Fill a Valid IRS 5304-SIMPLE Form

Fill a Valid IRS 5304-SIMPLE Form

When it comes to saving for retirement, small businesses have a range of options, one of which is creating a Savings Incentive Match Plan for Employees, or SIMPLE IRA. This is where the IRS 5304-SIMPLE form plays a crucial role. Specifically designed for employers who choose not to designate a financial institution for their employees, this form allows each employee to select where they would like their retirement contributions to be deposited. This flexibility is a significant advantage, offering employees control over their investments and potential for growth in their retirement savings. Moreover, the form is part of the broader framework ensuring that businesses comply with federal guidelines for retirement plans, making it an essential document for employers aiming to provide a robust and compliant retirement benefits package. By helping businesses set up these plans efficiently and in compliance with tax laws, the IRS 5304-SIMPLE form facilitates a smoother process for both employers and employees, making the journey toward retirement security a bit easier to navigate.

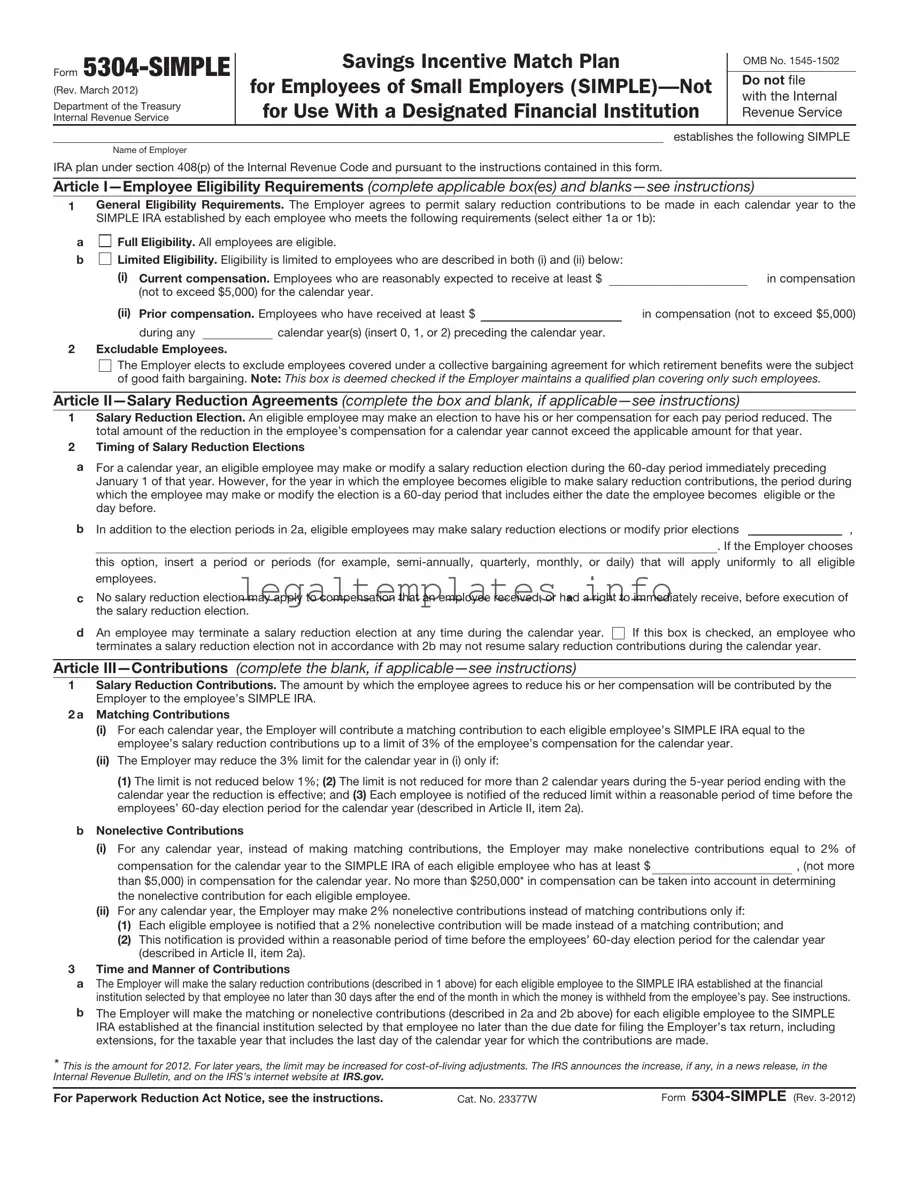

Form

(Rev. March 2012)

Department of the Treasury

Internal Revenue Service

Savings Incentive Match Plan

for Employees of Small Employers

OMB No.

Do not file

with the Internal Revenue Service

establishes the following SIMPLE

Name of Employer

IRA plan under section 408(p) of the Internal Revenue Code and pursuant to the instructions contained in this form.

Article

1General Eligibility Requirements. The Employer agrees to permit salary reduction contributions to be made in each calendar year to the SIMPLE IRA established by each employee who meets the following requirements (select either 1a or 1b):

a |

Full Eligibility. All employees are eligible. |

|

|

||||||

b |

Limited Eligibility. Eligibility is limited to employees who are described in both (i) and (ii) below: |

|

|

||||||

|

(i) |

Current compensation. Employees who are reasonably expected to receive at least $ |

|

in compensation |

|||||

|

(ii) |

(not to exceed $5,000) for the calendar year. |

|

|

|

||||

|

Prior compensation. Employees who have received at least $ |

|

|

in compensation (not to exceed $5,000) |

|||||

|

|

during any |

|

calendar year(s) (insert 0, 1, or 2) preceding the calendar year. |

|

|

|||

2Excludable Employees.

The Employer elects to exclude employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining. Note: This box is deemed checked if the Employer maintains a qualified plan covering only such employees.

Article

1Salary Reduction Election. An eligible employee may make an election to have his or her compensation for each pay period reduced. The total amount of the reduction in the employee’s compensation for a calendar year cannot exceed the applicable amount for that year.

2Timing of Salary Reduction Elections

aFor a calendar year, an eligible employee may make or modify a salary reduction election during the

b In addition to the election periods in 2a, eligible employees may make salary reduction elections or modify prior elections,

. If the Employer chooses this option, insert a period or periods (for example,

cNo salary reduction election may apply to compensation that an employee received, or had a right to immediately receive, before execution of the salary reduction election.

dAn employee may terminate a salary reduction election at any time during the calendar year.

If this box is checked, an employee who terminates a salary reduction election not in accordance with 2b may not resume salary reduction contributions during the calendar year.

If this box is checked, an employee who terminates a salary reduction election not in accordance with 2b may not resume salary reduction contributions during the calendar year.

Article

1Salary Reduction Contributions. The amount by which the employee agrees to reduce his or her compensation will be contributed by the Employer to the employee’s SIMPLE IRA.

2 a Matching Contributions

(i)For each calendar year, the Employer will contribute a matching contribution to each eligible employee’s SIMPLE IRA equal to the employee’s salary reduction contributions up to a limit of 3% of the employee’s compensation for the calendar year.

(ii)The Employer may reduce the 3% limit for the calendar year in (i) only if:

(1) The limit is not reduced below 1%; (2) The limit is not reduced for more than 2 calendar years during the

bNonelective Contributions

(i)For any calendar year, instead of making matching contributions, the Employer may make nonelective contributions equal to 2% of

compensation for the calendar year to the SIMPLE IRA of each eligible employee who has at least $, (not more

than $5,000) in compensation for the calendar year. No more than $250,000* in compensation can be taken into account in determining the nonelective contribution for each eligible employee.

(ii)For any calendar year, the Employer may make 2% nonelective contributions instead of matching contributions only if:

(1)Each eligible employee is notified that a 2% nonelective contribution will be made instead of a matching contribution; and

(2)This notification is provided within a reasonable period of time before the employees’

3Time and Manner of Contributions

aThe Employer will make the salary reduction contributions (described in 1 above) for each eligible employee to the SIMPLE IRA established at the financial institution selected by that employee no later than 30 days after the end of the month in which the money is withheld from the employee’s pay. See instructions.

bThe Employer will make the matching or nonelective contributions (described in 2a and 2b above) for each eligible employee to the SIMPLE IRA established at the financial institution selected by that employee no later than the due date for filing the Employer’s tax return, including extensions, for the taxable year that includes the last day of the calendar year for which the contributions are made.

* This is the amount for 2012. For later years, the limit may be increased for

For Paperwork Reduction Act Notice, see the instructions. |

Cat. No. 23377W |

Form |

Form |

Page 2 |

Article |

|

1Contributions in General. The Employer will make no contributions to the SIMPLE IRAs other than salary reduction contributions (described in Article III, item 1) and matching or nonelective contributions (described in Article III, items 2a and 2b).

2Vesting Requirements. All contributions made under this SIMPLE IRA plan are fully vested and nonforfeitable.

3No Withdrawal Restrictions. The Employer may not require the employee to retain any portion of the contributions in his or her SIMPLE IRA or otherwise impose any withdrawal restrictions.

4Selection of IRA Trustee. The Employer must permit each eligible employee to select the financial institution that will serve as the trustee, custodian, or issuer of the SIMPLE IRA to which the Employer will make all contributions on behalf of that employee.

5Amendments To This SIMPLE IRA Plan. This SIMPLE IRA plan may not be amended except to modify the entries inserted in the blanks or boxes provided in Articles I, II, III, VI, and VII.

6Effects Of Withdrawals and Rollovers

aAn amount withdrawn from the SIMPLE IRA is generally includible in gross income. However, a SIMPLE IRA balance may be rolled over or transferred on a

bIf an individual withdraws an amount from a SIMPLE IRA during the

Article

1Compensation

aGeneral Definition of Compensation. Compensation means the sum of the wages, tips, and other compensation from the Employer subject to federal income tax withholding (as described in section 6051(a)(3)), the amounts paid for domestic service in a private home, local college club, or local chapter of a college fraternity or sorority, and the employee’s salary reduction contributions made under this plan, and, if applicable, elective deferrals under a section 401(k) plan, a SARSEP, or a section 403(b) annuity contract and compensation deferred under a section 457 plan required to be reported by the Employer on Form

bCompensation for

2Employee. Employee means a

3Eligible Employee. An eligible employee means an employee who satisfies the conditions in Article I, item 1 and is not excluded under Article I, item 2.

4SIMPLE IRA. A SIMPLE IRA is an individual retirement account described in section 408(a), or an individual retirement annuity described in section 408(b), to which the only contributions that can be made are contributions under a SIMPLE IRA plan and rollovers or transfers from another SIMPLE IRA.

Article

are unavailable, or (2) that financial institution provides the procedures directly to the employee. See Employee Notification in the instructions.)

Article

This SIMPLE IRA plan is effective |

|

|

|

|

. See |

|

instructions. |

|

|

|

|

|

|

* |

* |

* |

* |

* |

|

|

|

|

|

|

|

|

|

Name of Employer |

|

By: |

Signature |

Date |

||

|

|

|

|

|

|

|

Address of Employer |

|

Name and title |

|

|

||

Form

Form |

Page 3 |

Model Notification to Eligible Employees

I.Opportunity to Participate in the SIMPLE IRA Plan

You are eligible to make salary reduction contributions to theSIMPLE IRA

plan. This notice and the attached summary description provide you with information that you should consider before you decide whether to start, continue, or change your salary reduction agreement.

II.Employer Contribution Election

For the |

|

calendar year, the Employer elects to contribute to your SIMPLE IRA (employer must select either (1), (2), or (3)): |

|||||

(1) |

A matching contribution equal to your salary reduction contributions up to a limit of 3% of your compensation for the year; |

||||||

(2) |

A matching contribution equal to your salary reduction contributions up to a limit of |

% (employer must insert a |

|||||

number from 1 to 3 and is subject to certain restrictions) of your compensation for the |

year; or |

|

|||||

(3) |

A nonelective contribution equal to 2% of your compensation for the year (limited to compensation of $250,000*) if you are an |

||||||

employee who makes at least $ |

|

(employer must insert an amount that is $5,000 or less) in compensation for |

|||||

the year. |

|

|

|

|

|

||

|

|

|

|

|

|||

III.Administrative Procedures

To start or change your salary reduction contributions, you must complete the salary reduction agreement and return it to

|

|

|

(employer should designate a place or |

individual by |

|

(employer should insert a date that is not less than 60 |

days after notice is given). |

|

|

|

|

IV. Employee Selection of Financial Institution

You must select the financial institution that will serve as the trustee, custodian, or issuer of your SIMPLE IRA and notify your Employer of your selection.

Model Salary Reduction Agreement

I.Salary Reduction Election

Subject to the requirements of the SIMPLE IRA plan of |

|

|

|

|

(name of |

|||

employer) I authorize |

|

% or $ |

|

|

(which equals |

|

% of my current rate of pay) to be withheld from |

|

my pay for each pay period and contributed to my SIMPLE IRA as a salary reduction contribution.

II.Maximum Salary Reduction

I understand that the total amount of my salary reduction contributions in any calendar year cannot exceed the applicable amount for that year. See instructions.

III.Date Salary Reduction Begins

I understand that my salary reduction contributions will start as soon as permitted under the SIMPLE IRA plan and as soon as

administratively feasible or, if later,. (Fill in the date you want the salary reduction contributions to begin. The date must be after you sign this agreement.)

IV. Employee Selection of Financial Institution

I select the following financial institution to serve as the trustee, custodian, or issuer of my SIMPLE IRA.

Name of financial institution

Address of financial institution

SIMPLE IRA account name and number

I understand that I must establish a SIMPLE IRA to receive any contributions made on my behalf under this SIMPLE IRA plan. If the information regarding my SIMPLE IRA is incomplete when I first submit my salary reduction agreement, I realize that it must be completed by the date contributions must be made under the SIMPLE IRA plan. If I fail to update my agreement to provide this information by that date, I understand that my Employer may select a financial institution for my SIMPLE IRA.

V.Duration of Election

This salary reduction agreement replaces any earlier agreement and will remain in effect as long as I remain an eligible employee under the SIMPLE IRA plan or until I provide my Employer with a request to end my salary reduction contributions or provide a new salary reduction agreement as permitted under this SIMPLE IRA plan.

Signature of employee |

|

Date |

*This is the amount for 2012. For later years, the limit may be increased for

Form

Form |

Page 4 |

General Instructions

Section references are to the Internal Revenue Code unless otherwise noted.

Purpose of Form

Form

SIMPLE IRA.

These instructions are designed to assist in the establishment and administration of the SIMPLE IRA plan. They are not intended to supersede any provision in the SIMPLE IRA plan.

Do not file Form

For more information, see Pub. 560, Retirement Plans for Small Business (SEP, SIMPLE, and Qualified Plans), and Pub. 590, Individual Retirement Arrangements (IRAs).

Note. If you used the March 2002, August 2005, or September 2008 version of Form

Which Employers May

Establish and Maintain a

SIMPLE IRA Plan?

To establish and maintain a SIMPLE IRA plan, you must meet both of the following requirements:

1.Last calendar year, you had no more than 100 employees (including

2.You do not maintain during any part of the calendar year another qualified plan with respect to which contributions are made, or benefits are accrued, for service in the calendar year. For this purpose, a qualified plan (defined in section 219(g)(5)) includes a qualified pension plan, a

participating in the SIMPLE IRA plan. If the failure to continue to satisfy the

Certain related employers (trades or businesses under common control) must be treated as a single employer for purposes of the SIMPLE IRA requirements. These are: (1) a controlled group of corporations under section 414(b); (2) a partnership or sole proprietorship under common control under section 414(c); or (3) an affiliated service group under section 414(m). In addition, if you have leased employees required to be treated as your own employees under the rules of section 414(n), then you must count all such leased employees for the requirements listed above.

What Is a SIMPLE IRA Plan?

A SIMPLE IRA plan is a written arrangement that provides you and your employees with an easy way to make contributions to provide retirement income for your employees. Under a SIMPLE IRA plan, employees may choose whether to make salary reduction contributions to the SIMPLE IRA plan rather than receiving these amounts as part of their regular compensation. In addition, you will contribute matching or nonelective contributions on behalf of eligible employees (see Employee Eligibility Requirements below and Contributions later). All contributions under this plan will be deposited into a SIMPLE individual retirement account or annuity established for each eligible employee with the financial institution selected by him or her.

When To Use Form

A SIMPLE IRA plan may be established by using this Model Form or any other document that satisfies the statutory requirements.

Do not use Form

1.You want to require that all SIMPLE IRA plan contributions initially go to a financial institution designated by you. That is, you do not want to permit each of your eligible employees to choose a financial institution that will initially receive contributions. Instead, use Form

2.You want employees who are nonresident aliens receiving no earned income from you that is income from sources within the United States to be eligible under this plan; or

3.You want to establish a SIMPLE 401(k) plan.

Completing Form

Pages 1 and 2 of Form

The SIMPLE IRA plan is a legal document with important tax consequences for you and your employees. You may want to consult with your attorney or tax advisor before adopting this plan.

Employee Eligibility Requirements (Article I)

Each year for which this SIMPLE IRA plan is effective, you must permit salary reduction contributions to be made by all of your employees who are reasonably expected to receive at least $5,000 in compensation from you during the year, and who received at least $5,000 in compensation from you in any 2 preceding years. However, you can expand the group of employees who are eligible to participate in the SIMPLE IRA plan by completing the options provided in Article I, items 1a and 1b. To choose full eligibility, check the box in Article I, item 1a. Alternatively, to choose limited eligibility, check the box in Article I, item 1b, and then insert “$5,000” or a lower compensation amount (including zero) and “2” or a lower number of years of service in the blanks in (i) and (ii) of Article I, item 1b.

In addition, you can exclude from participation those employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining. You may do this by checking the box in Article I, item 2. Under certain circumstances, these employees must be excluded. See Which Employers May Establish and Maintain a SIMPLE IRA Plan? above.

Salary Reduction Agreements (Article II)

As indicated in Article II, item 1, a salary reduction agreement permits an eligible employee to make a salary reduction election to have his or her compensation for each pay period reduced by a percentage (expressed as a percentage or dollar amount). The total amount of

Form |

Page 5 |

the reduction in the employee’s compensation cannot exceed the applicable amount for any calendar year. The applicable amount is $11,500 for 2012. After 2012, the $11,500 amount may be increased for

Timing of Salary Reduction Elections

For any calendar year, an eligible employee may make or modify a salary reduction election during the

You can extend the

You may use the Model Salary Reduction Agreement on page 3 to enable eligible employees to make or modify salary reduction elections.

Employees must be permitted to terminate their salary reduction elections at any time. They may resume salary reduction contributions for the year if permitted under Article II, item 2b. However, by checking the box in Article II, item 2d, you may prohibit an employee who terminates a salary reduction election outside the normal election cycle from resuming salary reduction contributions during the remainder of the calendar year.

Contributions (Article III)

Only contributions described below may be made to this SIMPLE IRA plan. No additional contributions may be made.

Salary Reduction Contributions

As indicated in Article III, item 1, salary reduction contributions consist of the amount by which the employee agrees to reduce his or her compensation. You must contribute the salary reduction contributions to the financial institution selected by each eligible employee.

Matching Contributions

In general, you must contribute a matching contribution to each eligible employee’s SIMPLE IRA equal to the employee’s salary reduction contributions. This matching contribution cannot exceed 3% of the employee’s compensation. See Definition of Compensation, below.

You may reduce this 3% limit to a lower percentage, but not lower than 1%. You cannot lower the 3% limit for more than 2 calendar years out of the

Note. If any year in the

To elect this option, you must notify the employees of the reduced limit within a reasonable period of time before the applicable

Nonelective Contributions

Instead of making a matching contribution, you may, for any year, make a nonelective contribution equal to 2% of compensation for each eligible employee who has at least $5,000 in compensation for the year.

Nonelective contributions may not be based on more than $250,000* of compensation.

To elect to make nonelective contributions, you must notify employees within a reasonable period of time before the applicable

Note. Insert “$5,000” in Article III, item 2b(i) to impose the $5,000 compensation requirement. You may expand the group of employees who are eligible for nonelective contributions by inserting a compensation amount lower than $5,000.

Effective Date (Article VII)

Insert in Article VII the date you want the provisions of the SIMPLE IRA plan to become effective. You must insert January 1 of the applicable year unless this is the first year for which you are adopting any SIMPLE IRA plan. If this is the first year for which you are adopting a SIMPLE IRA plan, you may insert any date between January 1 and October 1, inclusive of the applicable year.

Additional Information

Timing of Salary Reduction Contributions

The employer must make the salary reduction contributions to the financial institution selected by each eligible employee for his or her SIMPLE IRA no later than the 30th day of the month following the month in which the amounts would otherwise have been payable to the employee in cash.

The Department of Labor has indicated that most SIMPLE IRA plans are also subject to Title I of the Employee Retirement Income Security Act of 1974 (ERISA). Under Department of Labor regulations at 29 CFR

Definition of Compensation

“Compensation” means the amount described in section 6051(a)(3) (wages, tips, and other compensation from the employer subject to federal income tax withholding under section 3401(a)), and amounts paid for domestic service in a private home, local college club, or local chapter of a college fraternity or sorority. Usually, this is the amount shown in box 1 of Form

For

Employee Notification

You must notify each eligible employee prior to the employee’s

*This is the amount for 2012. For later years, the limit may be increased for

Form |

Page 6 |

issuer of the employee’s SIMPLE IRA. In this notification, you must indicate whether you will provide:

1.A matching contribution equal to your employees’ salary reduction contributions up to a limit of 3% of their compensation;

2.A matching contribution equal to your employees’ salary reduction contributions subject to a percentage limit that is between 1 and 3% of their compensation; or

3.A nonelective contribution equal to 2% of your employees’ compensation.

You can use the Model Notification to Eligible Employees earlier to satisfy these employee notification requirements for this SIMPLE IRA plan. A Summary Description must also be provided to eligible employees at this time. This summary description requirement may be satisfied by providing a completed copy of pages 1 and 2 of Form

Article

If you fail to provide the employee notification (including the summary description) described above, you will be liable for a penalty of $50 per day until the notification is provided. If you can show that the failure was due to reasonable cause, the penalty will not be imposed.

If the financial institution’s name, address, or withdrawal procedures are not available at the time the employee must be given the summary description, you must provide the summary description without this information. In that case, you will have reasonable cause for not including this information in the summary description, but only if you ensure that it is provided to the employee as soon as administratively feasible.

Reporting Requirements

You are not required to file any annual information returns for your SIMPLE IRA plan, such as Form 5500, Annual Return/Report of Employee Benefit Plan, or Form

Deducting Contributions

Contributions to this SIMPLE IRA plan are deductible in your tax year containing the end of the calendar year for which the contributions are made.

Contributions will be treated as made for a particular tax year if they are made for that year and are made by the due date (including extensions) of your income tax return for that year.

Summary Description

Each year the SIMPLE IRA plan is in effect, the financial institution for the SIMPLE IRA of each eligible employee must provide the employer the information described in section 408(l)(2)(B). This requirement may be satisfied by providing the employer a current copy of Form

There is a penalty of $50 per day imposed on the financial institution for each failure to provide the summary description described above. However, if the failure was due to reasonable cause, the penalty will not be imposed.

Paperwork Reduction Act Notice. You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete this form will vary depending on individual circumstances. The estimated average time is:

Recordkeeping . . |

. |

. |

3 hr., 38 min. |

Learning about the |

|

|

|

law or the form . . |

. |

. |

2 hr., 26 min. |

Preparing the form |

. |

. |

. . 47 min. |

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. You can write to the Internal Revenue Service, Tax Products Coordinating Committee, SE:W:CAR:MP:T:M:S, 1111 Constitution Ave. NW,

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS 5304-SIMPLE form is used by small businesses to set up a Savings Incentive Match Plan for Employees (SIMPLE) that allows employees to choose their own financial institution for receiving contributions. |

| Eligibility | Businesses with 100 or fewer employees who received $5,000 or more in compensation during the preceding calendar year are eligible to use this form. |

| Contribution Limits | Contribution limits for the SIMPLE plans are adjusted annually for inflation. For the current limit, users should refer to the IRS website or recent publications. |

| Employer Match | Employers using Form 5304-SIMPLE must either match employee contributions dollar for dollar up to 3% of an employee's compensation or contribute 2% of each eligible employee's compensation. |

| Deadlines | The plan must be established and employees notified within a specific timeframe before the tax year begins, usually by November 2nd for an existing business. |

| Employee Control | Unlike other retirement plans, the 5304-SIMPLE allows employees to select the financial institution where their contributions will be deposited. |

| Governing Law | While the IRS sets the federal guidelines for SIMPLE IRA plans, state laws regarding retirement plans can vary and may impose additional requirements on employers. |

Filling out the IRS 5304-SIMPLE form is a critical step for small businesses that elect to offer a savings incentive match plan for employees (SIMPLE). This specific form allows each employee to choose their own financial institution for receiving SIMPLE IRA contributions, giving both employees and employers flexibility and control over their retirement savings. Approaching this task with accuracy and attention to detail ensures compliance with IRS regulations and sets the stage for a successful and beneficial SIMPLE IRA plan for all involved. Here’s a step-by-step guide to get you through the form without much hassle.

After completing the IRS 5304-SIMPLE form, review it thoroughly to ensure no errors or omissions. Filing accurate and complete forms with the IRS is crucial to maintaining the integrity of your SIMPLE IRA plan and avoiding potential compliance issues. Once satisfied, submit the form according to the IRS submission guidelines pertinent to your situation. Remember, this is about setting up a foundation for your employees' future financial security, a task that, while it may seem daunting, marks a significant contribution towards their well-being.

What is an IRS 5304-SIMPLE form?

The IRS 5304-SIMPLE form is a document used by small business employers to set up a Savings Incentive Match Plan for Employees (SIMPLE) IRA. This plan allows employees and employers to contribute to traditional IRAs set up for employees. It is designed for businesses with 100 or fewer employees who earned $5,000 or more during the preceding calendar year. The 5304-SIMPLE form allows each participant to choose the financial institution for receiving their contributions, giving them flexibility in selecting where their IRA will be held.

Who can use the IRS 5304-SIMPLE form?

Small business employers with 100 or fewer employees who received at least $5,000 in compensation during the previous year are eligible to use the IRS 5304-SIMPLE form. This includes self-employed individuals. It's an attractive option for small businesses that wish to offer a retirement savings plan but are looking for a simpler, less costly alternative to traditional 401(k) plans. It's important to note that employers who choose to adopt a SIMPLE IRA plan cannot maintain any other employer-sponsored retirement plan.

How do contributions work with the 5304-SIMPLE IRA plan?

Contributions to a 5304-SIMPLE IRA plan can come from both employees and employers. Employees can choose to make salary reduction contributions up to the legal annual limit, which is subject to cost-of-living adjustments each year. Employers are required to make either a matching contribution of up to 3% of an employee’s compensation or a non-elective contribution of 2% of an employee’s compensation up to the annual compensation limit. This ensures that all participating employees receive some form of employer contribution, whether or not they choose to contribute themselves.

What are the deadlines for setting up a 5304-SIMPLE IRA plan?

A 5304-SIMPLE IRA plan must be set up by October 1st of the year it will come into effect. For businesses starting mid-year or newly eligible businesses, the plan should be set up as soon as administratively feasible after meeting the eligibility requirements. Annual employee notices of the plan must be distributed within a reasonable time before the 60-day election period, which generally runs from November 2nd to December 31st for an existing plan. It's crucial for businesses to adhere to these deadlines to ensure the plan's smooth implementation and operation.

One common mistake that individuals make when filling out the IRS 5304-SIMPLE form is neglecting to accurately designate a financial institution. This form, intended to establish a Savings Incentive Match Plan for Employees (SIMPLE) IRA, requires the designation of an institution where contributions will be deposited. However, oftentimes, the name or address of the institution is incorrectly noted, or the section is left blank entirely. This oversight can cause significant delays in the processing of the form, as well as the setup of the retirement plan.

Another error frequently encountered involves misunderstandings regarding the eligibility requirements for participation. The IRS 5304-SIMPLE form mandates that employers clearly outline the eligibility criteria for their employees. Unfortunately, it's not uncommon for this section to be incorrectly filled out, leading to potential disputes or confusion about who is qualified to participate in the plan. Ensuring that the eligibility criteria are correctly defined and communicated is crucial for the smooth operation of the SIMPLE IRA plan.

Contributions and compensation definitions often become a source of errors. Employers are required to determine and document how they calculate compensation for the purposes of contributions to the SIMPLE IRA. Mistakes in this area can arise from not fully understanding what constitutes compensation for this specific purpose. As such, misinterpretation can lead to either over-contributions or under-contributions, each with its respective ramifications for both employer and employee.

An oversight that can be particularly vexing involves incorrectly completed signature and date sections. The form requires signatures from both the employer and the designated financial institution, confirming their agreement to the arrangement detailed in the document. Sometimes, the form is submitted without all necessary signatures, which invalidates the document. Ensuring that all parties have duly signed and dated the form is a simple yet often overlooked step in the process.

Choosing incorrect plan years can also cause complications. The IRS 5304-SIMPLE form asks employers to specify the plan year, which typically aligns with the calendar year. However, errors occur if an employer inadvertently selects a fiscal year that doesn't match the calendar year without proper justification or alignment with IRS regulations. This mistake can lead to administrative challenges and potential issues with compliance.

Lastly, forgetting to specify the employer's name and address correctly and clearly on the form is a seemingly minor but impactful error. Accurate identification of the employer is essential for the IRS to process the form and establish the plan. Inconsistencies or omissions in this information can result in unnecessary delays or the need to resubmit the form entirely, thereby hindering the timely establishment of the SIMPLE IRA plan.

The IRS 5304-SIMPLE form is an integral document used by small businesses to establish a Savings Incentive Match Plan for Employees. However, setting up and maintaining a SIMPLE IRA plan often necessitates additional forms and documents. These documents not only comply with regulatory requirements but also ensure the smooth operation of the retirement plan. The following list highlights some of these critical forms and documents that employers and employees might use in conjunction with the IRS 5304-SIMPLE form.

In tandem with the IRS 5304-SIMPLE form, these documents form a comprehensive legal and procedural framework for the effective administration of SIMPLE IRA plans. By closely adhering to the guidelines and requirements stipulated in these documents, employers can ensure compliance with federal regulations, thereby securing the financial future of their employees.

The IRS 5304-SIMPLE form is closely related to the IRS 5305-SIMPLE form. Both are designed for small employers to set up savings incentive match plans for employees (SIMPLE) IRAs. The primary difference is that the 5304-SIMPLE allows employees to choose the financial institution for their IRA, whereas the 5305-SIMPLE requires all contributions to be deposited at an employer-selected financial institution. This choice impacts how employees manage their retirement savings.

Another document similar to the IRS 5304-SIMPLE form is the IRS Form 401(k) Plan Document. This document is used by employers to establish a 401(k) plan, which is another type of retirement savings plan. While the structure and specific rules differ, both documents serve the purpose of helping employees save for retirement, with tax-deferred growth on contributions. The key difference lies in the flexibility and contribution limits provided by each plan.

The IRS Form 1099-R is also related, as it deals with distributions from retirement plans, including SIMPLE IRAs. After an employer sets up a SIMPLE IRA plan using the 5304-SIMPLE, distributions from these accounts are reported on Form 1099-R. This form is crucial for both employees and the IRS to track withdrawals from retirement accounts, including any taxes or penalties that might apply.

Similarly, Form 5498 is connected to the 5304-SIMPLE since it is used to report IRA contributions to the IRS, including contributions to SIMPLE IRAs. After employers and employees contribute to SIMPLE IRAs throughout the year, these contributions are reported annually on Form 5498. This ensures the IRS has accurate information on retirement account contributions for tax purposes.

Form 8938, Statement of Foreign Financial Assets, has relevance to the 5304-SIMPLE in scenarios where an employee holds a SIMPLE IRA account through a financial institution outside the United States. This form must be filed if the total value of those foreign financial accounts exceeds certain thresholds, highlighting the global aspect of retirement savings and the IRS's interest in foreign financial accounts.

The IRS Form W-4 is indirectly related to the 5304-SIMPLE form. While Form W-4 is primarily used to determine the amount of federal income tax withholding from an employee's paycheck, employees contributing to a SIMPLE IRA may adjust their withholdings in anticipation of their retirement contributions. This adjustment can help manage tax liabilities, reflecting the interconnectedness of income and retirement planning.

Another document with similarities is IRS Form 8822, Change of Address. Employees participating in a SIMPLE IRA plan established with the 5304-SIMPLE form need to keep their address current with the IRS to receive important tax documents related to their retirement account, such as Form 1099-R and Form 5498. This ensures that employees receive timely and accurate tax documents.

Lastly, the IRS Form 2848, Power of Attorney and Declaration of Representative, is relevant to users of the 5304-SIMPLE form. should an employee need someone else to act on their behalf with the IRS regarding their SIMPLE IRA. This form becomes necessary when dealing with more complex tax situations or when the employee cannot handle their tax affairs directly, showing the need for authorized representation in certain circumstances.

When it comes to preparing the IRS 5304-SIMPLE form, which is vital for setting up a Savings Incentive Match Plan for Employees (SIMPLE) that allows employees to choose their own financial institutions for receiving contributions, accuracy and attention to detail are key. To guide you through this process, here are five dos and don'ts that will help ensure your form is completed correctly.

Do:When navigating the complexities of retirement plans, the IRS 5304-SIMPLE form often comes into play for small businesses. There are, however, several misconceptions about this particular form that need to be clarified:

Clarifying these misconceptions ensures that small businesses can make informed decisions about setting up and managing retirement savings options for their employees through the SIMPLE IRA plan.

The IRS 5304-SIMPLE form is intended for the specific use of establishing a Savings Incentive Match Plan for Employees (SIMPLE) that allows employees to choose the financial institution for receiving their contributions. Here are seven key takeaways to ensure proper completion and use of this form:

Note: Always consult with a financial adviser or tax professional to ensure that the 5304-SIMPLE form and the SIMPLE IRA plan are correctly established and maintained in compliance with current IRS rules and regulations.

How to Design a Crest - A traditional shield adorned with symbols representing the story, values, and culture of those it represents.

Free Printable Annual Physical Exam Form - Assesses the individual’s need for an ICF/ID level of care, ensuring those with intellectual disabilities receive appropriate support.