Fill a Valid IRS W-3 Form

Fill a Valid IRS W-3 Form

At the heart of federal tax reporting for employers lies the IRS W-3 form, a crucial document that consolidates the total earnings, Social Security wages, Medicare wages, and withholding for all employees over the tax year. Often seen as the companion piece to the more familiar W-2 forms handed out to employees, the W-3 plays a pivotal role in ensuring that payroll information is accurately communicated to the Social Security Administration (SSA). It's not a form that employees will ever need to fill out, but rather one that demands meticulous attention from employers as it aggregates individual employee data into a single report. The importance of the W-3 form cannot be overstated, as it not only facilitates compliance with federal regulations but also supports the efficient operation of social welfare programs by providing a snapshot of workforce compensation. Submission errors or delays can lead to penalties, underscoring the need for employers to handle this form with care. This introductory glimpse into the W-3 form sheds light on its purpose, significance, and the obligations it places on employers within the ecosystem of federal tax reporting.

Attention:

You may file Forms

The maximum amount of dependent care assistance benefits excludable from income may be increased for 2021. The American Rescue Plan Act of 2021 permits employers to increase the amount of dependent care benefits under their plans that can be excluded from an employee’s income from $5,000 ($2,500 for married filing separately) to up to $10,500 ($5,250 for married filing separately). See section C of Notice

Internal Revenue Bulletin:

Note: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file Copy A downloaded from this website with the SSA; a penalty may be imposed for filing forms that can’t be scanned. See the penalties section in the current General Instructions for Forms

Please note that Copy B and other copies of this form, which appear in black, may be downloaded, filled in, and printed and used to satisfy the requirement to provide the information to the recipient.

To order official IRS information returns such as Forms

See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms.

DO NOT STAPLE

33333

b

Kind of Payer

(Check one)

a Control number |

|

|

For Official Use Only ▶ |

||

|

|

|

|

|

OMB No. |

|

941 |

Military |

943 |

|

944 |

▲ |

|

||||

|

|

|

|

Kind |

|

|

|

Hshld. |

Medicare |

of |

|

|

Employer |

||||

|

emp. |

govt. emp. |

|||

|

|

|

|

|

(Check one) |

▲

None apply |

501c |

|||||||||

|

|

|

|

|

|

|

|

sick pay |

||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

(Check if |

||

State/local |

State/local 501c Federal govt. |

|||||||||

applicable) |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

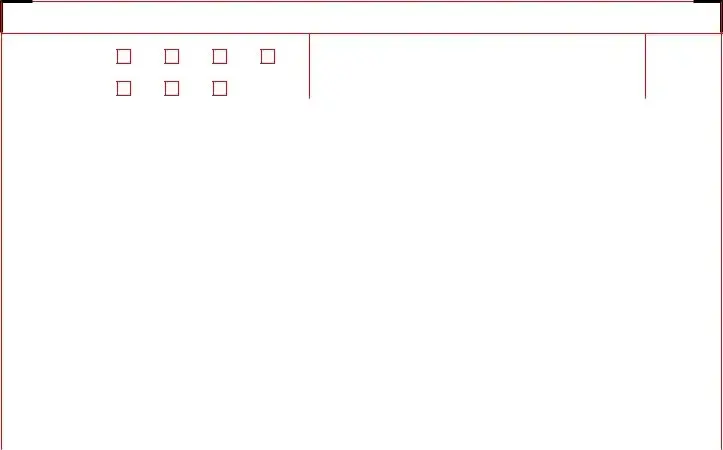

c Total number of Forms |

|

d Establishment number |

1 Wages, tips, other compensation |

2 Federal income tax withheld |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

e Employer identification number (EIN) |

3 Social security wages |

4 Social security tax withheld |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f Employer’s name |

|

5 |

Medicare wages and tips |

6 Medicare tax withheld |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

8 Allocated tips |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

|

10 Dependent care benefits |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

11 Nonqualified plans |

12a Deferred compensation |

|

||||

|

g Employer’s address and ZIP code |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

|

h Other EIN used this year |

|

13 For |

12b |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|||||

|

15 State |

Employer’s state ID number |

14 Income tax withheld by payer of |

|

||||||||

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 State wages, tips, etc. |

|

17 State income tax |

18 Local wages, tips, etc. |

19 Local income tax |

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Employer’s contact person |

|

|

Employer’s telephone number |

For Official Use Only |

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Employer’s fax number |

|

|

Employer’s email address |

|

|

|

|

||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return and accompanying documents, and, to the best of my knowledge and belief, they are true, correct, and complete.

Signature ▶ |

Title ▶ |

|

Date ▶ |

Form |

2022 |

Department of the Treasury |

|

Internal Revenue Service |

|||

Send this entire page with the entire Copy A page of Form(s)

Do not send any payment (cash, checks, money orders, etc.) with Forms

Reminder

Separate instructions. See the 2022 General Instructions for Forms

Purpose of Form

Complete a Form

The SSA strongly suggests employers report Form

•

•File Upload. Upload wage files to the SSA you have created using payroll or tax software that formats the files according to the SSA’s Specifications for Filing Forms

When To File Paper Forms

Mail Form

Where To File Paper Forms

Send this entire page with the entire Copy A page of Form(s)

Social Security Administration

Direct Operations Center

Note: If you use “Certified Mail” to file, change the ZIP code to

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions.

Cat. No. 10159Y

| Fact Name | Description |

|---|---|

| Purpose | The IRS W-3 form is a summary/transmittal form used to report total earnings, Social Security wages, Medicare wages, and withholding for all employees for the previous year. |

| Who Must File | Employers who file Form W-2, Wage and Tax Statement, must also file Form W-3 to transmit Copy A of Forms W-2 to the Social Security Administration. |

| Deadline | The form must be filed with the Social Security Administration by January 31st of the year following the reported wages. |

| Electronic Filing | Employers filing 250 or more Form W-2s must file both forms W-2 and W-3 electronically, unless the IRS grants a waiver. |

Filing the IRS W-3 form accurately is necessary for employers to summarize their total earnings, taxes withheld, and other payroll information for the year. This summary supports the individual W-2 forms sent to employees and the Social Security Administration (SSA). Below, find a detailed list of steps to complete this form. Remember, accuracy is paramount, as errors can lead to unnecessary delays and complications.

After the IRS W-3 form is filled out and submitted, it's crucial to keep a copy for your records. Should the IRS or SSA request more information, having this documentation readily available will make responding easier. Timeliness and accuracy in this process not only comply with federal regulations but also ensure that employees' earnings and deductions are correctly reported for their personal tax filings.

What is a W-3 form?

The W-3 form, formally known as the Transmittal of Wage and Tax Statements, is a document used in the United States to summarize an employer's total earnings, Social Security wages, Medicare wages, and withholding for all employees for the previous year. It is typically submitted to the Social Security Administration (SSA) along with a copy of each employee's W-2 form, which outlines individual earnings and deductions. The form functions as a cover sheet for the W-2 forms being sent.

When is the W-3 form due?

The deadline for submitting the W-3 form, along with the W-2 forms for employees, is January 31st of the year following the reported tax year. For instance, for wages paid during the 2022 tax year, the W-3 form must be submitted by January 31, 2023. This deadline applies whether the forms are filed electronically or by mail. It's important to meet this deadline to avoid potential penalties for late filing.

Who needs to file a W-3 form?

Any employer who sends out W-2 forms must also file a W-3 form. This includes all businesses, large or small, that have employees from whom income, social security, or Medicare tax was withheld. This also applies to businesses that would otherwise not withhold taxes because they paid wages of $600 or more to an employee during the year. Nonprofit organizations, households employing domestic workers, and government agencies are also required to file if they meet these criteria.

How is the W-3 form submitted?

The W-3 form can be submitted either electronically or by mail. Many employers find electronic filing to be easier and more efficient, and it is the required method for employers who are submitting W-2 forms for 250 or more employees. The Social Security Administration encourages all employers to file electronically regardless of the number of W-2 forms they are submitting. When mailing, the form must be sent to the address provided by the SSA specifically for W-2/W-3 submissions. It's critical to use the current year's form and to verify the mailing address each year, as it can change.

Filing tax documents is a critical responsibility for both individuals and businesses alike. One common form that often presents challenges is the IRS W-3, Transmittal of Wage and Tax Statements. This form summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the year. While it may seem straightforward, errors in filling out this form can lead to unnecessary delays and complications. Here are eight mistakes to avoid.

Firstly, a common mistake is incorrect employer information. This includes errors in the Employer Identification Number (EIN), employer name, and address. It's crucial to double-check these details for accuracy because they must match the information the IRS has on file. Incorrect information can result in processing delays or misfiled documents.

Another frequent error involves inaccuracies in employee wage and tax information. Each figure needs to be precisely reported to avoid discrepancies. Incorrect reporting can lead to audits or penalties. Be as meticulous as possible when transferring numbers to ensure everything matches up to the payroll records.

Failure to report all necessary data can also be problematic. The W-3 form requires a detailed account of wages, tips, other compensation, income tax withheld, Social Security taxes, and more. Missing any of these details can lead to incomplete filings, which can result in penalties.

Incorrect calculation of Social Security and Medicare wages is another common error. Due to the caps on taxable income for these programs, not all wages may be subject to taxes. Ensure the calculations accurately reflect these caps to avoid underpaying or overpaying taxes.

Some filers mistakenly use the form for the wrong year. Tax forms and their requirements can change annually. Always verify that you're using the most current version of the W-3 form to comply with the latest tax laws and guidelines.

Another oversight is neglecting to sign the form. An unsigned W-3 form is considered incomplete by the IRS. Ensure that the designated official or the employer signs the form before submission.

Incorrect filing status can cause headaches, too. The W-3 form must be filed along with the correct copies of Form W-2 for each employee. Mixing up these forms, or failing to include all necessary copies, can lead to processing errors.

Last but not least, missing the filing deadline can result in late fees and penalties. It's important to keep track of the filing deadline, which is typically January 31st, to ensure timely submission. Postponing the task can lead to costly mistakes.

In summary, filling out the IRS W-3 form requires attention to detail, accurate calculations, and adherence to deadlines. By avoiding these common mistakes, employers can ensure a smoother filing process, keep in good standing with tax authorities, and maintain accurate records for both the business and its employees.

When dealing with the Internal Revenue Service (IRS), businesses must familiarize themselves with a variety of forms and documents, particularly when processing payroll. The IRS W-3 form, which serves as a summary of employee wages and tax withholdings for the year, is often accompanied by other important documents. These documents are essential for proper reporting and compliance with tax laws. Each form plays a role in ensuring the accuracy of financial and tax information submitted to the IRS. Here is a list of forms and documents often used alongside the IRS W-3 form.

Understanding each of these documents and how they relate to the IRS W-3 form is crucial for businesses to maintain compliance with IRS regulations. Careful and accurate preparation of these forms ensures the financial integrity of the employer's tax records and contributes to the smooth operation of payroll processes. Professional advice and assistance can be valuable for navigating these requirements.

The IRS W-2 form shares similarities with the W-3 form, as it essentially serves as a summary report for the W-2 forms sent by an employer. The W-2 form reports an employee's annual wages and the amount of taxes withheld from their paycheck. Like the W-3, it is crucial for tax reporting purposes, but it is provided to both the IRS and the employee, detailing individual employment income and tax withheld.

Another document that bears resemblance to the W-3 form is the 1096 form, which is often used by businesses to summarize the information returns like 1099s, which are submitted to the IRS. Just like the W-3 summarizes W-2 information, the 1096 serves as a cover sheet that compiles the information from multiple forms of a different nature (e.g., independent contractor payments, dividends, interest payments) into a single document for IRS submission.

The 940 form, which employers use to report their annual Federal Unemployment Tax Act (FUTA) tax, shares some conceptual similarities with the W-3. Both forms are concerned with employment-related taxes, though the W-3 focuses on income tax, Social Security, and Medicare withholdings, whereas the 940 focuses on unemployment contributions. They both summarize data relevant to a specific tax reporting requirement for employers.

Form 941 is used by employers to report quarterly federal tax returns, encompassing withheld income tax, as well as employer and employee Social Security and Medicare taxes. Its resemblance to the W-3 lies in its function of reporting taxes related to employment, albeit on a quarterly basis for the 941, compared to the annual summary provided by the W-3.

The Schedule K-1 (Form 1065) document, while primarily for partnership income reporting, shares the general concept of summarizing and reporting income and tax information to the IRS, similar to what the W-3 does for wage and tax statements. The K-1, however, is specific to partners in a partnership, detailing their share of the business's income, deductions, and credits.

The W-4 form is closely related to the W-3 in the employment tax reporting process. Employees use the W-4 to inform employers of their withholding allowances, which directly influences the information reported on the W-2 and summarized in the W-3. The W-4 plays a proactive role by determining the amount of tax to be withheld, which is crucial for accurate W-3 reporting.

Form 1040, the U.S. individual income tax return, is indirectly related to the W-3 through the information it gathers. W-2 forms, which are summarized by the W-3, are used by individuals to fill out their 1040 forms, making the accuracy of the W-3 important for personal tax reporting and compliance.

The 1099-MISC form, used to report miscellaneous income such as payments to independent contractors, is akin to the W-2 and, by extension, the W-3 in its goal of reporting income and tax information to the IRS. While 1099 forms cover non-employee compensation, making the nature of the income different, the W-3's summarization of employment tax and income data serves a parallel purpose in the landscape of tax reporting.

Lastly, the W-7 form, used by individuals to apply for an IRS Individual Taxpayer Identification Number (ITIN), indirectly connects with the W-3's domain of tax reporting. Although it is more focused on identifying taxpayer eligibility, the ability to properly file and report taxes, which includes the accurate submission of forms like the W-3, can hinge on obtaining an ITIN through the W-7 for those who do not have a Social Security number.

Filling out the IRS W-3 form, a summary of all W-2 forms sent by an employer, is a critical task that requires attention to detail. Here are essential do's and don'ts to guide you through this process:

Understanding the IRS W-3 form is essential for businesses, but there are several misconceptions about it. Here’s a list of common misunderstandings and their clarifications:

Only large companies need to file the W-3 form. This is incorrect. Any business that submits W-2 forms for employees must also file a W-3 form. It serves as a summary of the information on the W-2 forms and is required regardless of the company's size.

The W-3 form can be filed anytime before the end of the tax year. This statement is false. The W-3 form, along with the W-2 forms, must be filed by January 31st of the year following the tax year being reported.

If you file W-2s electronically, you don't need to file a W-3. This is a misconception. Even if you file W-2 forms electronically, the IRS still requires a W-3 submission. The W-3 form summarizes the information reported on the W-2s.

You must mail the W-3 form to the IRS. This isn't the only option. While mailing is a traditional method, electronic filing is also available and encouraged by the IRS for its convenience and efficiency.

The W-3 form is complex and requires special software to complete. While specialized payroll software can simplify the process, it's not necessary to use it. Small businesses without complex payroll systems can still complete and file a W-3 form with basic information from their W-2 forms.

Corrections to W-2 forms don't affect the W-3 form. Actually, if W-2 forms are corrected after the W-3 has been submitted, a corrected W-3 form, called a W-3c, must also be filed to reflect these changes.

You can request an extension for filing the W-3 form. Unlike some other tax forms, there is no provision for requesting an extension of time to file the W-3 form. It's crucial to meet the January 31st deadline to avoid penalties.

The information on the W-3 form is only used by the IRS. This isn’t true. The Social Security Administration (SSA) also uses the information on the W-3 form, in tandem with the W-2 forms, to ensure accurate Social Security and Medicare records for employees.

The IRS W-3 form, officially known as the "Transmittal of Wage and Tax Statements," is a critical document for employers in the process of reporting their employees' annual earnings and withholding taxes to the Social Security Administration (SSA). Here are seven key takeaways about filling out and using this form:

Employers need to understand these aspects of Form W-3 to comply with federal reporting requirements effectively and ensure accurate income reporting and tax withholding for their employees.

Fake Restraining Order Papers - Specifies exceptions where peaceful written contact through a lawyer for legal paperwork is allowed, ensuring necessary legal communications can continue.

Baseball Tryout Form - Enables the objective comparison of players by standardizing the assessment process during baseball tryouts.