Fill a Valid IRS W-9 Form

Fill a Valid IRS W-9 Form

Understanding the importance of the IRS W-9 form is crucial for both individuals and businesses engaging in various financial transactions in the United States. This simple yet significant document plays a key role in the tax reporting and withholding process, ensuring that the correct information is available for income verification and tax compliance purposes. The W-9 form is primarily used to gather details like the taxpayer identification number (TIN), which can be a social security number (SSN) or an employer identification number (EIN), from contractors, freelancers, and other entities paid for services. It's a way for businesses to collect the necessary information to issue 1099 forms, which report the income paid to individuals not employed by them, to the IRS. While the form may not be submitted directly to the IRS by the person who fills it out, the information it collects is essential for accurate tax reporting and reducing the likelihood of backup withholding—a process where the payee might need to withhold a percentage of income for tax purposes. Ensuring that the W-9 is filled out correctly and updated as necessary helps individuals and businesses stay compliant with tax regulations, avoid potential penalties, and streamline their financial operations.

Form |

Request for Taxpayer |

Give Form to the |

(Rev. October 2018) |

Identification Number and Certification |

requester. Do not |

Department of the Treasury |

▶ Go to www.irs.gov/FormW9 for instructions and the latest information. |

send to the IRS. |

Internal Revenue Service |

|

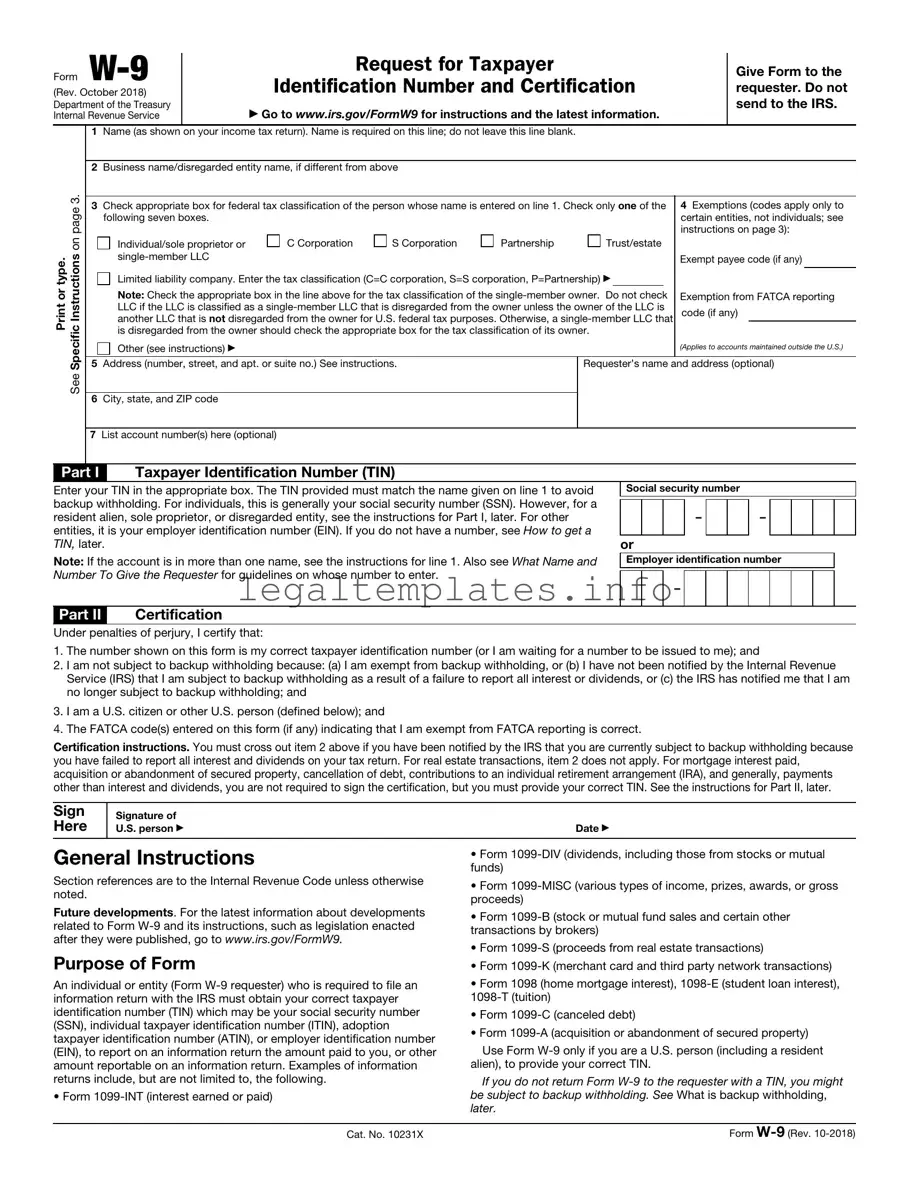

1Name (as shown on your income tax return). Name is required on this line; do not leave this line blank.

2Business name/disregarded entity name, if different from above

3. |

|

|

|

|

|

|

|

|

3 Check appropriate box for federal tax classification of the person whose name is entered on line 1. Check only one of the |

4 Exemptions (codes apply only to |

|||||||

page |

||||||||

following seven boxes. |

|

|

|

|

certain entities, not individuals; see |

|||

|

|

|

|

|

instructions on page 3): |

|||

on |

Individual/sole proprietor or |

C Corporation |

S Corporation |

Partnership |

Trust/estate |

|

|

|

Printor type. InstructionsSpecific |

|

|

|

|

Exempt payee code (if any) |

|||

5 Address (number, street, and apt. or suite no.) See instructions. |

|

Requester’s name |

|

|

||||

|

and address (optional) |

|||||||

|

Limited liability company. Enter the tax classification (C=C corporation, S=S corporation, P=Partnership) ▶ |

|

|

|||||

|

Note: Check the appropriate box in the line above for the tax classification of the |

Exemption from FATCA reporting |

||||||

|

LLC if the LLC is classified as a |

code (if any) |

||||||

|

another LLC that is not disregarded from the owner for U.S. federal tax purposes. Otherwise, a |

|

|

|||||

|

is disregarded from the owner should check the appropriate box for the tax classification of its owner. |

|

|

|||||

|

Other (see instructions) ▶ |

|

|

|

|

(Applies to accounts maintained outside the U.S.) |

||

See |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

6 City, state, and ZIP code |

|

|

|

|

|

|

|

7List account number(s) here (optional)

Part I Taxpayer Identification Number (TIN)

Enter your TIN in the appropriate box. The TIN provided must match the name given on line 1 to avoid backup withholding. For individuals, this is generally your social security number (SSN). However, for a resident alien, sole proprietor, or disregarded entity, see the instructions for Part I, later. For other entities, it is your employer identification number (EIN). If you do not have a number, see How to get a TIN, later.

Note: If the account is in more than one name, see the instructions for line 1. Also see What Name and Number To Give the Requester for guidelines on whose number to enter.

Part II Certification

Social security number

– |

|

|

– |

|

|

|

|

or

Employer identification number

–

Under penalties of perjury, I certify that:

1.The number shown on this form is my correct taxpayer identification number (or I am waiting for a number to be issued to me); and

2.I am not subject to backup withholding because: (a) I am exempt from backup withholding, or (b) I have not been notified by the Internal Revenue Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or (c) the IRS has notified me that I am no longer subject to backup withholding; and

3.I am a U.S. citizen or other U.S. person (defined below); and

4.The FATCA code(s) entered on this form (if any) indicating that I am exempt from FATCA reporting is correct.

Certification instructions. You must cross out item 2 above if you have been notified by the IRS that you are currently subject to backup withholding because you have failed to report all interest and dividends on your tax return. For real estate transactions, item 2 does not apply. For mortgage interest paid, acquisition or abandonment of secured property, cancellation of debt, contributions to an individual retirement arrangement (IRA), and generally, payments other than interest and dividends, you are not required to sign the certification, but you must provide your correct TIN. See the instructions for Part II, later.

Sign |

Signature of |

|

Here |

U.S. person ▶ |

Date ▶ |

General Instructions |

• Form |

|

|

||

Section references are to the Internal Revenue Code unless otherwise |

funds) |

|

• Form |

||

noted. |

||

proceeds) |

||

Future developments. For the latest information about developments |

||

• Form |

||

related to Form |

||

transactions by brokers) |

||

after they were published, go to www.irs.gov/FormW9. |

||

• Form |

||

Purpose of Form |

||

• Form |

||

An individual or entity (Form |

• Form 1098 (home mortgage interest), |

|

information return with the IRS must obtain your correct taxpayer |

||

identification number (TIN) which may be your social security number |

• Form |

|

(SSN), individual taxpayer identification number (ITIN), adoption |

• Form |

|

taxpayer identification number (ATIN), or employer identification number |

||

Use Form |

||

(EIN), to report on an information return the amount paid to you, or other |

||

amount reportable on an information return. Examples of information |

alien), to provide your correct TIN. |

|

returns include, but are not limited to, the following. |

If you do not return Form |

|

• Form |

be subject to backup withholding. See What is backup withholding, |

|

|

later. |

Cat. No. 10231X |

Form |

Form |

Page 2 |

By signing the

1.Certify that the TIN you are giving is correct (or you are waiting for a number to be issued),

2.Certify that you are not subject to backup withholding, or

3.Claim exemption from backup withholding if you are a U.S. exempt payee. If applicable, you are also certifying that as a U.S. person, your allocable share of any partnership income from a U.S. trade or business is not subject to the withholding tax on foreign partners' share of effectively connected income, and

4.Certify that FATCA code(s) entered on this form (if any) indicating that you are exempt from the FATCA reporting, is correct. See What is FATCA reporting, later, for further information.

Note: If you are a U.S. person and a requester gives you a form other than Form

Definition of a U.S. person. For federal tax purposes, you are considered a U.S. person if you are:

•An individual who is a U.S. citizen or U.S. resident alien;

•A partnership, corporation, company, or association created or organized in the United States or under the laws of the United States;

•An estate (other than a foreign estate); or

•A domestic trust (as defined in Regulations section

Special rules for partnerships. Partnerships that conduct a trade or business in the United States are generally required to pay a withholding tax under section 1446 on any foreign partners’ share of effectively connected taxable income from such business. Further, in certain cases where a Form

In the cases below, the following person must give Form

•In the case of a disregarded entity with a U.S. owner, the U.S. owner of the disregarded entity and not the entity;

•In the case of a grantor trust with a U.S. grantor or other U.S. owner, generally, the U.S. grantor or other U.S. owner of the grantor trust and not the trust; and

•In the case of a U.S. trust (other than a grantor trust), the U.S. trust (other than a grantor trust) and not the beneficiaries of the trust.

Foreign person. If you are a foreign person or the U.S. branch of a foreign bank that has elected to be treated as a U.S. person, do not use Form

Nonresident alien who becomes a resident alien. Generally, only a nonresident alien individual may use the terms of a tax treaty to reduce or eliminate U.S. tax on certain types of income. However, most tax treaties contain a provision known as a “saving clause.” Exceptions specified in the saving clause may permit an exemption from tax to continue for certain types of income even after the payee has otherwise become a U.S. resident alien for tax purposes.

If you are a U.S. resident alien who is relying on an exception contained in the saving clause of a tax treaty to claim an exemption from U.S. tax on certain types of income, you must attach a statement to Form

1.The treaty country. Generally, this must be the same treaty under which you claimed exemption from tax as a nonresident alien.

2.The treaty article addressing the income.

3.The article number (or location) in the tax treaty that contains the saving clause and its exceptions.

4.The type and amount of income that qualifies for the exemption from tax.

5.Sufficient facts to justify the exemption from tax under the terms of the treaty article.

Example. Article 20 of the

If you are a nonresident alien or a foreign entity, give the requester the appropriate completed Form

Backup Withholding

What is backup withholding? Persons making certain payments to you must under certain conditions withhold and pay to the IRS 24% of such payments. This is called “backup withholding.” Payments that may be subject to backup withholding include interest,

You will not be subject to backup withholding on payments you receive if you give the requester your correct TIN, make the proper certifications, and report all your taxable interest and dividends on your tax return.

Payments you receive will be subject to backup withholding if:

1.You do not furnish your TIN to the requester,

2.You do not certify your TIN when required (see the instructions for Part II for details),

3.The IRS tells the requester that you furnished an incorrect TIN,

4.The IRS tells you that you are subject to backup withholding

because you did not report all your interest and dividends on your tax return (for reportable interest and dividends only), or

5.You do not certify to the requester that you are not subject to backup withholding under 4 above (for reportable interest and dividend accounts opened after 1983 only).

Certain payees and payments are exempt from backup withholding. See Exempt payee code, later, and the separate Instructions for the Requester of Form

Also see Special rules for partnerships, earlier.

What is FATCA Reporting?

The Foreign Account Tax Compliance Act (FATCA) requires a participating foreign financial institution to report all United States account holders that are specified United States persons. Certain payees are exempt from FATCA reporting. See Exemption from FATCA reporting code, later, and the Instructions for the Requester of Form

Updating Your Information

You must provide updated information to any person to whom you claimed to be an exempt payee if you are no longer an exempt payee and anticipate receiving reportable payments in the future from this person. For example, you may need to provide updated information if you are a C corporation that elects to be an S corporation, or if you no longer are tax exempt. In addition, you must furnish a new Form

Penalties

Failure to furnish TIN. If you fail to furnish your correct TIN to a requester, you are subject to a penalty of $50 for each such failure unless your failure is due to reasonable cause and not to willful neglect.

Civil penalty for false information with respect to withholding. If you make a false statement with no reasonable basis that results in no backup withholding, you are subject to a $500 penalty.

Form |

Page 3 |

Criminal penalty for falsifying information. Willfully falsifying certifications or affirmations may subject you to criminal penalties including fines and/or imprisonment.

Misuse of TINs. If the requester discloses or uses TINs in violation of federal law, the requester may be subject to civil and criminal penalties.

Specific Instructions

Line 1

You must enter one of the following on this line; do not leave this line blank. The name should match the name on your tax return.

If this Form

a.Individual. Generally, enter the name shown on your tax return. If you have changed your last name without informing the Social Security Administration (SSA) of the name change, enter your first name, the last name as shown on your social security card, and your new last name.

Note: ITIN applicant: Enter your individual name as it was entered on your Form

b.Sole proprietor or

c.Partnership, LLC that is not a

d.Other entities. Enter your name as shown on required U.S. federal tax documents on line 1. This name should match the name shown on the charter or other legal document creating the entity. You may enter any business, trade, or DBA name on line 2.

e.Disregarded entity. For U.S. federal tax purposes, an entity that is disregarded as an entity separate from its owner is treated as a “disregarded entity.” See Regulations section

Line 2

If you have a business name, trade name, DBA name, or disregarded entity name, you may enter it on line 2.

Line 3

Check the appropriate box on line 3 for the U.S. federal tax classification of the person whose name is entered on line 1. Check only one box on line 3.

IF the entity/person on line 1 is |

THEN check the box for . . . |

|

a(n) . . . |

|

|

|

|

|

• |

Corporation |

Corporation |

• |

Individual |

Individual/sole proprietor or single- |

• |

Sole proprietorship, or |

member LLC |

• |

|

|

company (LLC) owned by an |

|

|

individual and disregarded for U.S. |

|

|

federal tax purposes. |

|

|

|

|

|

• |

LLC treated as a partnership for |

Limited liability company and enter |

U.S. federal tax purposes, |

the appropriate tax classification. |

|

• |

LLC that has filed Form 8832 or |

(P= Partnership; C= C corporation; |

2553 to be taxed as a corporation, |

or S= S corporation) |

|

or |

|

|

• |

LLC that is disregarded as an |

|

entity separate from its owner but |

|

|

the owner is another LLC that is |

|

|

not disregarded for U.S. federal tax |

|

|

purposes. |

|

|

|

|

|

• |

Partnership |

Partnership |

|

|

|

• |

Trust/estate |

Trust/estate |

|

|

|

Line 4, Exemptions

If you are exempt from backup withholding and/or FATCA reporting, enter in the appropriate space on line 4 any code(s) that may apply to you.

Exempt payee code.

•Generally, individuals (including sole proprietors) are not exempt from backup withholding.

•Except as provided below, corporations are exempt from backup withholding for certain payments, including interest and dividends.

•Corporations are not exempt from backup withholding for payments made in settlement of payment card or third party network transactions.

•Corporations are not exempt from backup withholding with respect to attorneys’ fees or gross proceeds paid to attorneys, and corporations that provide medical or health care services are not exempt with respect to payments reportable on Form

The following codes identify payees that are exempt from backup withholding. Enter the appropriate code in the space in line 4.

Form |

Page 4 |

The following chart shows types of payments that may be exempt from backup withholding. The chart applies to the exempt payees listed above, 1 through 13.

IF the payment is for . . . |

THEN the payment is exempt |

|

for . . . |

|

|

Interest and dividend payments |

All exempt payees except |

|

for 7 |

|

|

Broker transactions |

Exempt payees 1 through 4 and 6 |

|

through 11 and all C corporations. |

|

S corporations must not enter an |

|

exempt payee code because they |

|

are exempt only for sales of |

|

noncovered securities acquired |

|

prior to 2012. |

|

|

Barter exchange transactions and |

Exempt payees 1 through 4 |

patronage dividends |

|

|

|

Payments over $600 required to be |

Generally, exempt payees |

reported and direct sales over |

1 through 52 |

$5,0001 |

|

|

|

Payments made in settlement of |

Exempt payees 1 through 4 |

payment card or third party network |

|

transactions |

|

|

|

1See Form

2However, the following payments made to a corporation and reportable on Form

Exemption from FATCA reporting code. The following codes identify payees that are exempt from reporting under FATCA. These codes apply to persons submitting this form for accounts maintained outside of the United States by certain foreign financial institutions. Therefore, if you are only submitting this form for an account you hold in the United States, you may leave this field blank. Consult with the person requesting this form if you are uncertain if the financial institution is subject to these requirements. A requester may indicate that a code is not required by providing you with a Form

Note: You may wish to consult with the financial institution requesting this form to determine whether the FATCA code and/or exempt payee code should be completed.

Line 5

Enter your address (number, street, and apartment or suite number). This is where the requester of this Form

Line 6

Enter your city, state, and ZIP code.

Part I. Taxpayer Identification Number (TIN)

Enter your TIN in the appropriate box. If you are a resident alien and you do not have and are not eligible to get an SSN, your TIN is your IRS individual taxpayer identification number (ITIN). Enter it in the social security number box. If you do not have an ITIN, see How to get a TIN below.

If you are a sole proprietor and you have an EIN, you may enter either your SSN or EIN.

If you are a

Note: See What Name and Number To Give the Requester, later, for further clarification of name and TIN combinations.

How to get a TIN. If you do not have a TIN, apply for one immediately. To apply for an SSN, get Form

If you are asked to complete Form

Note: Entering “Applied For” means that you have already applied for a TIN or that you intend to apply for one soon.

Caution: A disregarded U.S. entity that has a foreign owner must use the appropriate Form

Part II. Certification

To establish to the withholding agent that you are a U.S. person, or resident alien, sign Form

For a joint account, only the person whose TIN is shown in Part I should sign (when required). In the case of a disregarded entity, the person identified on line 1 must sign. Exempt payees, see Exempt payee code, earlier.

Signature requirements. Complete the certification as indicated in items 1 through 5 below.

Form |

Page 5 |

1.Interest, dividend, and barter exchange accounts opened before 1984 and broker accounts considered active during 1983. You must give your correct TIN, but you do not have to sign the certification.

2.Interest, dividend, broker, and barter exchange accounts opened after 1983 and broker accounts considered inactive during 1983. You must sign the certification or backup withholding will apply. If you are subject to backup withholding and you are merely providing your correct TIN to the requester, you must cross out item 2 in the certification before signing the form.

3.Real estate transactions. You must sign the certification. You may cross out item 2 of the certification.

4.Other payments. You must give your correct TIN, but you do not have to sign the certification unless you have been notified that you have previously given an incorrect TIN. “Other payments” include payments made in the course of the requester’s trade or business for rents, royalties, goods (other than bills for merchandise), medical and health care services (including payments to corporations), payments to a nonemployee for services, payments made in settlement of payment card and third party network transactions, payments to certain fishing boat crew members and fishermen, and gross proceeds paid to attorneys (including payments to corporations).

5.Mortgage interest paid by you, acquisition or abandonment of secured property, cancellation of debt, qualified tuition program payments (under section 529), ABLE accounts (under section 529A), IRA, Coverdell ESA, Archer MSA or HSA contributions or distributions, and pension distributions. You must give your correct TIN, but you do not have to sign the certification.

What Name and Number To Give the Requester

|

For this type of account: |

Give name and SSN of: |

|

|

|

1. |

Individual |

The individual |

2. |

Two or more individuals (joint |

The actual owner of the account or, if |

|

account) other than an account |

combined funds, the first individual on |

|

maintained by an FFI |

the account1 |

3. |

Two or more U.S. persons |

Each holder of the account |

|

(joint account maintained by an FFI) |

|

4. |

Custodial account of a minor |

The minor2 |

|

(Uniform Gift to Minors Act) |

|

5. a. The usual revocable savings trust |

The |

|

|

(grantor is also trustee) |

The actual owner1 |

|

b. |

|

|

a legal or valid trust under state law |

|

6. |

Sole proprietorship or disregarded |

The owner3 |

|

entity owned by an individual |

|

7. |

Grantor trust filing under Optional |

The grantor* |

|

Form 1099 Filing Method 1 (see |

|

|

Regulations section |

|

|

(A)) |

|

|

|

|

|

For this type of account: |

Give name and EIN of: |

|

|

|

8. |

Disregarded entity not owned by an |

The owner |

|

individual |

|

9. |

A valid trust, estate, or pension trust |

Legal entity4 |

10. |

Corporation or LLC electing |

The corporation |

|

corporate status on Form 8832 or |

|

|

Form 2553 |

|

11. |

Association, club, religious, |

The organization |

|

charitable, educational, or other tax- |

|

|

exempt organization |

|

12. |

Partnership or |

The partnership |

13. |

A broker or registered nominee |

The broker or nominee |

|

|

|

For this type of account: |

Give name and EIN of: |

|

|

14. Account with the Department of |

The public entity |

Agriculture in the name of a public |

|

entity (such as a state or local |

|

government, school district, or |

|

prison) that receives agricultural |

|

program payments |

|

15. Grantor trust filing under the Form |

The trust |

1041 Filing Method or the Optional |

|

Form 1099 Filing Method 2 (see |

|

Regulations section |

|

|

|

1List first and circle the name of the person whose number you furnish. If only one person on a joint account has an SSN, that person’s number must be furnished.

2Circle the minor’s name and furnish the minor’s SSN.

3You must show your individual name and you may also enter your business or DBA name on the “Business name/disregarded entity” name line. You may use either your SSN or EIN (if you have one), but the IRS encourages you to use your SSN.

4List first and circle the name of the trust, estate, or pension trust. (Do not furnish the TIN of the personal representative or trustee unless the legal entity itself is not designated in the account title.) Also see Special rules for partnerships, earlier.

*Note: The grantor also must provide a Form

Note: If no name is circled when more than one name is listed, the number will be considered to be that of the first name listed.

Secure Your Tax Records From Identity Theft

Identity theft occurs when someone uses your personal information such as your name, SSN, or other identifying information, without your permission, to commit fraud or other crimes. An identity thief may use your SSN to get a job or may file a tax return using your SSN to receive a refund.

To reduce your risk:

•Protect your SSN,

•Ensure your employer is protecting your SSN, and

•Be careful when choosing a tax preparer.

If your tax records are affected by identity theft and you receive a notice from the IRS, respond right away to the name and phone number printed on the IRS notice or letter.

If your tax records are not currently affected by identity theft but you think you are at risk due to a lost or stolen purse or wallet, questionable credit card activity or credit report, contact the IRS Identity Theft Hotline at

For more information, see Pub. 5027, Identity Theft Information for Taxpayers.

Victims of identity theft who are experiencing economic harm or a systemic problem, or are seeking help in resolving tax problems that have not been resolved through normal channels, may be eligible for Taxpayer Advocate Service (TAS) assistance. You can reach TAS by calling the TAS

Protect yourself from suspicious emails or phishing schemes. Phishing is the creation and use of email and websites designed to mimic legitimate business emails and websites. The most common act is sending an email to a user falsely claiming to be an established legitimate enterprise in an attempt to scam the user into surrendering private information that will be used for identity theft.

Form |

Page 6 |

The IRS does not initiate contacts with taxpayers via emails. Also, the IRS does not request personal detailed information through email or ask taxpayers for the PIN numbers, passwords, or similar secret access information for their credit card, bank, or other financial accounts.

If you receive an unsolicited email claiming to be from the IRS, forward this message to phishing@irs.gov. You may also report misuse of the IRS name, logo, or other IRS property to the Treasury Inspector General for Tax Administration (TIGTA) at

Visit www.irs.gov/IdentityTheft to learn more about identity theft and how to reduce your risk.

Privacy Act Notice

Section 6109 of the Internal Revenue Code requires you to provide your correct TIN to persons (including federal agencies) who are required to file information returns with the IRS to report interest, dividends, or certain other income paid to you; mortgage interest you paid; the acquisition or abandonment of secured property; the cancellation of debt; or contributions you made to an IRA, Archer MSA, or HSA. The person collecting this form uses the information on the form to file information returns with the IRS, reporting the above information. Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their laws. The information also may be disclosed to other countries under a treaty, to federal and state agencies to enforce civil and criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism. You must provide your TIN whether or not you are required to file a tax return. Under section 3406, payers must generally withhold a percentage of taxable interest, dividend, and certain other payments to a payee who does not give a TIN to the payer. Certain penalties may also apply for providing false or fraudulent information.

| Fact | Description |

|---|---|

| Purpose of Form W-9 | Used to provide a correct Taxpayer Identification Number (TIN) to the person who is required to file an information return with the IRS. |

| Entities Requesting W-9 | Typically, it is requested by businesses or individuals who make payments to freelancers, independent contractors, or other non-employees. |

| Primary Use | Essential for reporting income paid to contractors, interest income, real estate transactions, mortgage interest paid, acquisition or abandonment of secured property, cancellation of debt, and contributions made to an IRA. |

| Consequences of Not Filing | Failure to provide a Form W-9 when requested may lead to backup withholding, where the payer must withhold tax from your payments at a prescribed rate. |

| State-Specific Forms | While Form W-9 is a federal form, some states may have similar requirements for state tax purposes, governed by each state's department of revenue or taxation. |

Filling out the IRS W-9 form is a straightforward process, but it's crucial to get it right. This document is often requested by companies or individuals who plan to pay you, ensuring they gather the correct information to report payments to the IRS. Whether you're a freelancer, an independent contractor, or providing services that result in payment, you'll likely need to complete this form at some point. By following the steps below, you can ensure your W-9 is accurately filled out and submitted properly.

Once you've completed these steps, your W-9 is ready to be submitted to the requester. It's important to handle this form with care, as it contains sensitive information. Never send this form or any other sensitive documents via email unless it's encrypted or a secure transfer method is used. Keeping a copy for your records is also a good practice. By ensuring your W-9 is filled out accurately, you're taking an important step in managing your tax obligations and avoiding potential issues down the line.

What is a W-9 form?

A W-9 form, officially titled "Request for Taxpayer Identification Number and Certification," is a form used in the United States. Individuals and entities use it to provide their correct taxpayer identification number (TIN) to the person who is required to file an information return with the IRS. Information returns report income, real estate transactions, mortgage interest payments, acquisition or abandonment of secured property, cancellation of debt, contributions made to an IRA, and more.

Who needs to fill out a W-9 form?

Any individual or entity that needs to provide their taxpayer identification information to another person or entity, usually in the context of freelance work, independent contracting, or other non-employee work relationships, must fill out a W-9 form. This includes contractors, consultants, and vendors. It's also used by financial institutions to obtain identifying information from their customers.

Why do companies request a W-9 form?

Companies request a W-9 form to gather necessary information to prepare information returns, which they must file with the IRS. This includes reporting payments made to non-employees and other financial transactions. It ensures that they have the correct taxpayer identification number (TIN) and other details to accurately report financial activity as required by law.

What information do I need to provide on a W-9 form?

On a W-9 form, you are required to provide your name as shown on your tax return, your business name if different from your personal name, your tax classification (e.g., individual/sole proprietor, corporation, partnership), your taxpayer identification number (TIN) which may be your social security number (SSN) or employer identification number (EIN), and your address. You must also sign and date the form, certifying that the information is correct.

Is there a deadline to submit the W-9 form?

There is no official deadline for submitting a W-9 form to the requestor; however, it is typically required at the beginning of a business relationship or prior to receiving the first payment for services or goods provided. Failing to provide a completed W-9 when requested can lead to backup withholding, where the payer must withhold tax from your payments at the current rate set by the IRS.

What is backup withholding?

Backup withholding is a form of tax withholding on income for those who either fail to provide their TIN (taxpayer identification number) or do not report all their income. The IRS sets the withholding rate, and it's applied to certain payments when the necessary conditions are not met. It acts as an incentive for taxpayers to supply correct information to payees.

Can I refuse to fill out a W-9 form?

Refusing to fill out a W-9 form can result in backup withholding of payments for goods and services at the IRS mandated rate. The form is a legal requirement to verify your tax identification number and certify your tax status, so failure to comply can also affect your business relationships and lead to potential penalties from the IRS.

Is it safe to email a completed W-9 form?

Emailing sensitive documents, including those with your taxpayer identification number, can pose a risk of interception by unauthorized parties. It's important to ensure that the recipient's email is secure or to use encrypted email services. Whenever possible, consider using secure file transfer methods provided by the requesting party or encrypted methods of transmission.

How long should I keep copies of filled-out W-9 forms?

While the IRS does not specify a required retention period for W-9 forms, it's a good practice to keep them for at least three years after the end of the tax year in which you last used the information from the form. This period aligns with the IRS's statute of limitations for auditing tax returns. However, consulting with a tax professional for personalized advice is recommended.

What should I do if my information changes after I've submitted a W-9 form?

If your information, such as your name, address, or taxpayer identification number, changes after you've submitted a W-9 form, you should complete a new form with the updated information and provide it to all parties you initially gave the old form to. This ensures that they have your most current information for IRS reporting purposes.

One common mistake that people make when filling out the IRS W-9 form is not using their correct legal name. This name should match the one on your social security card or other government-issued identification. If there is a discrepancy between the name provided on the W-9 and the taxpayer identification number (TIN), it could lead to issues with the IRS, such as delayed refunds or unprocessed documents.

Another error often encountered is incorrectly inputting the Taxpayer Identification Number (TIN), which is typically a Social Security Number (SSN) for individuals. Some might mistakenly transpose numbers or inaccurately record their Employer Identification Number (EIN) if they are representing an entity like a trust, estate, or corporation. Ensuring this number is accurately reflected is critical as it ties all financial transactions taxed under this number directly to the taxpayer.

Individuals also frequently overlook the importance of selecting the correct tax classification on the W-9 form. This selection determines how the business will be taxed and can affect the nature of the tax documents received in the following year. For instance, a limited liability company (LLC) has to specify its tax classification based on its structure. Incorrect classification can lead to improper reporting and potentially higher taxes or penalties.

Not signing the form is a simpler yet equally significant error. A W-9 form without a signature may not be considered valid. The signature attests that the information provided is accurate and true to the best of the taxpayer's knowledge. Unsigned forms can result in the form being returned for correction, causing delays in what might be time-sensitive financial processes.

Finally, people sometimes fail to update their W-9 form when their circumstances change, such as a name change due to marriage or divorce, or a change in business structure. Not having up-to-date information on file can lead to misfiled taxes or the IRS not being able to match the information to the correct taxpayer. Regularly updating the form ensures that all information remains current and accurate.

The IRS W-9 form is a pivotal document utilized primarily for tax identification and the certification of a person's tax ID number, typically requested by companies or individuals who are required to report payments made to freelancers, contractors, and other non-employees to the Internal Revenue Service (IRS). While the W-9 is a cornerstone in tax documentation, especially within the freelance and contract-based workforce, there are several other forms and documents frequently used in conjunction with it, each serving its unique role in the broader landscape of tax documentation and compliance.

In navigating the complexities of tax documentation and compliance, understanding the interplay between the IRS W-9 form and these additional forms and documents is crucial. Each document serves a specific purpose, from reporting income and tax liabilities to requesting tax return transcripts or applying for an EIN. By familiarizing oneself with these documents, individuals and businesses can ensure they meet their tax obligations, thereby avoiding potential penalties and ensuring a smoother interaction with tax authorities.

The IRS W-9 form, Request for Taxpayer Identification Number and Certification, shares similarities with the W-4 form, Employee's Withholding Certificate. Both forms are used by the IRS to ensure accurate tax withholding and reporting. However, while the W-9 is utilized by freelancers and independent contractors to provide their taxpayer information to entities that pay them, the W-4 is used by employees to inform their employers of their withholding allowances and personal information to calculate tax withholdings from their paychecks.

Similar to the IRS W-9 form, the 1099 form series is used for reporting income other than wages, salaries, and tips. The W-9 form provides the payer the necessary taxpayer identification number (TIN) and certification to accurately file information returns with the IRS, using forms in the 1099 series, for transactions such as freelance earnings, interest, dividends, and non-employee compensation.

The W-8BEN form, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals), parallels the W-9 form in its role of collecting tax information, but it is specifically used by non-U.S. persons. Where the W-9 form is used by U.S. persons (both citizens and resident aliens) to certify their tax ID numbers, the W-8BEN form is for non-U.S. individuals to certify their foreign status and claim any applicable benefits under the tax treaty.

The IRS Form 1040, U.S. Individual Tax Return, is the primary form used by individuals to file their annual income tax returns, which differs in purpose from the W-9's use in business and freelancing settings for tax information gathering. However, the information collected through the W-9 can directly impact the accuracy and completeness of an individual's 1040 form, particularly in reporting freelance or independent contractor income.

The SS-4 form, Application for Employer Identification Number (EIN), is used to apply for an EIN; this number is necessary for tax reporting for entities rather than individuals. While the W-9 form collects taxpayer identification information for individuals and entities, the SS-4 is the avenue through which businesses can obtain their unique nine-digit EIN necessary for tax filings, employee payroll, and opening business bank accounts.

Another document similar to the IRS W-9 form is the W-8ECI, Certificate of Foreign Person's Claim That Income Is Effectively Connected With the Conduct of a Trade or Business in the United States. Like the W-9, it's part of the tax documentation process but is specifically for foreign persons or entities claiming that their income is connected with a U.S. business and, thus, subject to withholding. The W-9, alternatively, is used domestically for essentially the same purpose: to declare tax status and ensure appropriate tax withholding and reporting.

The IRS W-9 form is a crucial document for reporting income paid to freelancers, independent contractors, and other non-employees. Ensuring accuracy and thoroughness when completing this form is of paramount importance. Below are lists of dos and don'ts to guide you through this process.

Do:

Don't:

Many individuals and businesses often misunderstand the IRS W-9 form, leading to common errors and misconceptions. It's crucial to have accurate information to comply with tax laws and maintain smooth financial operations. Here are five frequent misconceptions about the IRS W-9 form.

Only employees need to fill it out: A common misconception is that W-9 forms are only for employees. In reality, they are used by freelancers, independent contractors, and other non-employees. Businesses use the information to report income paid to non-employees through a 1099 form.

Submitting a W-9 means taxes are withheld: Filling out a W-9 does not result in automatic tax withholding. This form simply provides the payer with the necessary information, like the taxpayer identification number (TIN), to report income paid. It's the responsibility of the individual or entity filling the form to handle their taxes.

The information on a W-9 doesn't need to be updated: Actually, it's crucial to submit a new W-9 form if your name, business name, address, or TIN changes. Keeping this information current helps avoid potential issues, such as backup withholding or not receiving important tax documents.

W-9 forms are submitted to the IRS: This is another common mistake. W-9 forms are provided to the person or business that pays you, not the IRS. The payer uses the information to complete the necessary 1099 form for tax reporting purposes.

Electronic signatures are not allowed on W-9 forms: The IRS does permit electronic signatures on W-9 forms. This flexibility supports efficient operations, especially in today's digital age, allowing businesses and individuals to process these forms quickly and securely.

The IRS W-9 form, titled "Request for Taxpayer Identification Number and Certification," is a crucial document used primarily for tax reporting purposes in the United States. It plays a significant role in ensuring the accuracy of financial records and the fulfillment of tax obligations. Below are key takeaways regarding the filling out and utilization of the IRS W-9 form:

Understanding these key aspects of the W-9 form can greatly facilitate compliance with U.S. tax laws, both for individuals and for businesses engaging with independent contractors. Properly managing and retaining these forms is essential for fulfilling tax reporting requirements and avoiding potential penalties.

Free Horse Training Contract Template - It serves as the entire agreement between the owner and trainer, superseding any prior discussions with its comprehensive and specific terms.

I983 Form Instructions - The form is designed to reflect changes in the training plan, should they occur, ensuring the program remains relevant and beneficial.

Notarized Letter of Consent - It's designed to give peace of mind to parents, ensuring their children are in trusted hands while aboard.