Fill a Valid IRS 940 Form

Fill a Valid IRS 940 Form

Every year, employers across the United States navigate the complexities of tax filing with a myriad of forms, among which the IRS 940 form plays a crucial role. This form is essentially used to report federal unemployment tax, a mandate that supports the government's ability to provide unemployment benefits to workers who have lost their jobs. Understanding the fundamental aspects of this form is essential for employers, as it aids in compliance with federal regulations, helps avoid potential penalties for late or incorrect filings, and ensures the accurate calculation of owed taxes based on the annual wages paid to employees. The intricacies of the form require a detailed overview, including who should file it, when it is due, and the specific information that must be reported. An employer's journey with the IRS 940 form is marked by the need to provide detailed employment data, adjustments based on state unemployment insurance rates, and calculations that account for payments already made. It serves not just as a tax form but as a reflection of an employer's fiscal responsibility and support for the workforce's safety net.

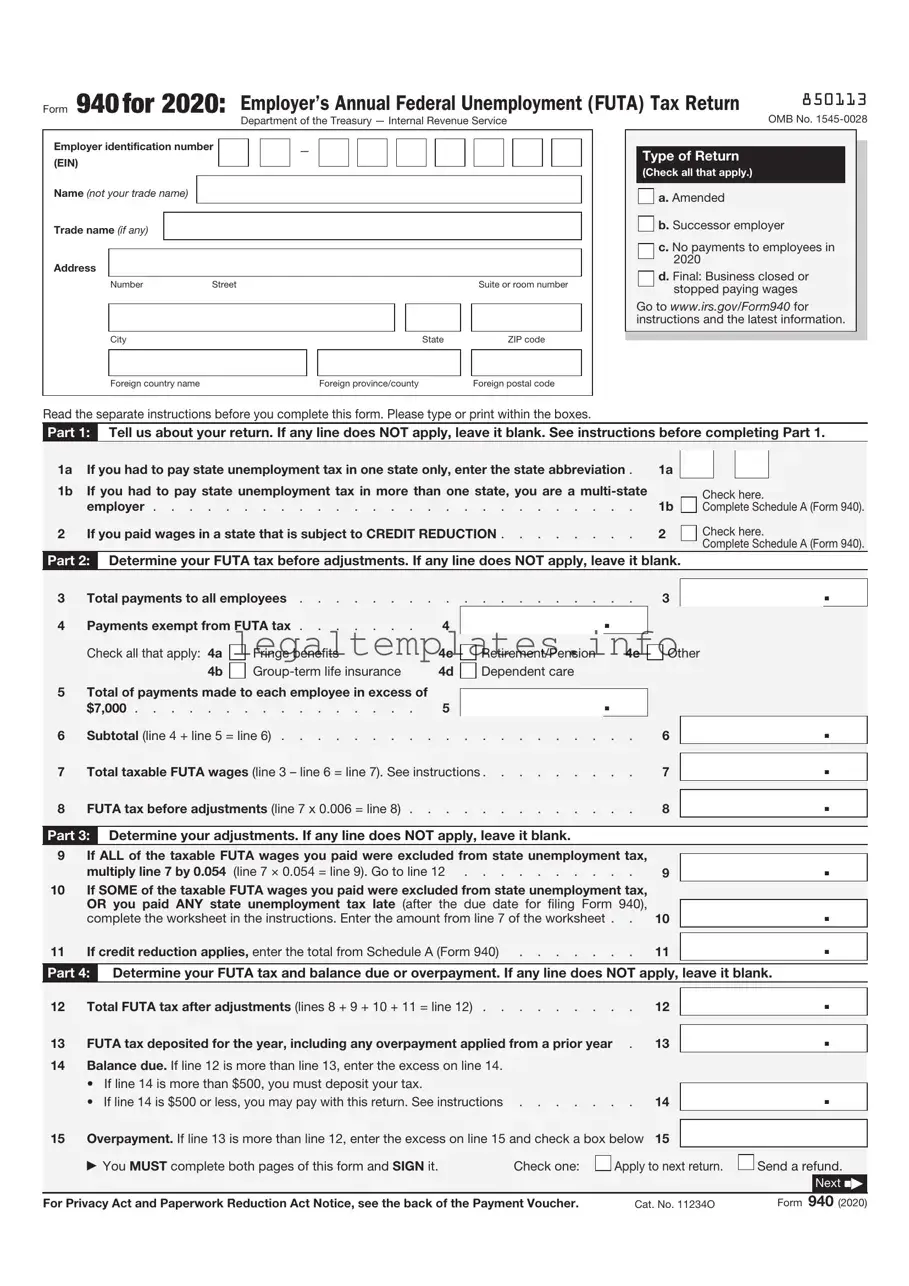

Form 940for 2020: Employer’s Annual Federal Unemployment (FUTA) Tax Return |

850113 |

|

OMB No. |

||

Department of the Treasury — Internal Revenue Service |

Employer identification number |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade name (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Number |

Street |

|

|

|

|

Suite or room number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign country name |

|

|

Foreign province/county |

|

Foreign postal code |

||

Type of Return

(Check all that apply.)

a. Amended

a. Amended

b. Successor employer

b. Successor employer

c. No payments to employees in 2020

d. Final: Business closed or stopped paying wages

Go to www.irs.gov/Form940 for instructions and the latest information.

Read the separate instructions before you complete this form. Please type or print within the boxes.

Part 1: Tell us about your return. If any line does NOT apply, leave it blank. See instructions before completing Part 1.

1a |

If you had to pay state unemployment tax in one state only, enter the state abbreviation . |

1a |

|

1b |

If you had to pay state unemployment tax in more than one state, you are a |

|

|

|

employer |

1b |

|

2 |

If you paid wages in a state that is subject to CREDIT REDUCTION |

2 |

|

|

Check here.

Complete Schedule A (Form 940).

Check here.

Complete Schedule A (Form 940).

Part 2: Determine your FUTA tax before adjustments. If any line does NOT apply, leave it blank.

3 |

Total payments to all employees |

. |

3 |

|

|

|

|

. |

||||||||||

4 |

Payments exempt from FUTA tax |

4 |

|

|

|

. |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Check all that apply: 4a |

|

Fringe benefits |

4c |

|

Retirement/Pension |

4e |

|

Other |

|

|

|

|

|||||

|

|

4b |

|

4d |

|

Dependent care |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

5 |

Total of payments made to each employee in excess of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

. |

|

|

|

|

|

|

|

|

||||||

|

$7,000 |

5 |

|

|

|

|

|

|

|

|

|

|

|

|||||

6 |

Subtotal (line 4 + line 5 = line 6) |

. |

6 |

|

|

|

. |

|||||||||||

|

|

|

|

|

|

|

|

|||||||||||

7 |

Total taxable FUTA wages (line 3 – line 6 = line 7). See instructions |

. |

7 |

|

|

|

|

. |

||||||||||

|

|

|

|

|

|

|

|

|||||||||||

8 |

FUTA tax before adjustments (line 7 x 0.006 = line 8) |

. |

8 |

|

|

|

|

. |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part 3: |

Determine your adjustments. If any line does NOT apply, leave it blank. |

|

|

|

|

|

|

|

|

|||||||||

9 |

If ALL of the taxable FUTA wages you paid were excluded from state unemployment tax, |

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

. |

||||||||||||

|

multiply line 7 by 0.054 |

(line 7 × 0.054 = line 9). Go to line 12 |

. |

9 |

|

|

|

|||||||||||

10 |

If SOME of the taxable FUTA wages you paid were excluded from state unemployment tax, |

|

|

|

|

|

|

|

||||||||||

|

OR you paid ANY state unemployment tax late (after the due date for filing Form 940), |

|

|

|

|

|

|

. |

||||||||||

|

complete the worksheet in the instructions. Enter the amount from line 7 of the worksheet . |

. |

10 |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|||||||||||

11 |

If credit reduction applies, enter the total from Schedule A (Form 940) |

. |

11 |

|

|

|

|

. |

||||||||||

|

|

|

||||||||||||||||

Part 4: |

Determine your FUTA tax and balance due or overpayment. If any line does NOT apply, leave it blank. |

|||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||

12 |

Total FUTA tax after adjustments (lines 8 + 9 + 10 + 11 = line 12) |

. |

12 |

|

|

|

|

. |

||||||||||

|

|

|

|

|

|

|

|

|||||||||||

13 |

FUTA tax deposited for the year, including any overpayment applied from a prior year |

. |

13 |

|

|

|

|

. |

||||||||||

14 |

Balance due. If line 12 is more than line 13, enter the excess on line 14. |

|

|

|

|

|

|

|

|

|||||||||

|

• If line 14 is more than $500, you must deposit your tax. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

14 |

|

|

|

|

. |

|||||

|

• |

If line 14 is $500 or less, you may pay with this return. See instructions |

. |

|

|

|

||||||||||||

|

|

|

|

|

|

|

||||||||||||

15 |

Overpayment. If line 13 is more than line 12, enter the excess on line 15 and check a box below |

15 |

|

|

|

|

. |

|||||||||||

|

|

You MUST complete both pages of this form and SIGN it. |

|

|

Check one: |

|

|

|

Apply to next return. |

|

Send a refund. |

|||||||

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Next N |

|

|

|

|

|

|

||||||||||||||

For Privacy Act and Paperwork Reduction Act Notice, see the back of the Payment Voucher. |

Cat. No. 11234O |

|

Form |

940 (2020) |

||||||||||||||

850212

Name (not your trade name)

Employer identification number (EIN)

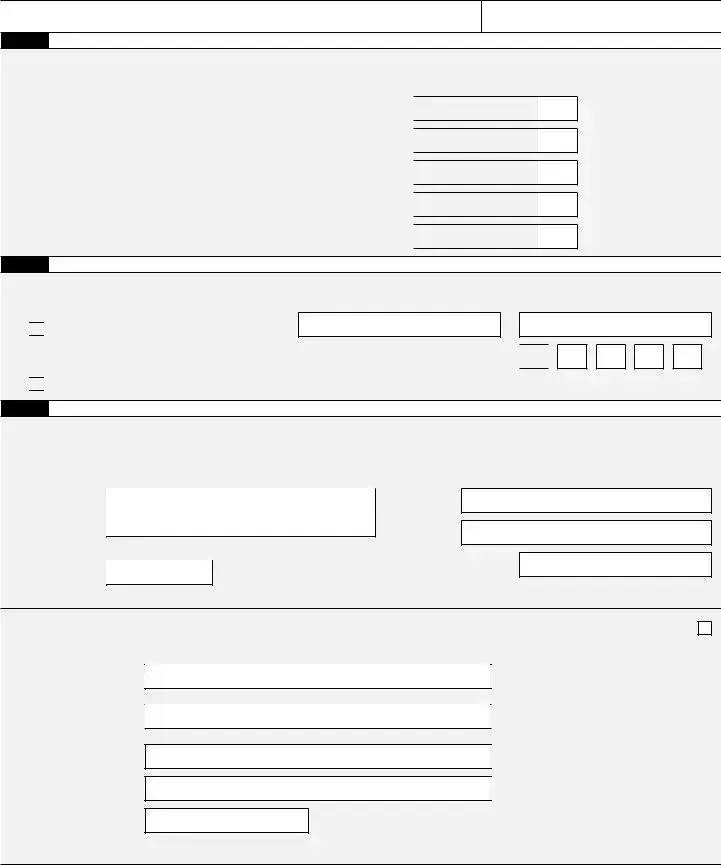

Part 5: Report your FUTA tax liability by quarter only if line 12 is more than $500. If not, go to Part 6.

16Report the amount of your FUTA tax liability for each quarter; do NOT enter the amount you deposited. If you had no liability for a quarter, leave the line blank.

16a |

1st quarter (January 1 – March 31) . . |

. . |

. |

. |

. |

. |

. |

16a |

16b |

2nd quarter (April 1 – June 30) . . . |

. . |

. |

. |

. |

. |

. |

16b |

16c |

3rd quarter (July 1 – September 30) . |

. . |

. |

. |

. |

. |

. |

16c |

16d |

4th quarter (October 1 – December 31) |

. . |

. |

. |

. |

. |

. |

16d |

17 Total tax liability for the year (lines 16a + 16b + 16c + 16d = line 17) 17

.

.

.

.

.

.

.

.

.

.

Total must equal line 12.

Part 6: May we speak with your

Do you want to allow an employee, a paid tax preparer, or another person to discuss this return with the IRS? See the instructions for details.

Yes. Designee’s name and phone number

Yes. Designee’s name and phone number

Select a

No.

No.

Part 7: Sign here. You MUST complete both pages of this form and SIGN it.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete, and that no part of any payment made to a state unemployment fund claimed as a credit was, or is to be, deducted from the payments made to employees. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Sign your name here

Date

/ /

Print your name here

Print your title here

Best daytime phone

Paid Preparer Use Only

Preparer’s name

Preparer’s signature

Firm’s name (or yours if

Address

City

Check if you are

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

Date |

/ |

/ |

|

|

|

EIN |

|

|

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

|

|

|

State |

|

ZIP code |

|

|

|

|

|

|

|

Page 2 |

Form 940 (2020) |

Form

Purpose of Form

Complete Form

Making Payments With Form 940

To avoid a penalty, make your payment with your 2020 Form 940 only if your FUTA tax for the fourth quarter (plus any undeposited amounts from earlier quarters) is $500 or less. If your total FUTA tax after adjustments (Form 940, line 12) is more than $500, you must make deposits by electronic funds transfer. See When Must You Deposit Your FUTA Tax? in the Instructions for Form

940.Also see sections 11 and 14 of Pub. 15 for more information about deposits.

Use Form

may be subject to a penalty. See Deposit Penalties in section 11 of Pub. 15.

Specific Instructions

Box

Box

Box

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your EIN, “Form 940,” and “2020” on your check or money order. Don’t send cash. Don’t staple Form

•Detach Form

Note: You must also complete the entity information above Part 1 on Form 940.

Detach Here and Mail With Your Payment and Form 940. |

|

|||||

|

|

|

|

|||

Form |

|

Payment Voucher |

|

OMB No. |

||

|

|

|||||

|

|

|

|

|

||

|

|

|

|

|

|

|

Department of the Treasury |

|

Don’t staple or attach this voucher to your payment. |

|

2020 |

||

Internal Revenue Service |

|

|

||||

1 Enter your employer identification number (EIN). |

2 |

|

Dollars |

|

Cents |

|

|

|

Enter the amount of your payment. |

|

|

|

|

|

|

Make your check or money order payable to “United States Treasury” |

|

|

|

|

|

|

|

|

|

|

|

3Enter your business name (individual name if sole proprietor).

Enter your address.

Enter your city, state, and ZIP code; or your city, foreign country name, foreign province/county, and foreign postal code.

Form 940 (2020)

Privacy Act and Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. We need it to figure and collect the right amount of tax. Chapter 23, Federal Unemployment Tax Act, of Subtitle C, Employment Taxes, of the Internal Revenue Code imposes a tax on employers with respect to employees. This form is used to determine the amount of the tax that you owe. Section 6011 requires you to provide the requested information if you are liable for FUTA tax under section 3301. Section 6109 requires you to provide your identification number. If you fail to provide this information in a timely manner or provide a false or fraudulent form, you may be subject to penalties.

You’re not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books and records relating to a form or instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law.

Generally, tax returns and return information are confidential, as required by section 6103. However, section 6103 allows or requires the IRS to disclose or give the information shown on your tax return to others as described in the Code. For example, we may disclose

your tax information to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions to administer their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.

The time needed to complete and file this form will vary depending on individual circumstances. The estimated average time is:

Recordkeeping |

9 hr., 19 min. |

Learning about the law or the form . . |

1 hr., 23 min. |

Preparing, copying, assembling, and |

|

sending the form to the IRS |

1 hr., 36 min. |

If you have comments concerning the accuracy of these time estimates or suggestions for making Form 940 simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/FormComments. Or you can send your comments to Internal Revenue Service, Tax Forms and Publications Division, 1111 Constitution Ave. NW,

| Fact Number | Fact Details |

|---|---|

| 1 | The IRS Form 940 is used to report annual Federal Unemployment Tax Act (FUTA) tax. |

| 2 | Employers must file Form 940 for the year in which they paid wages of $1,500 or more to employees or had at least one employee for some part of a day in any 20 or more different weeks. |

| 3 | FUTA tax, along with state unemployment systems, provides funds for paying unemployment compensation to workers who have lost their jobs. |

| 4 | The standard FUTA tax rate is 6.0%, but employers may receive a credit of up to 5.4% for state unemployment taxes paid, effectively reducing the FUTA tax rate to 0.6%. |

| 5 | Form 940 is due annually, by January 31, for the preceding year’s wages. However, if all FUTA taxes were deposited when due, the deadline is extended to February 10. |

| 6 | Employers can make FUTA tax payments quarterly, and they must use the Electronic Federal Tax Payment System (EFTPS) to make these payments. |

| 7 | If an employer's total FUTA tax liability for the year is $500 or less, they can pay the tax when filing Form 940, instead of making quarterly payments. |

| 8 | Certain types of employment and wages are exempt from FUTA tax, including wages paid to one's spouse or child under the age of 21, and certain state and local government employees. |

| 9 | Penalties for late filing of Form 940 or late payment of the FUTA tax can include charges of 5% of the unpaid tax for each month or part of a month the return is late, up to 25%. |

| 10 | For state-specific forms related to unemployment taxes, employers must comply with the laws of the states where their employees work, as these can vary widely. |

After completing the IRS 940 form, your next steps involve ensuring all the information provided is accurate, signing the document, and determining the right filing method for your needs—be it electronically or through mail. The IRS recommends double-checking the Employer Identification Number (EIN), the totals calculated for payments and adjustments, and your contact information. This action ensures the IRS can process your form without delays. Once reviewed and signed, choose your filing method based on convenience or IRS requirements. If you opt for mail, find the appropriate address for your state on the IRS website. For electronic filing, you may need to use IRS e-file or another approved electronic filing option. Remember to keep a copy of the form and any other documents submitted for your records.

What is the IRS 940 form?

The IRS 940 form, officially known as the "Employer's Annual Federal Unemployment (FUTA) Tax Return," serves a crucial role for businesses. It's designed to report the annual amount of unemployment tax that employers are required to pay on behalf of their employees. This tax contributes to the federal government's ability to oversee unemployment benefits to those who have lost their jobs.

Who needs to file the IRS 940 form?

Generally, the obligation to file the IRS 940 form falls upon businesses that have either paid wages of $1,500 or more to employees in any quarter of the calendar year or had at least one employee working for some part of a day in any 20 or more different weeks of the year. This requirement holds regardless of whether the employees are full-time, part-time, or temporary.

When is the IRS 940 form due?

The deadline to file the IRS 940 form is January 31st of the following year. If an employer has made all FUTA tax payments on time throughout the year, the IRS may extend the filing deadline to February 10. It’s critical for businesses to adhere to this timeline to avoid potential penalties for late filing.

What information is needed to complete the IRS 940 form?

To accurately complete the IRS 940 form, employers need several pieces of information. This includes the total amount of employee wages paid during the calendar year, the amount of FUTA tax that has been deposited, and any adjustments to state unemployment insurance contributions. The form is also designed to calculate the employer’s FUTA tax liability and any overpayments that may be credited to the next year’s return.

How are FUTA taxes calculated?

FUTA taxes are calculated at a rate of 6.0% on the first $7,000 paid to each employee as wages during the year. However, employers who pay their state unemployment taxes in full and on time may receive a credit of up to 5.4%, effectively reducing their FUTA tax rate to 0.6%. This mechanism underscores the importance of timely state tax payments in reducing federal unemployment tax liabilities.

Can I e-file the IRS 940 form?

Yes, employers have the option to e-file the IRS 940 form through the IRS e-file system. This modernized e-file method not only streamlines the filing process but also ensures the security of the transmitted information. Employers can use IRS-approved software or a tax professional who is an authorized IRS e-file provider to file the form electronically.

What happens if I file the form late or fail to pay the FUTA tax?

Late filing of the IRS 940 form or delayed payment of the FUTA tax can result in penalties and interest charges. The IRS calculates penalties based on how late the form and payments are, with interest accruing on unpaid taxes from the due date of the return. Employers are encouraged to file and pay as promptly as possible to minimize these additional charges.

Can I make corrections to a previously filed IRS 940 form?

Yes, employers have the ability to correct previously filed IRS 940 forms. This can be done by filling out and submitting an amended return. The process for making corrections is detailed in the instructions for the form, guiding employers on how to report and remit any additional FUTA tax liability.

Where can I find assistance with the IRS 940 form?

Employers seeking assistance with the IRS 940 form can find resources through several avenues. The IRS website offers comprehensive guides and the form's instructions. Additionally, tax professionals and IRS-approved e-file providers can offer expert guidance tailored to an employer's specific situation, ensuring compliance with federal tax obligations.

The process of filing the IRS 940 form, which is essential for reporting annual Federal Unemployment Tax Act (FUTA) tax, can sometimes be daunting. One common mistake made is the inaccurate calculation of FUTA tax. Employers must pay close attention to the IRS guidelines regarding what constitutes taxable wages and apply the correct tax rate. An incorrect calculation can lead to either an underpayment or an overpayment, each carrying its own set of complications.

Another frequent error is not taking full advantage of available credits. The 940 form allows employers to claim credits for amounts paid into state unemployment funds. Neglecting these credits or misreporting them can significantly increase the amount of FUTA tax owed, thus missing an opportunity to reduce the tax burden.

Employers often overlook the necessity of detailing state unemployment contributions on the form. This information is crucial, especially for businesses that operate across multiple states. The IRS needs to know how much was paid to each state to accurately calculate the potential credit reduction. Failure to provide this information may lead to incorrect processing of the form and potential penalties.

A clerical yet critical mistake is incorrect employer information, including the Employer Identification Number (EIN). Such discrepancies may seem minor but can cause significant delays in processing. The IRS relies on accurate employer identification to properly credit tax payments to the correct account. An incorrect or missing EIN can lead to unanticipated complications, including the assessment of penalties.

Not filing on time is another common oversight. The deadline for filing Form 940 is January 31st, following the end of the tax year. Missing this deadline can result in penalties and interest charges. It is crucial for employers to keep track of this date and ensure that they allocate sufficient time for the completion and submission of the form.

Underestimating the importance of record-keeping related to Form 940 filing is yet another misstep. The IRS may require documentation to support the amounts reported, including payroll records and state unemployment tax contributions. Failure to maintain these records can lead to challenges in verifying the accuracy of the form should the IRS have questions or initiate an audit.

Lastly, attempting to navigate the complexities of Form 940 without seeking assistance when needed can be a mistake. Misunderstandings of the form’s requirements and tax law nuances can lead to errors. Many employers benefit from consulting with a tax professional or utilizing IRS resources to ensure accurate and compliant completion of the form.

In conclusion, while the task of filling out the IRS Form 940 can seem straightforward, it is fraught with potential pitfalls. By being aware of these common mistakes and taking steps to avoid them, employers can ensure they remain compliant with FUTA tax requirements while minimizing their tax liability and avoiding unnecessary penalties.

Filing taxes can often seem like navigating a maze with all the forms and documents one needs to complete. The IRS 940 form, commonly required for reporting annual Federal Unemployment Tax Act (FUTA) tax, is just the beginning for many businesses. Along with this crucial form, there are several other documents businesses may need to prepare and file to fully comply with tax regulations. Below is a list of up to seven forms and documents commonly used in conjunction with the IRS 940 form.

Understanding and utilizing these forms correctly can be pivotal in achieving compliance with tax regulations and minimizing business tax liabilities. Each document has a specific purpose and set of requirements, underscoring the importance of meticulously preparing your tax filings. If there are any uncertainties, it's always a wise strategy to consult with a tax professional or an accountant who can provide guidance tailored to your business's unique situation.

The IRS 940 form, known as the Employer's Annual Federal Unemployment (FUTA) Tax Return, shares similarities with several other tax documents. One of these is the IRS Form 941, the Employer's Quarterly Federal Tax Return. The 941 form is used by employers to report income taxes withheld from employees' paychecks, and the employees' portion of Social Security and Medicare taxes. Like the 940, it deals with employment taxation but focuses on reporting on a quarterly basis rather than annually.

Another document similar to the IRS 940 is the IRS Form 944, Employer’s Annual Federal Tax Return. This form is designed for smaller employers to file and pay the aforementioned taxes once a year instead of quarterly. While the 940 form addresses unemployment tax specifically, the 944 form allows small business employers to report income tax and other payroll taxes on an annual schedule, making it a simpler alternative for those eligible.

The IRS Form 1099-MISC is also comparable in some aspects. This form is used to report miscellaneous income, such as payments to independent contractors. While it serves a very different purpose from the IRS 940 form, focusing instead on non-employee compensation, it similarly involves reporting obligations of the employer or business entity. Both forms play crucial roles in ensuring the correct reporting and taxation of payments, although to different recipients — employees versus non-employees.

Lastly, the State Unemployment Tax Act (SUTA) forms, while not a single standardized federal form like the IRS 940, are related in their purpose. Every state requires employers to report income and pay unemployment taxes, similar to the FUTA tax at the federal level. The specifics of these forms vary from state to state, but their function aligns closely with the objectives of the 940 form: to fund unemployment insurance benefits for workers who have lost their jobs. Thus, both FUTA and SUTA taxes represent parallel systems operating at different governmental levels.

Filling out the IRS 940 form, which is essential for reporting your annual Federal Unemployment Tax Act (FUTA) tax, requires careful attention to detail. Here are six dos and don'ts to help you accurately complete the form and ensure compliance with the tax code.

Do:The IRS Form 940 often comes surrounded by misconceptions that can lead to confusion and mistakes when businesses prepare their annual federal unemployment tax filings. To clear up some of the common misunderstandings, here’s a list that sheds light on the facts:

Only big companies need to file: This is a common mistake. In reality, any business that paid wages of $1,500 or more in any quarter, or had at least one employee for a portion of a day in any 20 or more different weeks in a year, needs to file Form 940.

Filing Form 940 means you’re done with unemployment taxes: Not quite. Form 940 only covers federal unemployment taxes. Businesses often must also pay state unemployment taxes and file separate state unemployment tax forms.

You can file Form 940 anytime during the year: Actually, there's a deadline. Form 940 is due annually, and the deadline to file is January 31st for the previous year's taxes, although you have until February 10th if you deposited all the FUTA tax when it was due.

All wages paid to employees are subject to FUTA tax: Not all wages are taxable for FUTA. For example, payments for group term life insurance, retirement/pension contributions, and many fringe benefits are not considered taxable wages for FUTA purposes.

Calculating FUTA tax is simple and straightforward: Calculating FUTA tax can get complicated. You must understand which wages are subject to FUTA tax and the impact of state unemployment taxes on your FUTA tax rate. It’s not simply a flat rate applied across all wages.

You must pay FUTA taxes quarterly: This concept is slightly off. While Form 940 is filed annually, FUTA tax payments must be made quarterly if the owed amount is over $500.

If you missed the deadline, it’s too late to file: Even if you missed the January 31st deadline, you should still file Form 940 as soon as possible. Late filing may result in penalties, but the sooner you file, the lower those penalties might be.

FUTA taxes are taken out of employee wages: This is incorrect. Unlike other payroll taxes, FUTA taxes are paid solely by the employer. They are not deducted from an employee’s wages.

Only full-time employees count when determining if you need to file: When determining if you meet the criteria for filing Form 940, all employees count, including part-time and temporary employees, not just full-time ones.

Understanding these points about Form 940 can help businesses navigate their responsibilities when it comes to federal unemployment taxes more effectively, ensuring compliance and avoiding unnecessary penalties.

Filing the IRS 940 form is critical for employers, as it relates to unemployment taxes at the federal level. Understanding this form can ensure compliance and prevent potential penalties. Here are six key takeaways about filling out and using the IRS 940 form:

By paying attention to these key aspects of the IRS 940 form, employers can fulfill their legal obligations, contribute to the unemployment system, and avoid unnecessary penalties. Understanding the details and requirements for filing this form is an essential part of managing a business responsibly.

Dd 214 - The form is frequently requested by employers as proof of military service and experience.

Chemical Service Waiver Form - This agreement form ensures clients are aware of and accept the possible effects and costs related to their chemical hair treatments.