabilities. Here are nine common errors to watch out for:

One frequent mistake is incorrectly reporting income. Businesses sometimes report gross receipts instead of net income, or they fail to account for all sources of income, including interest and dividends. It's essential to carefully review all financial records and ensure the income is accurately reported according to IRS guidelines.

Another common error involves misclassifying expenses. Businesses might incorrectly categorize capital expenditures as deductible expenses or vice versa. It’s important to understand the difference between capital expenditures (which must be capitalized and depreciated over time) and deductible business expenses to ensure accurate reporting.

Failing to properly report shareholder compensation is another mistake. Compensation paid to shareholders who work for the corporation can be deductible, but it must be reasonable and for services rendered. Overcompensating shareholders can attract IRS scrutiny, especially if the compensation significantly exceeds industry norms.

A significant number of corporations neglect to claim all available deductions and credits. From research and development credits to deductions for charitable contributions, these benefits can significantly reduce taxable income, but they are often overlooked or misunderstood.

Incorrectly calculating depreciation is a common error that can lead to overstatements or understatements of expenses. The IRS has specific methods and schedules for depreciation, and it’s crucial to follow these guidelines to accurately calculate depreciation deductions.

Omitting or inaccurately completing schedules and attachments can also lead to problems. The IRS 1120 form requires various schedules and attachments depending on the corporation's activities, assets, and transactions. Missing information can trigger IRS inquiries or audits.

Using the wrong tax year or filing status can also be problematic. It's vital to ensure that the form corresponds to the correct tax year and that the corporation’s filing status is accurately reflected.

Another mistake is failing to sign and date the form. This might seem trivial, but an unsigned tax return is considered incomplete by the IRS and can delay processing or lead to penalties.

Finally, errors in calculation are not uncommon and can significantly impact the tax owed or refund due. It is advisable to double-check all mathematical computations or, better yet, use tax preparation software or consult with a tax professional to minimize the likelihood of errors.

Avoiding these mistakes requires a thorough understanding of tax laws as they apply to corporations, meticulous record-keeping, and attention to detail. When in doubt, consulting a tax professional can help ensure the accuracy and completeness of the IRS 1120 form.

When filing the IRS 1120 form, corporations are required to provide additional documentation that supports the information within the form itself. The 1120 form, utilized by domestic corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service, often necessitates supplemental forms and documents to provide a comprehensive view of the corporation's financial status. These additional documents play a crucial role in ensuring accuracy and compliance with federal tax laws.

In addition to the IRS 1120 form, these documents collectively contribute to a thorough disclosure of a corporation's operating results and financial position. Each plays a specific role in clarifying different aspects of business operations, assets, and liabilities. Properly completing and submitting these forms is integral to fulfilling corporate tax obligations and avoiding potential penalties for non-compliance. Ensuring all relevant documents accompany the IRS 1120 form helps corporations maintain transparency and adhere to U.S. tax regulations.

The IRS 1120 form, utilized by corporations to report their income, deductions, and credits to the Internal Revenue Service (IRS), shares similarities with several other tax documents. Each serves a unique purpose but parallels can be drawn in their use for reporting financial information to the IRS or providing a structured way to calculate taxes owed.

One such document is the IRS 1040 form, the standard federal income tax form used by individuals. Both the 1120 and 1040 forms are essential tools for reporting annual income. While 1120 is specifically for corporations, 1040 is designed for individual taxpayers. Both forms assist in calculating the amount of tax owed based on the income reported, though their deductions and credits vary to cater to their respective filers.

Similarly, the IRS 1120-S form is closely related to the 1120 form but is tailored for S corporations. S corporations elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. The 1120-S includes schedules that shareholders use to report their share of the corporation's income or loss. The parallel lies in the purpose both forms serve in reporting income and deductions, but they differ in their tax treatment and the type of entity they are designed for.

The 1065 form is another document that resonates with the 1120 form, designed for partnerships. It reports the income, deductions, gains, losses, etc., of a partnership but does not pay income tax itself. Instead, profits and losses are passed through to the partners. The connection between the 1120 and 1065 forms is their role in reporting business income; however, they cater to different types of business structures (corporations vs. partnerships).

Similarities can also be found with the Schedule K-1, which is a component of the 1065 form. The Schedule K-1 documents the distribution of income, losses, and dividends to partners or S corporation shareholders. Like the 1120, which reports a corporation's income and losses, the Schedule K-1 ensures that the business's financial activities are communicated to the IRS and properly allocated to the individuals involved.

The IRS 990 form, required for nonprofit organizations, echoes the purpose of the 1120 form in reporting income and expenses. However, the 990 serves tax-exempt entities by detailing their financial activities, ensuring compliance with the conditions of their tax-exempt status. Both forms are critical for their respective entities in maintaining transparency with the IRS about their annual operations.

Engagement with the 940 form, which is used by employers to report annual Federal Unemployment Tax Act (FUTA) tax, shares a procedural connection to the 1120 form. Both require annual filing and involve calculating taxes owed to the federal government, albeit for different taxes and purposes. The 940 form specifically addresses unemployment tax contributions, highlighting the employer's financial obligations beyond income tax.

Last but not least, the 1099 form series, which reports various types of income from non-employment-related sources, shares a fundamental linkage with the 1120 in the overarching theme of tax reporting. While 1099 forms are typically issued by businesses to report payments made to independent contractors, interest, dividends, and other types of income, they complement the reporting process by highlighting additional income streams that may affect the tax calculations of individuals and entities.

Filling out the IRS 1120 form, the U.S. Corporation Income Tax Return, is an important task for corporations in the United States. It's essential for corporations to accurately report their annual income, expenses, and other financial information. Below are ten do’s and don’ts to keep in mind when completing this form:

Do:The IRS 1120 form, commonly understood as the U.S. Corporation Income Tax Return, is a critical document for corporations within the United States. Nevertheless, misconceptions frequently arise, leading to confusion about its preparation and the implications for corporations. To clarify, it's essential to debunk these myths comprehensively.

Misconception 1: Only Large Corporations Need to File Form 1120

Contrary to popular belief, not only large corporations are required to file IRS Form 1120. In reality, the IRS mandates every C corporation, regardless of size, to file this form. This includes corporations that might not have engaged in any business activities during the tax year.

Misconception 2: Filing Form 1120 Extends to S Corporations

This is incorrect. S Corporations are generally exempt from filing Form 1120, as they instead file Form 1120S, a variant tailored for S Corporation reporting. The distinction lies in their tax treatment, with S Corporations allowing income to pass through to shareholders to be taxed at individual rates.

Misconception 3: Form 1120 Is Purely for Reporting Income

While reporting income is a significant element, Form 1120 encompasses more. Deductions, credits, and other financial details relevant to a corporation’s tax obligations are also crucial components. The form serves to provide a comprehensive overview of a corporation's financial status.

Misconception 4: Penalties for Late Filing Are Negligible

This misunderstanding can lead to detrimental financial repercussions. The IRS enforces strict penalties for late filing of Form 1120, which can accumulate rapidly, amounting to substantial sums. The penalties are essentially designed to encourage timely compliance.

Misconception 5: All Corporations Pay a Flat Tax Rate

Although the U.S. corporate tax regime underwent significant changes with the Tax Cuts and Jobs Act of 2017, instituting a flat federal corporate income tax rate, corporations may still face different effective tax rates based on their eligible deductions and credits. Thus, the notion of a universally applied flat tax rate does not capture the complete tax obligation picture.

Misconception 6: Electronic Filing Is Optional

The IRS has made electronic filing (e-filing) mandatory for most corporations, especially those with assets above a certain threshold. This measure not only expedites the processing of returns but also enhances the efficiency and accuracy of tax administration.

Misconception 7: The Same Information from Last Year Can Be Reused

While prior year forms can serve as helpful references, each year's form must accurately reflect the current year's financial activities and tax laws, which can change annually. Recycling information without validation can lead to errors and possible penalties.

Misconception 8: Only CPA-Accredited Professionals Can File Form 1120

Although it's advisable to seek professional assistance for filing complex tax forms, it's not a mandatory requirement. Corporations may file Form 1120 on their own, provided they possess the requisite knowledge and understanding of the tax laws applicable to their situation.

Misconception 9: Amended Returns Are Discouraged

The IRS allows, and in some cases requires, corporations to file amended returns using Form 1120X in the event of recognizing errors or omissions on originally filed returns. This process is crucial for maintaining compliance and ensuring accuracy in tax reporting.

Demystifying these misconceptions about the IRS 1120 form can alleviate undue stress and complications for corporations endeavoring to fulfill their tax obligations. With accurate information and diligence, navigating the intricacies of corporate tax reporting becomes a more manageable task.

The IRS 1120 form, used by corporations to file their income tax returns, presents several key points that should be understood when preparing and submitting this document. Here are ten key takeaways for those navigating this form:

Understanding these points can simplify the process of completing and filing the IRS 1120 form, helping corporations meet their tax obligations accurately and efficiently.

No Trespassing Letter to Neighbor - Explicit warning issued by a property owner or authorized representative to an individual, specifying that entrance onto the property is strictly forbidden.

Da Form 4886 - The DA Form 4986 underscores the importance of personal property accountability within the military community.

Make Ready Technician - Supports property managers in delivering well-maintained and appealing rental units by covering extensive inspection points from entrance to kitchen.