Fill a Valid IRS 2553 Form

Fill a Valid IRS 2553 Form

For businesses operating within the United States, navigating the complexities of tax regulations is a crucial aspect of managing operations efficiently. Among the myriad of forms and documents, the IRS 2553 form stands out for businesses that choose to be treated as an S corporation, offering them the possibility to enjoy certain tax benefits. This election allows businesses to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. Shareholders report the flow-through of income and losses on their personal tax returns and are assessed tax at their individual income tax rates. This setup can result in significant tax savings, especially for small businesses. However, accurately completing and filing this form within the specific time frame required by the IRS is essential for businesses aiming to capitalize on this election. The form itself requires information about the corporation’s name, address, the tax year, and consent statements from all shareholders, ensuring every shareholder agrees to the S corporation election. This election not only influences a corporation's federal tax obligations but also how it is perceived in the eyes of the law and its operational flexibility.

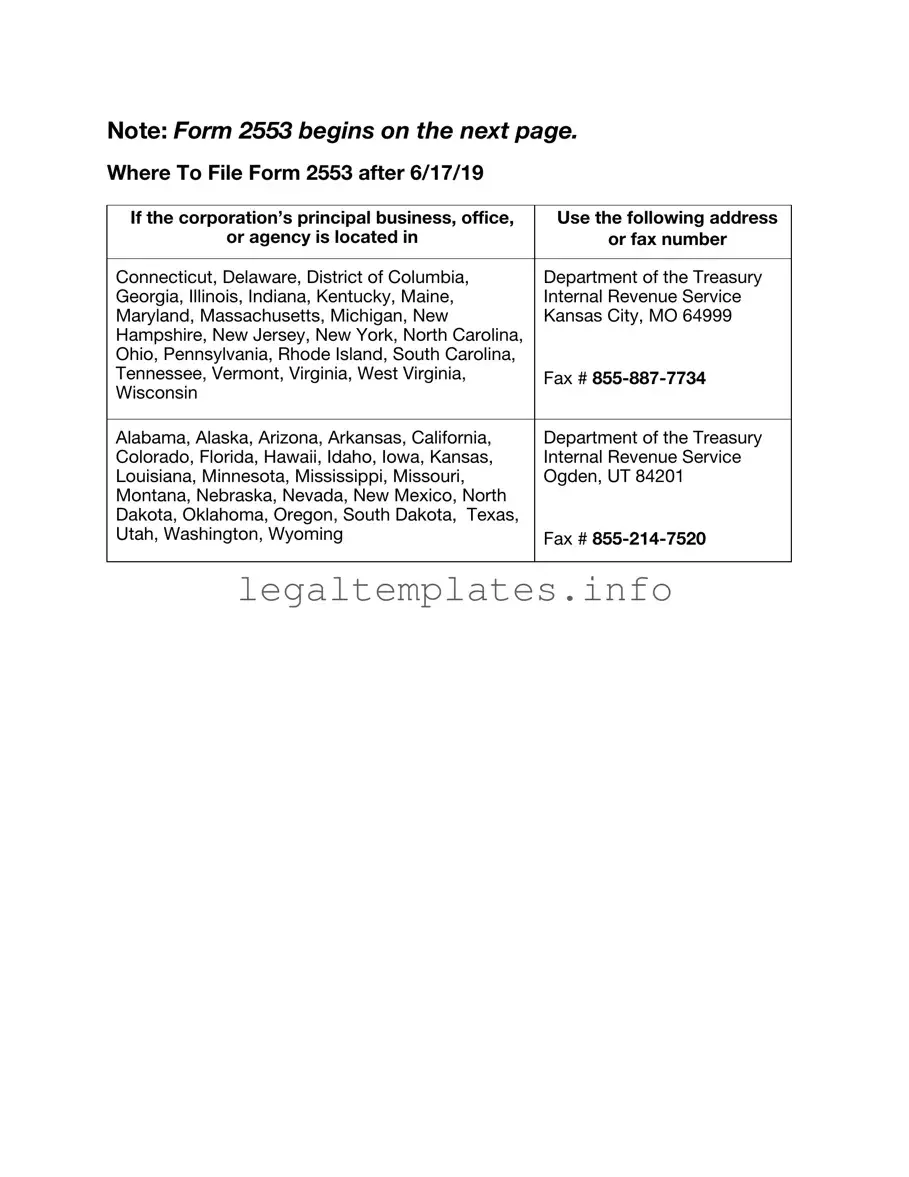

Note: Form 2553 begins on the next page.

Where To File Form 2553 after 6/17/19

If the corporation’s principal business, office, |

Use the following address |

or agency is located in |

or fax number |

|

|

Connecticut, Delaware, District of Columbia, |

Department of the Treasury |

Georgia, Illinois, Indiana, Kentucky, Maine, |

Internal Revenue Service |

Maryland, Massachusetts, Michigan, New |

Kansas City, MO 64999 |

Hampshire, New Jersey, New York, North Carolina, |

|

Ohio, Pennsylvania, Rhode Island, South Carolina, |

|

Tennessee, Vermont, Virginia, West Virginia, |

Fax # |

Wisconsin |

|

|

|

Alabama, Alaska, Arizona, Arkansas, California, |

Department of the Treasury |

Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, |

Internal Revenue Service |

Louisiana, Minnesota, Mississippi, Missouri, |

Ogden, UT 84201 |

Montana, Nebraska, Nevada, New Mexico, North |

|

Dakota, Oklahoma, Oregon, South Dakota, Texas, |

|

Utah, Washington, Wyoming |

Fax # |

|

|

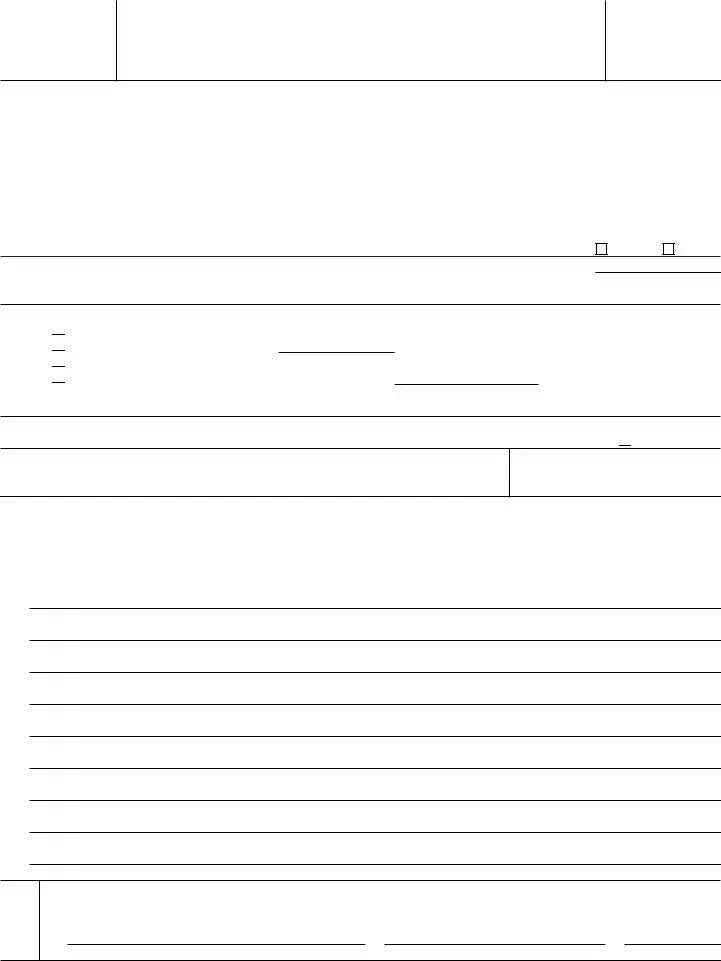

Form 2553

(Rev. December 2017)

Department of the Treasury Internal Revenue Service

Election by a Small Business Corporation

(Under section 1362 of the Internal Revenue Code)

(Including a late election filed pursuant to Rev. Proc.

▶You can fax this form to the IRS. See separate instructions.

▶Go to www.irs.gov/Form2553 for instructions and the latest information.

OMB No.

Note: This election to be an S corporation can be accepted only if all the tests are met under Who May Elect in the instructions, all shareholders have signed the consent statement, an officer has signed below, and the exact name and address of the corporation (entity) and other required form information have been provided.

Part I |

|

Election Information |

|

|

|

|

|

|

|

Name (see instructions) |

A Employer identification number |

||

Type |

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

B Date incorporated |

|

|||

or |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

City or town, state or province, country, and ZIP or foreign postal code |

C State of incorporation |

|

|||

|

|

|

|

|||

|

|

|

|

|

|

|

D |

Check |

the applicable box(es) if the corporation (entity), after applying for the EIN shown in A above, changed its |

name or |

address |

||

EElection is to be effective for tax year beginning (month, day, year) (see instructions) . . . . . . ▶

Caution: A corporation (entity) making the election for its first tax year in existence will usually enter the beginning date of a short tax year that begins on a date other than January 1.

FSelected tax year:

(1) Calendar year

Calendar year

(2) Fiscal year ending (month and day) ▶

Fiscal year ending (month and day) ▶

(3)

(4)

If box (2) or (4) is checked, complete Part II.

GIf more than 100 shareholders are listed for item J (see page 2), check this box if treating members of a family as one shareholder results in no more than 100 shareholders (see test 2 under Who May Elect in the instructions) ▶

HName and title of officer or legal representative whom the IRS may call for more information

Telephone number of officer or legal representative

IIf this S corporation election is being filed late, I declare I had reasonable cause for not filing Form 2553 timely. If this late election is being made by an entity eligible to elect to be treated as a corporation, I declare I also had reasonable cause for not filing an entity classification election timely and the representations listed in Part IV are true. See below for my explanation of the reasons the election or elections were not made on time and a description of my diligent actions to correct the mistake upon its discovery. See instructions.

|

Under penalties of perjury, I declare that I have examined this election, including accompanying documents, and, to the best of my |

||

Sign knowledge and belief, the election contains all the relevant facts relating to the election, and such facts are true, correct, and complete. |

|||

Here |

▲Signature of officer |

|

|

|

Title |

Date |

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 18629R |

Form 2553 (Rev. |

|

Form 2553 (Rev. |

Page 2 |

Name |

Employer identification number |

Part I Election Information (continued) Note: If you need more rows, use additional copies of page 2.

J

Name and address of each

shareholder or former shareholder required to consent to the election.

(see instructions)

K

Shareholder’s Consent Statement

Under penalties of perjury, I declare that I consent to the election of the

Signature |

Date |

L

Stock owned or

percentage of ownership

(see instructions)

Number of |

|

shares or |

|

percentage |

Date(s) |

of ownership |

acquired |

M |

|

Social security |

|

number or |

N |

employer |

Shareholder’s |

identification |

tax year ends |

number (see |

(month and |

instructions) |

day) |

Form 2553 (Rev.

Form 2553 (Rev. |

Page 3 |

|

Name |

|

Employer identification number |

|

|

|

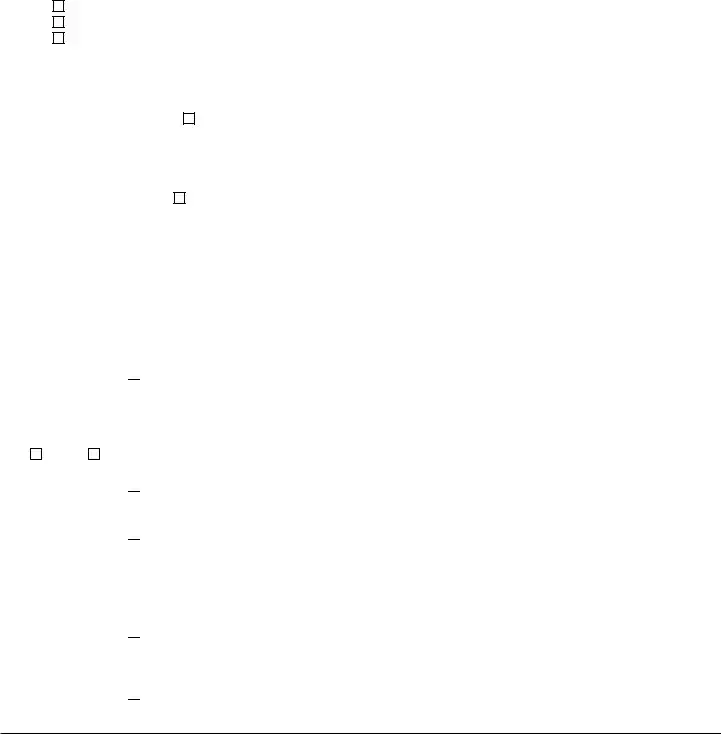

Part II |

Selection of Fiscal Tax Year (see instructions) |

|

Note: All corporations using this part must complete item O and item P, Q, or R. |

|

|

O Check the applicable box to indicate whether the corporation is: |

|

|

1. |

A new corporation adopting the tax year entered in item F, Part I. |

|

2. |

An existing corporation retaining the tax year entered in item F, Part I. |

|

3. |

An existing corporation changing to the tax year entered in item F, Part I. |

|

PComplete item P if the corporation is using the automatic approval provisions of Rev. Proc.

1. Natural Business Year ▶ |

I represent that the corporation is adopting, retaining, or changing to a tax year that qualifies |

as its natural business year (as defined in section 5.07 of Rev. Proc.

2. Ownership Tax Year ▶ |

I represent that shareholders (as described in section 5.08 of Rev. Proc. |

than half of the shares of the stock (as of the first day of the tax year to which the request relates) of the corporation have the same tax year or are concurrently changing to the tax year that the corporation adopts, retains, or changes to per item F, Part I, and that such tax year satisfies the requirement of section 4.01(3) of Rev. Proc.

Note: If you do not use item P and the corporation wants a fiscal tax year, complete either item Q or R below. Item Q is used to request a fiscal tax year based on a business purpose and to make a

QBusiness

1. Check here ▶  if the fiscal year entered in item F, Part I, is requested under the prior approval provisions of Rev. Proc.

if the fiscal year entered in item F, Part I, is requested under the prior approval provisions of Rev. Proc.

Yes |

No |

2.Check here ▶

to show that the corporation intends to make a

to show that the corporation intends to make a

3.Check here ▶

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event (1) the corporation’s business purpose request is not approved and the corporation makes a

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event (1) the corporation’s business purpose request is not approved and the corporation makes a

RSection 444

1.Check here ▶

to show that the corporation will make, if qualified, a section 444 election to have the fiscal tax year shown in item F, Part I. To make the election, you must complete Form 8716, Election To Have a Tax Year Other Than a Required Tax Year, and either attach it to Form 2553 or file it separately.

to show that the corporation will make, if qualified, a section 444 election to have the fiscal tax year shown in item F, Part I. To make the election, you must complete Form 8716, Election To Have a Tax Year Other Than a Required Tax Year, and either attach it to Form 2553 or file it separately.

2.Check here ▶

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event the corporation is ultimately not qualified to make a section 444 election.

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event the corporation is ultimately not qualified to make a section 444 election.

Form 2553 (Rev.

Form 2553 (Rev. |

Page 4 |

Name |

Employer identification number |

Part III Qualified Subchapter S Trust (QSST) Election Under Section 1361(d)(2)* Note: If you are making more than

one QSST election, use additional copies of page 4.

Income beneficiary’s name and address

Social security number

Trust’s name and address

Employer identification number

Date on which stock of the corporation was transferred to the trust (month, day, year) . . . . . . . . ▶

In order for the trust named above to be a QSST and thus a qualifying shareholder of the S corporation for which this Form 2553 is filed, I hereby make the election under section 1361(d)(2). Under penalties of perjury, I certify that the trust meets the definitional requirements of section 1361(d)(3) and that all other information provided in Part III is true, correct, and complete.

Signature of income beneficiary or signature and title of legal representative or other qualified person making the election |

|

Date |

*Use Part III to make the QSST election only if stock of the corporation has been transferred to the trust on or before the date on which the corporation makes its election to be an S corporation. The QSST election must be made and filed separately if stock of the corporation is transferred to the trust after the date on which the corporation makes the S election.

Part IV Late Corporate Classification Election Representations (see instructions)

If a late entity classification election was intended to be effective on the same date that the S corporation election was intended to be effective, relief for a late S corporation election must also include the following representations.

1The requesting entity is an eligible entity as defined in Regulations section

2The requesting entity intended to be classified as a corporation as of the effective date of the S corporation status;

3The requesting entity fails to qualify as a corporation solely because Form 8832, Entity Classification Election, was not timely filed under Regulations section

4The requesting entity fails to qualify as an S corporation on the effective date of the S corporation status solely because the S corporation election was not timely filed pursuant to section 1362(b); and

5a The requesting entity timely filed all required federal tax returns and information returns consistent with its requested classification as an S corporation for all of the years the entity intended to be an S corporation and no inconsistent tax or information returns have been filed by or with respect to the entity during any of the tax years, or

bThe requesting entity has not filed a federal tax or information return for the first year in which the election was intended to be effective because the due date has not passed for that year’s federal tax or information return.

Form 2553 (Rev.

| Fact Number | Description |

|---|---|

| 1 | The IRS Form 2553 is used by businesses to elect S corporation status. |

| 2 | It must be filed within two months and 15 days after the beginning of the tax year the election is to take effect. |

| 3 | Only corporations and certain limited liability companies (LLCs) can use this form. |

| 4 | To qualify for S corporation status, the company must meet specific IRS requirements, such as having only allowable shareholders and a single class of stock. |

| 5 | All shareholders must sign the form, indicating their consent to the election. |

| 6 | The form requires detailed information about the corporation, including its name, address, and employer identification number (EIN). |

| 7 | Electing S corporation status changes how a corporation is taxed, with profits and losses flowing through to shareholders' personal tax returns. |

| 8 | If the form is filed late, relief provisions exist but require the company to explain why it failed to file on time. |

| 9 | After submitting Form 2553, the IRS will send a letter confirming whether the election has been accepted or not. |

| 10 | State-specific requirements for S corporation status may vary, requiring additional forms or filings with state tax authorities. |

Completing the IRS Form 2553 is a critical step for businesses choosing to be taxed as an S corporation, which may offer several tax advantages over other forms of business taxation. This designation allows profits, and some losses, to be passed directly to owners' personal income without being subject to corporate tax rates, potentially leading to significant tax savings. However, navigating the process requires careful attention to detail to ensure all the information is accurate and complete. The following steps provide a straightforward guide to filling out the form, ensuring businesses can successfully apply for S corporation status.

After the Form 2553 is submitted, the corporation will wait for the IRS to process the election. This process can take several weeks. Upon approval, the IRS will send a confirmation letter, indicating the corporation is now recognized as an S corporation for tax purposes. It's essential to adhere to all IRS regulations and filing requirements moving forward to maintain this status. Should the IRS require further information or clarification, it is important to respond promptly to ensure the election remains in good standing. This transition marks a significant step in the corporation’s journey, potentially unlocking favorable tax treatment and influencing its growth strategies.

What is the IRS 2553 Form?

The IRS 2553 Form, also known as the Election by a Small Business Corporation form, is used by small businesses to request S corporation status for tax purposes. By electing to be treated as an S corporation, companies can pass corporate income, losses, deductions, and credits directly to their shareholders to be taxed at individual rates, thereby avoiding double taxation.

Who can file Form 2553?

Only certain entities can file Form 2553. These include domestic corporations and Limited Liability Companies (LLCs) that have made an election to be treated as a corporation. The entity must meet the IRS's requirements to qualify as a small business corporation, including having a permissible number of shareholders, having only allowable shareholders (which include individuals, certain trusts, and estates but not partnerships or non-resident alien shareholders), and having only one class of stock.

When should Form 2553 be filed?

Form 2553 must be filed no later than two months and 15 days after the beginning of the tax year the election is to take effect. Alternatively, it can be filed any time during the tax year preceding the tax year it is to take effect. For an election to be effective for the current tax year, the form must be filed by the aforementioned deadline. Late elections may still be accepted if the corporation can show that the failure to file on time was due to reasonable cause.

How to file Form 2553?

Form 2553 can be filed via mail or fax. The specific mailing address or fax number depends on the state where the business's principal business, office, or agency is located. The form requires comprehensive information about the corporation, including its name, address, employer identification number (EIN), and the tax year for which the election applies. Additionally, all shareholders must consent to the election by signing the form.

Can Form 2553 be filed electronically?

As of the last known update, Form 2553 cannot be filed electronically. It must be submitted through mail or fax, following the instructions provided by the IRS for the specific filing addresses or fax numbers applicable to your entity's location.

What happens after Form 2553 is filed?

After Form 2553 is filed, the IRS will process the election and send a letter of acceptance or rejection. Acceptance letters confirm the S corporation status and its effective date. If the form is rejected, the letter will explain the reasons for rejection, and entities may have the opportunity to address any issues and resubmit the form.

Are there any deadlines for the IRS to respond to a Form 2553 filing?

The IRS does not have a fixed deadline to respond to a Form 2553 filing. However, it typically takes around 60 days to receive a response. It is advisable to call the IRS if a confirmation letter has not been received within this timeframe to check on the status of the filing.

What are the common mistakes to avoid when filing Form 2553?

Common mistakes include not obtaining all required shareholder signatures, incorrect or incomplete information about the corporation, filing the form late without a reason that meets the IRS's reasonable cause criteria, and not using the form's most current version. Ensuring accuracy and completeness when filing can help avoid processing delays or rejections.

Can the S corporation election be terminated or revoked?

Yes, an S corporation status can be terminated or revoked either voluntarily by the shareholders or involuntarily by failing to meet the IRS's eligibility criteria. To revoke the election voluntarily, a statement must be filed with the IRS indicating the desire to revoke the election, signed by shareholders holding more than 50% of the shares. There are specific rules and implications for termination, so consultation with a tax advisor is recommended.

Is there any relief available for entities that miss the filing deadline?

The IRS provides relief for entities that miss the filing deadline under certain conditions. If an entity can show that the failure to file on time was due to reasonable cause, the IRS may allow a late election. Detailed instructions for requesting late election relief are outlined in the IRS's regulations and revenue procedures related to Form 2553.

Filling out the IRS 2553 form, required for small businesses electing to be taxed as an S-corporation, often includes errors that can lead to processing delays or even rejections. One common mistake is inaccurate or incomplete information. When businesses overlook details such as providing all necessary signatures or neglecting to fill in every required field, it impedes the processing of the form. This level of accuracy is crucial for the IRS's understanding and acceptance of the election.

Another frequent error is missing the filing deadline. The IRS mandates that Form 2553 be filed no later than two months and 15 days after the beginning of the tax year the election is to take effect. For a new company, this usually means the deadline aligns closely with the start of the business. Underestimating this timeline often results in a missed opportunity to benefit from S-corporation taxation for the desired tax year.

Incorrectly identifying the tax year is yet another mistake. Electing S-corporation status requires specifying the tax year for which the election applies. Some businesses mistakenly assume this aligns with the calendar year and fail to consider their fiscal year if it differs. This misalignment can nullify the election for the intended year, complicaying tax filings and potentially leading to higher taxes or penalties.

Lastly, a misunderstanding of eligibility criteria often leads to rejected applications. Not all businesses qualify for S-corporation status under IRS rules. Key requirements include having only allowable shareholders, such as individuals, certain trusts, and estates; having no more than 100 shareholders; issuing only one class of stock; and being a domestic corporation. Unawareness or oversight of these criteria frequently results in unsuccessful elections.

When it comes to navigating the complexities of tax law and corporate structure, understanding the paperwork involved can be more than just a logistical necessity—it's a strategy for success. Among these, the IRS Form 2553, Election by a Small Business Corporation, stands out. It's pivotal for businesses that choose to be taxed as an S corporation, a decision that can lead to significant tax advantages. However, Form 2553 doesn't journey alone through the bureaucratic landscape. There are several other important documents and forms that often accompany it, each playing a pivotal role in ensuring businesses comply with regulations and make the most of their elected status.

In the grand tapestry of corporate taxation, each form plays a critical role. They are the threads that weave together the legal and financial identity of a business, ensuring compliance, facilitating benefits, and paving the way for successful operational strategies. While navigating them may seem daunting, they collectively serve as the scaffold that supports the business's tax structure, illustrating the importance of understanding and accurately managing these documents.

The IRS Form 8832 is akin to the 2553 form, primarily because it offers a business the option to change its tax classification. Much like how the 2553 allows S corporations to elect their tax status, Form 8832 enables entities to choose their taxation as a C corporation or a partnership, providing flexibility in tax planning. Both forms play crucial roles in how a business decides to be recognized for tax purposes, greatly influencing their financial strategies and tax liabilities.

Form 1120S shares similarities with the 2553 form as it is directly tied to the election made through Form 2553. After electing S corporation status with Form 2553, a corporation must annually file Form 1120S to report income, losses, dividends, and other financial activities. This document is a continuation of the election process, facilitating the specialized tax treatment S corporations receive, making it an indispensable part of the S corp lifecycle.

Form 1065, while primarily used by partnerships to report their income, deductions, gains, and losses, has a connection to Form 2553 in its focus on pass-through taxation. When businesses file Form 2553 and elect S corporation status, they're choosing a tax treatment that, like partnerships, allows income to be passed through to the shareholders or owners to be taxed at individual rates, preventing double taxation. This similarity underscores the preference for tax structures that provide flexibility and potentially lower tax burdens for business owners.

The Employer Identification Number (EIN) Application (Form SS-4) is a precursor to the 2553 form. Before a corporation can elect to be treated as an S corporation using Form 2553, it must first obtain an EIN using Form SS-4. This identification number is essential for the IRS to track the business’s tax filings and is a fundamental requirement for nearly all businesses, making Form SS-4 a critical step before any tax election can be made.

Form 1040 Schedule C is related to Form 2553 in its use by sole proprietors to report their business income and expenses. Although it serves a different taxpayer – the sole proprietor – it shares the concept of pass-through taxation with S corporation status. Once a business elects to be treated as an S corp, the owners report their share of the corporation's income and losses on their personal tax returns, similar to how a sole proprietor's business income is treated.

Form W-9, Request for Taxpayer Identification Number and Certification, though fundamentally a form for identifying tax information for contractors, shares a connection with Form 2553 through its role in ensuring compliance with the IRS’s reporting requirements. It helps S corporations, like other entities, collect necessary information for reporting payments to the IRS, playing a crucial part in the tax reporting process by ensuring accurate reporting of payments and avoiding withholding errors.

The Articles of Incorporation, a document filed with a state to legally form a corporation, are indirectly related to the Form 2553. They lay the legal foundation for a company, establishing its existence. Without this incorporation, a business cannot elect S corporation status because the status is specifically for corporations (and certain other entities that meet the IRS criteria). Thus, while not an IRS form, the Articles of Incorporation are a crucial step on the path to electing S corp status.

Form 2551, another document within the IRS repertoire, is used by businesses to calculate and report excise taxes. While seemingly unrelated, the connection to Form 2553 lies in regulation and accountability. Just as excise taxes must be accurately reported for compliance, electing S corporation status with Form 2553 necessitates adherence to specific tax obligations and reporting standards, highlighting the broader theme of fiscal responsibility within business operations.

State-specific S corporation election forms, which vary by jurisdiction, serve a purpose parallel to the IRS Form 2553 but on a state level. Some states require a separate election to treat your corporation as an S corp under state tax laws, even after filing Form 2553 with the IRS. This underscores the layered complexity of tax planning and compliance, where federal elections may not suffice for state tax purposes, necessitating additional documentation.

Lastly, the Operating Agreement, typically used by LLCs, parallels Form 2553 in its role of defining the operations of a business and its ownership structure. Though it's an internal document and not filed with the IRS, it's instrumental in delineating how a business elects to be taxed if it chooses to be treated as an S corporation. This agreement can specify the allocation of income among members, echoing the pass-through characteristic of S corporation taxation and thus shares a conceptual similarity with the election process of Form 2553.

Filling out IRS Form 2553 is a crucial step for businesses electing to be treated as an S corporation for tax purposes. This election can afford significant tax benefits, including pass-through taxation, where the corporation's income, deductions, credits, etc., pass through directly to the shareholders' personal tax returns. To ensure a smooth and successful filing, it's important to pay close attention to the details and requirements of the form. Here are a few dos and don'ts to consider:

Do:

Ensure eligibility. Before filling out the form, make sure your business meets all the criteria for S corporation status, including the number of shareholders, type of shareholders, and stock categories.

Use the correct form version. Always use the most current version of Form 2553 available from the IRS website to avoid processing delays or rejections.

Provide accurate information. Double-check all entries for accuracy, especially critical information like the Employer Identification Number (EIN) and the names and Social Security numbers of all shareholders.

Be timely. Submit Form 2553 by the prescribed deadline — generally no later than two months and 15 days after the beginning of the tax year the election is to take effect.

Keep a copy. Always retain a copy of the signed form and any correspondence with the IRS regarding Form 2553 for your records.

Don't:

Overlook state requirements. In addition to the federal election, be aware of and comply with any state-specific requirements for S corporations, as they can vary.

Miss signatures. Ensure that all required parties, including all shareholders, sign the form. Missing signatures can result in the rejection of the form.

Ignore deadlines. Failing to submit Form 2553 on time could result in losing the S corporation election for the tax year, potentially leading to unfavorable tax implications.

Submit incomplete information. An incomplete form can delay processing times or lead to denial of your S corporation status.

Rely solely on paper filing. Consider using the IRS's electronic filing options where available, as it can expedite the processing of your form.

Adhering to these guidelines when completing and submitting IRS Form 2553 can help ensure that your election to S corporation status is processed efficiently and without unnecessary complications. Keep in mind that while this form is a critical step in electing S corporation status, maintaining compliance with ongoing requirements is equally important. Always consider consulting with a tax professional or legal advisor familiar with your specific business situation for personalized advice and guidance.

The IRS 2553 form, often associated with the election by a Small Business Corporation (S-Corporation) status, is surrounded by a myriad of misconceptions. Understanding these inaccuracies is crucial for businesses contemplating this tax status. Below are six common misunderstandings about Form 2553:

Dispelling these misconceptions about the IRS 2553 form is critical for businesses considering the S-Corporation election. It ensures decisions are made based on accurate understandings, potentially leading to significant tax advantages and compliance with federal tax obligations.

When it comes to navigating the nuances of tax forms, the IRS 2553 form stands out for those looking to elect S corporation status for their business. This election can offer various benefits, including pass-through taxation, where income is reported on the shareholders' individual tax returns, potentially leading to tax savings. Understanding how to properly complete and use form 2553 is crucial for business owners. Here are key takeaways to ensure the process is handled smoothly:

Successfully completing and submitting IRS form 2553 is a vital step for companies choosing to take advantage of the benefits of S corporation status. Attention to detail, understanding eligibility requirements, and timely filing are crucial components of this process. Remember, when in doubt, seeking advice from a tax professional can help navigate the complexities of tax laws and regulations.

Biopsychosocial Template - Investigates any family or relationship issues to offer tailored therapeutic interventions.

W9 Form Sample - For non-employees, the W-9 form is the starting point in the tax documentation process, ensuring they are taxed appropriately on income earned.