Fill a Valid IRS Schedule B 941 Form

Fill a Valid IRS Schedule B 941 Form

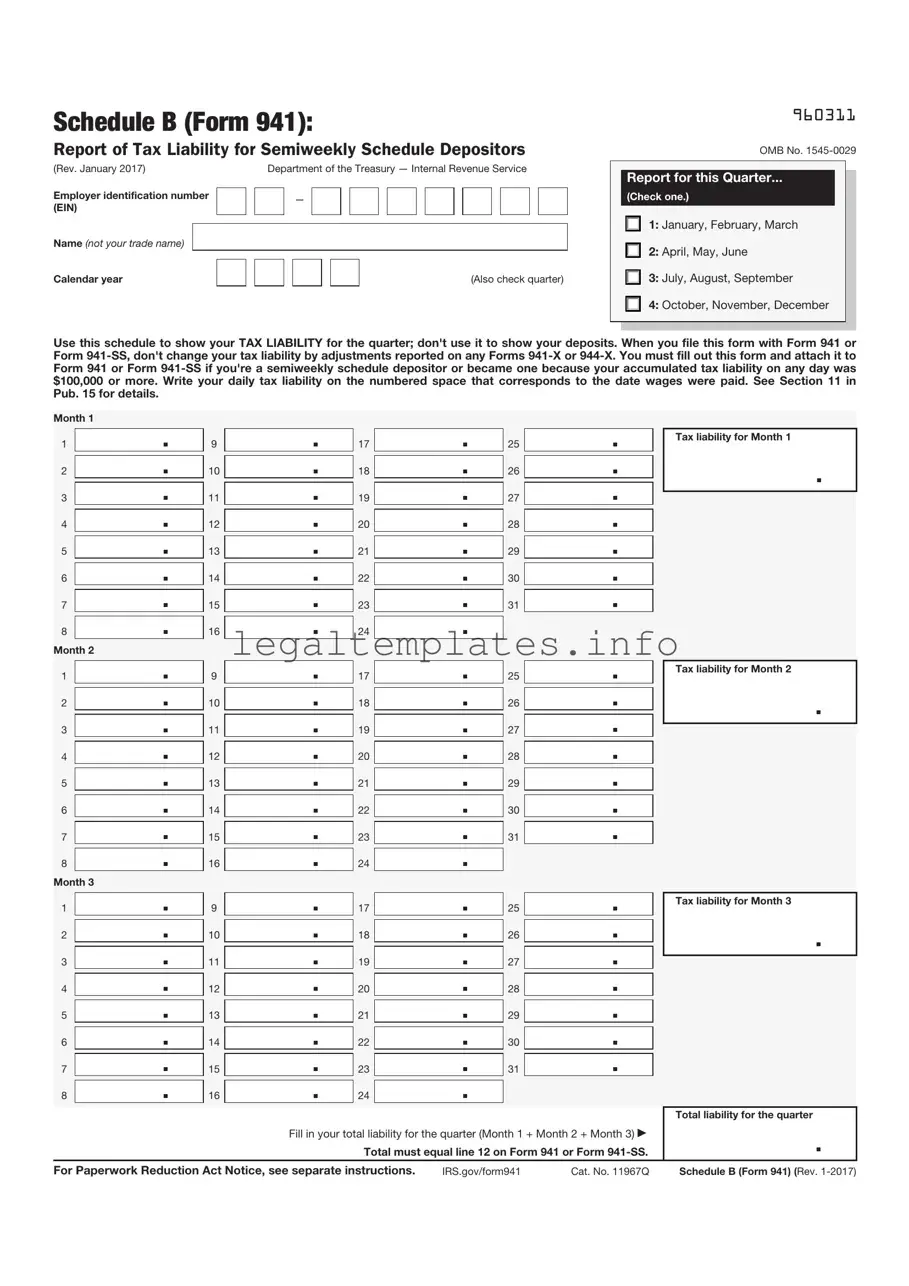

When navigating the complexities of payroll tax reporting, employers find themselves facing the task of accurately documenting and submitting various forms to the Internal Revenue Service (IRS). Among these, the IRS Schedule B (Form 941), stands out due to its specific requirements and significance. This particular document is intricately linked with Form 941, the Employer's Quarterly Federal Tax Return, and serves a crucial role for businesses that withhold income tax, social security tax, or Medicare tax from employees' wages. The essence of Schedule B lies in its detailed reporting of the tax liability for each payroll period within a quarter. Understanding its purpose, knowing when it is mandatory, and grasplying the nuances of accurate completion can significantly streamline the quarterly tax filing process. Employers, especially those who find themselves on a semi-weekly deposit schedule or have accumulated a tax liability of $100,000 or more on any given day during the quarter, must pay particular attention to Schedule B's requirements to ensure compliance and avoid potential penalties.

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. January 2017) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don't use it to show your deposits. When you file this form with Form 941 or Form

Month 1

1 .

.

2 .

.

3 .

.

4 .

.

5 .

.

6 .

.

7 .

.

8 .

.

Month 2

1 .

.

2 .

.

3 .

.

4 .

.

5 .

.

6 .

.

7 .

.

8 .

.

Month 3

9 .

.

10 .

.

11 .

.

12 .

.

13 .

.

14 .

.

15 .

.

16 .

.

9 .

.

10 .

.

11 .

.

12 .

.

13 .

.

14 .

.

15 .

.

16 .

.

17 .

.

18 .

.

19 .

.

20 .

.

21 .

.

22 .

.

23 .

.

24 .

.

17 .

.

18 .

.

19 .

.

20 .

.

21 .

.

22 .

.

23 .

.

24 .

.

25 .

.

26 .

.

27 .

.

28 .

.

29 .

.

30 .

.

31 .

.

25 .

.

26 .

.

27 .

.

28 .

.

29 .

.

30 .

.

31 .

.

Tax liability for Month 1

.

Tax liability for Month 2

.

1 |

|

. |

9 |

|

. |

17 |

|

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

18 |

|

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

19 |

|

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

20 |

|

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

21 |

|

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

22 |

|

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

23 |

|

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

24 |

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3) |

. |

|||||||||

|

|

|

|

|

|

Total must equal line 12 on Form 941 or Form |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

IRS.gov/form941 |

Cat. No. 11967Q |

Schedule B (Form 941) (Rev. |

|||||||||||

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Schedule B (Form 941) is used by employers to report tax liability for semiweekly schedule depositors or to explain tax liability amounts if they differ from the amount shown on Form 941. |

| Who Must File | Employers who have accumulated tax liability of $100,000 or more on any given day during a monthly or quarterly reporting period must file Schedule B (Form 941). |

| Filing Frequency | This form is filed quarterly, alongside Form 941, by those employers who fall under the semiweekly deposit schedule. |

| Due Dates | Schedule B (Form 941) is due by the last day of the month following the end of the quarter. For Q1, it's due by April 30; Q2 by July 31; Q3 by October 31; and Q4 by January 31. |

| Document Structure | The form consists of lists for reporting taxes, including columns for the date, tax liability amounts, and total liability for the reporting period. |

| Relevant Governing Law | Schedule B (Form 941) is governed by federal tax law, specifically under the Internal Revenue Code (IRC) and its regulations overseen by the Internal Revenue Service (IRS). |

Navigating IRS forms can often feel overwhelming, but understanding how to accurately complete them is crucial for compliance and avoiding unnecessary penalties. Schedule B (Form 941) is specifically designed for employers who report taxes semiweekly or those that have accumulated $100,000 or more in taxes on any given day during the reporting period. Properly filling out this form ensures your tax payments are adequately recorded. The following step-by-step guide will help to demystify the process, making it more accessible and manageable.

Completing Schedule B (Form 941) accurately is a vital part of maintaining compliance with IRS tax reporting requirements. By following these steps, employers can ensure their tax liabilities are correctly reported, which helps in avoiding penalties and potential issues with the IRS. Remember, this form is an accompaniment to your main Form 941, so it should be prepared with the same level of care and accuracy.

What is the purpose of the IRS Schedule B (Form 941)?

The IRS Schedule B (Form 941) is a tax form used by employers who withhold income tax from wages, or who must pay Medicare and Social Security taxes. This form serves to report the employer's liability for these taxes on a semi-weekly schedule or to explain adjustments to these amounts. Employers use it alongside the primary Form 941, Employer's Quarterly Federal Tax Return.

Who needs to file the IRS Schedule B (Form 941)?

Employers who report more than $50,000 in taxes during the lookback period or have accumulated a liability of $100,000 or more on any day during the deposit schedule, are required to file the IRS Schedule B (Form 941). This form is specifically designed for those who follow a semi-weekly deposit schedule. Entities that deposit monthly do not need to file this schedule unless directed by the IRS.

How is the lookback period determined for IRS Schedule B (Form 941)?

The lookback period plays a significant role in determining if an employer must file Schedule B. It is a period that helps identify the employer's tax liability and thereby their deposit schedule. The lookback period for Form 941 is the four quarters ending on June 30 of the prior year. If the employer reported $50,000 or less in taxes during this period, they follow a monthly schedule and are not required to file Schedule B unless directed otherwise by the IRS.

What information is required when filling out Schedule B (Form 941)?

When completing Schedule B, employers must provide their Employer Identification Number (EIN), the name associated with that EIN as registered with the IRS, and the quarter to which the Schedule B is being applied. Additionally, the form requires detailed information on tax liabilities for each semi-weekly period within the quarter. Accurate daily records of tax liabilities are crucial for completing this form correctly.

Can adjustments be made with IRS Schedule B (Form 941)?

While the primary purpose of Schedule B is to report the employer's federal tax liabilities on a semi-weekly basis, adjustments to tax liabilities reported in previous quarters can also be made with this form. However, these adjustments must be detailed and thoroughly documented to ensure accuracy and compliance with IRS regulations.

What is the deadline for filing IRS Schedule B (Form 941)?

IRS Schedule B must be filed with Form 941 by the quarterly deadlines, which are April 30, July 31, October 31, and January 31 for the respective quarters. It is important to adhere to these deadlines to avoid penalties and interest for late submissions. Employers must ensure that they accurately report their tax liabilities for each semi-weekly period to comply with federal tax requirements.

Filling out the IRS Schedule B form for the 941 can be tricky, and it's easy to stumble over some common errors if you're not careful. One of the most frequent mistakes is not aligning the payroll schedule accurately with the deposit schedule. Each business has a unique payroll frequency, and it's crucial to report taxes based on the specific timeframe your business operates within. Misaligning schedules can lead to incorrect tax calculations and subsequently incorrect tax payments.

Another error often seen is failing to report all tax liabilities for the quarter. It's essential to account for every employee when calculating payroll taxes. Overlooking even a single employee can lead to underreported tax liabilities, which can result in penalties and interest charges from the IRS.

Neglecting to double-check the mathematics is also a common pitfall. Arithmetic errors, while simple, can have significant consequences on the total tax liability reported. Ensuring that all calculations are accurate and that totals add up correctly is crucial to submitting an accurate Schedule B.

Many businesses forget to include adjustments for tips and sick pay. These items have specific tax implications and must be reported accurately on Schedule B. Not accounting for them can lead to discrepancies in reported tax liabilities.

A critical error is not considering prior balance due or overpayment. If your business had a balance due or an overpayment from a previous quarter, this must be factored into the current quarter's tax liabilities. Failure to do so can lead to inaccuracies in the amount of tax owed or refundable.

Incorrect Tax ID numbers or employer identification information is another area where errors are common. Ensuring that all identifying information is accurate and matches the records of the IRS is vital for processing your Schedule B correctly.

Sometimes, filers mistakenly skip lines or sections applicable to their business operations. Every line of Schedule B is there for a reason, and missing information can convey an incomplete picture of your tax liabilities.

Another mistake lies in not understanding the difference between taxes owed and deposits made. Schedule B requires a careful reconciliation of taxes due and the actual tax deposits. Confusing these can lead to improper tax filings.

Failure to sign and date the form is also a surprisingly frequent oversight. An unsigned or undated form is considered incomplete by the IRS and can be rejected, leading to delays in processing.

Lastly, not using the electronic filing systems provided by the IRS can be a misstep. Electronic filings are processed quicker and with fewer errors due to the built-in checks that identify common mistakes before submission. Avoiding this resource can increase the risk of errors and the time it takes for your filing to be acknowledged.

When preparing and submitting the IRS Schedule B (941) form, which is essential for reporting taxes associated with employment on a more frequent, often quarterly, basis, a range of additional forms and documents may also be required to ensure comprehensive compliance and accurate tax reporting. These supplementary forms play a crucial role in providing detailed information related to various aspects of payroll taxes. They are designed to complement the data provided in Schedule B by offering more in-depth details or covering other aspects of tax reporting not addressed by Schedule B directly.

Together, these forms create a framework that supports employers in their duty to accurately report and pay federal taxes. Each document has been designed to capture specific types of data or transactions, ensuring that all aspects of employment taxation are addressed systematically. Employers should remain vigilant in understanding which forms are relevant to their specific circumstances and be meticulous in their preparation and submission to comply fully with federal tax obligations.

The IRS Schedule B (Form 941) is closely akin to the IRS Form 940, which is the Federal Unemployment Tax Annual Report. Both of these forms are pivotal for employers, as they relate to reporting taxes withheld from employees' wages. The Form 940, similar to Schedule B, necessitates detail on taxes collected for unemployment, pinpointing the total amount due to the IRS. The primary distinction is their frequency and the type of tax reported, with Form 940 being annual and focusing on unemployment taxes, while Schedule B is more frequent and concentrates on withholding taxes.

Another document that resembles the IRS Schedule B (Form 941) is the IRS Form 945. This form is used to report withheld federal income tax from non-payroll payments, including gambling winnings, pension distributions, and backup withholding. Like Schedule B, Form 945 plays a crucial role in ensuring taxes withheld are properly reported to the IRS. Both necessitate meticulous record-keeping and accurate reportage of withheld taxes, albeit for different income sources.

The W-2 form, issued by employers, is another document that shares characteristics with the IRS Schedule B (Form 941). W-2 forms detail an employee's annual wages and the amount of taxes withheld from their paycheck. In essence, the information from W-2 forms feeds into what is reported on Schedule B and the summary Form 941, making them interlinked in the tax reporting process. Both serve the fundamental purpose of communicating to the IRS what has been withheld from employees' earnings, albeit at different stages and perspectives in the reporting cycle.

IRS Form W-3, the Transmittal of Wage and Tax Statements, also aligns closely with the Schedule B (Form 941) in purpose and function. Form W-3 is essentially the summary form accompanying all filed W-2 forms to the Social Security Administration, summarizing the total employee earnings, Social Security wages, and Medicare wages reported by an employer. Although it's directed to a different government agency, it complements the wage and tax reporting process integral to Schedule B, emphasizing aggregated data over the periodic details Schedule B captures.

Similarly, the IRS Form 1099 series, particularly Form 1099-MISC, used for reporting miscellaneous income payments, shares similarities with Schedule B (Form 941) in the broader context of tax reporting. Like Schedule B, various 1099 forms are crucial for reporting certain types of payments and the associated withholdings outside of the traditional employer-employee relationship. Both forms are essential in providing the IRS with a comprehensive view of taxable income and withholdings, albeit for different income categories.

Last but not least is the IRS Form 1096, which is akin to the transmittal letter for all 1099 forms sent to the IRS. This form is a summary report that accompanies the submission of Forms 1099, similar to how Form W-3 accompanies W-2 forms. While IRS Form 1096 differs in its specific function and the types of income it pertains to, it shares the broad objective of Schedule B (Form 941) in collating and summarizing tax-related information before it is submitted to the federal tax authorities. This ensures that the data reported is organized and facilitates the reconciliation of amounts reported with amounts withheld or paid.

Filling out the IRS Schedule B (Form 941) requires attention to detail and an understanding of your business’s payroll tax obligations. This form is used to report tax liability for semiweekly schedule depositors. To ensure accuracy and compliance, here are six dos and don'ts you should consider:

Do:The IRS Schedule B (Form 941) is surrounded by myths and misunderstandings that can perplex even seasoned business owners. Let's demystify some of these misconceptions to ensure you're approaching your tax obligations with clarity and confidence.

It's only for large businesses: A common belief is that Schedule B (Form 941) is designed exclusively for big corporations. In reality, it's used by employers who withhold federal income tax, social security tax, or Medicare tax from employees' paychecks, regardless of the size of their business. If you pay wages subject to these withholdings, you're likely required to file Schedule B with your Form 941.

It's filed annually: Contrary to what some may think, Schedule B (Form 941) is not an annual filing requirement. It's actually submitted quarterly. Employers need to stay on top of this schedule to avoid penalties for late submissions.

It's the same as Form 941: Mixing up Schedule B with Form 941 itself is easy but mistaken. While closely related, Schedule B is a supplementary document that details the tax liability for each pay period within the quarter. Form 941, on the other hand, provides a summary of the taxes owed and paid.

Penalties aren't a big deal: Some people underestimate the consequences of filing Schedule B late or inaccurately. The IRS can impose severe penalties, including fines and interest on unpaid taxes. Ensuring timely and correct filing is crucial to avoid these financial setbacks.

Electronic filing is optional: In today's digital age, electronic filing is often seen as a convenience rather than a requirement. However, the IRS mandates electronic filing for all employers required to file Schedule B (Form 941), provided they meet certain criteria, such as employing a specific number of employees or owing a certain amount in taxes.

Corrections are prohibited: Discovering an error after submission doesn't mean you're out of luck. Amendments are allowed and should be made using Form 941-X. It's important to correct inaccuracies to ensure compliance and correct tax reporting.

It can be ignored if you missed a quarter: Missing a filing doesn't mean you can or should skip submitting Schedule B for that quarter. If you fail to file, it's best to remedy the situation as soon as possible. Ignoring missed filings can lead to increased penalties and interest charges.

Personal income affects reporting: The belief that an employer's personal income impacts their Schedule B reporting is unfounded. Schedule B focuses solely on the taxes withheld from employees' wages, not the employer's personal financial situation.

Understanding the intricacies of Schedule B (Form 941) can save businesses from unnecessary headaches and financial penalties. By dispelling these myths, employers can ensure they remain compliant, avoid common pitfalls, and maintain a healthy relationship with the IRS.

Filing the IRS Schedule B (Form 941) is a crucial process for employers who report taxes withheld from employees' wages, Medicare taxes, and social security. Successfully navigating this process ensures compliance with the Internal Revenue Service (IRS) requirements and avoids potential penalties. Here are key takeaways to consider when filling out and using the IRS Schedule B (Form 941):

Complying with IRS requirements for filing Schedule B (Form 941) underscores a business's commitment to responsible tax reporting. By focusing on accuracy, timeliness, and adhering to the IRS guidelines, employers can navigate this process smoothly and maintain their compliance status.

Paycheck Template - Understanding deductions on your pay stub can lead to more informed financial decisions and tax planning.

Does an Advance Directive Need to Be Notarized in California - It aids in avoiding conflicts or confusion among family members by clearly stating the individual's health care preferences in writing.

Employee Application - An Employment Application PDF form is a standardized document that job applicants use to provide personal and professional information to potential employers.