Fill a Valid Loan Estimate Form

Fill a Valid Loan Estimate Form

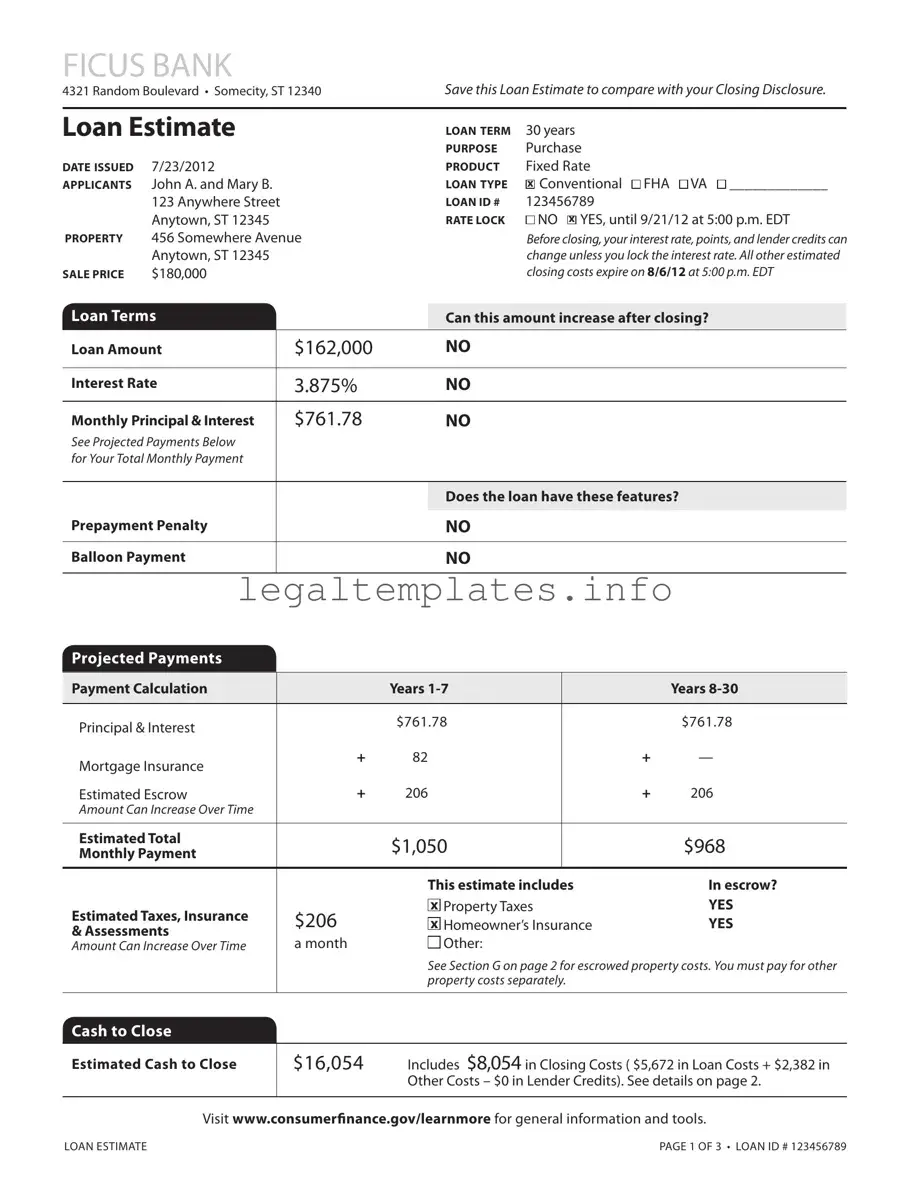

The Loan Estimate form, a critical first step for borrowers in understanding their mortgage options, encapsulates key loan details and estimated closing costs in a straightforward format. Issued by Ficus Bank, it breaks down the terms of the loan, including the interest rate, monthly payments, and whether these may change after closing. Dated 7/23/2012, with a 30-year term for a purchase on a fixed rate, it's clear this document is designed to protect applicants John A. and Mary B. by ensuring they have all pertinent information before moving forward. The form meticulously outlines costs associated with the loan, like origination charges and services you cannot shop for, alongside other government fees, prepaids, escrow payments at closing, and total estimated cash to close. It also offers a comparison section to aid borrowers in evaluating how this loan stacks up against others over a five-year period, including the APR and total interest percentage, providing a comprehensive overview of the financial commitment involved. Furthermore, the form covers additional information related to appraisals, assumptions, and homeowner’s insurance requirements, culminating in a detailed snapshot that supports informed decision-making for prospective homeowners.

FICUS BANK

4321 Random Boulevard • Somecity, ST 12340Save this Loan Estimate to compare with your Closing Disclosure.

Loan estimate |

LOAN TeRM |

30 years |

|

|

|

PuRPOse |

Purchase |

DATe IssueD |

7/23/2012 |

PRODuCT |

Fixed Rate |

APPLICANTs |

John A. and Mary B. |

LOAN TyPe |

x Conventional FHA VA _____________ |

|

123 Anywhere Street |

LOAN ID # |

123456789 |

|

Anytown, ST 12345 |

RATe LOCK |

NO x YES, until 9/21/12 at 5:00 p.m. EDT |

PROPeRTy |

456 Somewhere Avenue |

|

Before closing, your interest rate, points, and lender credits can |

|

Anytown, ST 12345 |

|

change unless you lock the interest rate. All other estimated |

sALe PRICe |

$180,000 |

|

closing costs expire on 8/6/12 at 5:00 p.m. EDT |

Loan Terms |

|

Can this amount increase after closing? |

Loan Amount |

$162,000 |

NO |

|

|

|

Interest Rate |

3.875% |

NO |

|

|

|

Monthly Principal & Interest |

$761.78 |

NO |

See Projected Payments Below |

|

|

for Your Total Monthly Payment |

|

|

|

|

|

|

|

Does the loan have these features? |

Prepayment Penalty |

|

|

|

NO |

|

|

|

|

Balloon Payment |

|

NO |

|

|

|

Projected Payments

Payment Calculation |

|

years |

|

|

years |

|

|

|

|

|

|

Principal & Interest |

|

$761.78 |

|

|

$761.78 |

|

|

|

|

|

|

Mortgage Insurance |

+ |

82 |

|

+ |

— |

|

|

|

|

|

|

Estimated Escrow |

+ |

206 |

|

+ |

206 |

Amount Can Increase Over Time |

|

|

|

|

|

|

|

|

|

|

|

estimated Total |

|

$1,050 |

|

|

$968 |

Monthly Payment |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This estimate includes |

|

In escrow? |

|

estimated Taxes, Insurance |

$206 |

x Property Taxes |

|

yes |

|

x Homeowner’s Insurance |

|

yes |

|||

& Assessments |

|

||||

a month |

Other: |

|

|

||

Amount Can Increase Over Time |

|

|

|||

|

|

See Section G on page 2 for escrowed property costs. You must pay for other |

|||

|

|

property costs separately. |

|

|

|

|

|

|

|

|

|

Cash to Close |

|

|

|

|

|

|

|

|

|

||

estimated Cash to Close |

$16,054 |

Includes $8,054 in Closing Costs ( $5,672 in Loan Costs + $2,382 in |

|||

|

|

Other Costs – $0 in Lender Credits). See details on page 2. |

|||

|

|

|

|

|

|

Visit www.consumerinance.gov/learnmore for general information and tools.

LOAN ESTIMATE |

page 1 of 3 • Loan ID # 123456789 |

Closing Cost Details

Loan Costs

A. Origination Charges |

$1,802 |

.25 % of Loan Amount (Points) |

$405 |

Application Fee |

$300 |

Underwriting Fee |

$1,097 |

Other Costs

e. Taxes and Other Government Fees |

$85 |

||||||

Recording Fees and Other Taxes |

|

|

$85 |

||||

Transfer Taxes |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

F. Prepaids |

|

|

$867 |

||||

Homeowner’s Insurance Premium ( |

6 months) |

$605 |

|||||

|

|

|

|

|

|

|

|

Mortgage Insurance Premium ( 0 |

months) |

$0 |

|||||

|

|

|

|

|

|

||

Prepaid Interest ( $17.44 per day for 15 days @ 3.875%) |

$262 |

||||||

Property Taxes ( 0 months) |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

B. services you Cannot shop For |

$672 |

Appraisal Fee |

$405 |

Credit Report Fee |

$30 |

Flood Determination Fee |

$20 |

Flood Monitoring Fee |

$32 |

Tax Monitoring Fee |

$75 |

Tax Status Research Fee |

$110 |

G. Initial escrow Payment at Closing |

|

|

$413 |

|

Homeowner’s Insurance |

$100.83 per month for |

23mo. $202 |

||

Mortgage Insurance |

per month for |

0 |

mo. |

|

Property Taxes |

$105.30 per month for |

2 |

mo. |

$211 |

H. Other |

$1,017 |

Title – Owner’s Title Policy (optional) |

$1,017 |

C. services you Can shop For |

$3,198 |

Pest Inspection Fee |

$135 |

Survey Fee |

$65 |

Title – Insurance Binder |

$700 |

Title – Lender’s Title Policy |

$535 |

Title – Title Search |

$1,261 |

Title – Settlement Agent Fee |

$502 |

D. TOTAL LOAN COsTs (A + B + C) |

$5,672 |

I. TOTAL OTHeR COsTs (e + F + G + H) |

$2,382 |

|

|

J. TOTAL CLOsING COsTs |

$8,054 |

|

|

D + I |

$8,054 |

Lender Credits |

$0 |

Calculating Cash to Close |

|

|

|

Total Closing Costs (J) |

$8,054 |

Closing Costs Financed (Included in Loan Amount) |

$0 |

Down Payment/Funds from Borrower |

$18,000 |

Deposit |

– $10,000 |

Funds for Borrower |

$0 |

Seller Credits |

$0 |

Adjustments and Other Credits |

$0 |

estimated Cash to Close |

$16,054 |

|

|

LOAN ESTIMATE |

page 2 of 3 • Loan ID # 123456789 |

Additional Information About This Loan

LeNDeR NMLs/LICeNse ID

LOAN OFFICeR

NMLs ID

PHONe

Ficus Bank

Joe Smith 12345 joesmith@icusbank.com

MORTGAGe BROKeR NMLs/LICeNse ID LOAN OFFICeR NMLs ID

eMAIL PHONe

Comparisons |

use these measures to compare this loan with other loans. |

||

|

|

|

|

In 5 years |

$56,582 |

Total you will have paid in principal, interest, mortgage insurance, and loan costs. |

|

$15,773 |

Principal you will have paid of. |

||

|

|||

|

|

|

|

Annual Percentage Rate (APR) |

4.494% |

Your costs over the loan term expressed as a rate. This is not your interest rate. |

|

|

|

|

|

Total Interest Percentage (TIP) |

69.447% |

The total amount of interest that you will pay over the loan term as a |

|

|

|

percentage of your loan amount. |

|

|

|

|

|

Other Considerations

Appraisal |

We may order an appraisal to determine the property’s value and charge you for this |

|

appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. |

|

You can pay for an additional appraisal for your own use at your own cost. |

Assumption |

If you sell or transfer this property to another person, we |

|

will allow, under certain conditions, this person to assume this loan on the original terms. |

|

x will not allow this person to assume this loan on the original terms. |

Homeowner’s |

This loan requires homeowner’s insurance on the property, which you may obtain from a |

Insurance |

company of your choice that we ind acceptable. |

Late Payment |

If your payment is more than 15 days late, we will charge a late fee of 5% of the monthly |

|

principal and interest payment. |

Reinance |

Reinancing this loan will depend on your future inancial situation, the property value, and |

|

market conditions. You may not be able to reinance this loan. |

servicing |

We intend |

|

to service your loan. If so, you will make your payments to us. |

|

x to transfer servicing of your loan. |

Conirm Receipt

By signing, you are only conirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature |

Date |

Date |

LOAN ESTIMATE |

page 3 of 3 • Loan ID #123456789 |

| Fact | Description |

|---|---|

| 1. Document Type | Loan Estimate |

| 2. Purpose | Provides a summary of the key loan terms, projected payments, costs of getting a mortgage, and other considerations of the loan. |

| 3. Issuer | Ficus Bank |

| 4. Loan Type Options | Conventional, FHA, VA |

| 5. Rate Lock Feature | Indicates whether the interest rate is locked and its expiration date and time. |

| 6. Projected Payments and Loan Costs | Breaks down the monthly payment, estimated taxes, insurance, and assessments, including a detailed list of loan costs and other costs. |

| 7. Cash to Close | Provides an estimate of the total amount of cash needed to close the mortgage. |

| 8. Governing Law | Federal (No specific state law mentioned since the Loan Estimate form is standardized under the TRID rule by the Consumer Financial Protection Bureau). |

Filling out the Loan Estimate form is a crucial step in understanding the details of your mortgage offer. It breaks down the terms, rates, and fees associated with your proposed loan, providing a clear picture of the financial commitment you are about to make. Accuracy and thoroughness are key to ensuring that you have a reliable document to compare with your Closing Disclosure.

After completing these steps, carefully review the entire document for any inconsistencies or errors. This document not only helps in comparing with your Closing Disclosure but also ensures you are fully informed about the specifics of your loan before closing.

What is a Loan Estimate?

The Loan Estimate is a three-page form that you receive after applying for a mortgage. It provides important details about the loan you've applied for, including the estimated interest rate, monthly payment, and total closing costs for the loan. It also outlines the loan terms and features that may impact your finances over time, such as prepayment penalties or balloon payments. The form is designed to help you understand and compare different loan offers.

Why is the Loan Estimate important?

This document is crucial because it gives prospective borrowers a clear and standardized way to compare mortgage offers and understand the terms and costs of their loan before they commit. Receiving this estimate allows you to ask lenders questions about your loan and negotiate better terms if possible. It's an essential tool in making an informed decision about which mortgage option is best for your situation.

When should I receive a Loan Estimate?

Under federal law, you must receive a Loan Estimate within three business days of submitting your mortgage application. This timeline ensures that you have the information early enough in the home-buying process to review and compare loan offers. If there are significant changes to your loan terms during the process, you may receive revised loan estimates.

What should I look for on my Loan Estimate?

There are several key sections to pay attention to: The loan terms, projected monthly payments, and costs at closing. Ensure that the interest rate and loan type (e.g., fixed-rate) match what you discussed with the lender. Review the "Projected Payments" section to understand how your payment could change over time. Finally, examine the "Costs at Closing" to see the estimated cash needed to close and the total closing costs.

Can the costs on the Loan Estimate change before closing?

Yes, some costs on the Loan Estimate can change before closing. However, certain fees are not allowed to increase, such as the lender's origination charge, while others can change within legal limits. For example, costs for third-party services where the lender allows you to choose the provider may increase. The interest rate can also change unless it is locked in. It's essential to ask your lender which costs are fixed and which can change.

What happens after I get a Loan Estimate?

Once you receive your Loan Estimate, review it carefully to ensure it aligns with what you discussed with your lender and that you understand all the terms and costs involved. From there, you can choose to proceed with the application with that lender, shop around and compare offers from other lenders, or negotiate the terms and costs outlined in the estimate. Remember, receiving a Loan Estimate does not obligate you to proceed with the loan; it's a tool to help you make informed decisions.

One common mistake made when filling out the Loan Estimate form is incorrectly identifying the loan type. This is a crucial detail as it affects terms and conditions, such as whether the loan is a Conventional, FHA, or VA loan. Incorrectly marking this section can lead to misunderstandings regarding interest rates, down payments, and insurance requirements.

Another error often encountered is the failure to accurately note the interest rate lock. If the box indicating the interest rate is locked is mistakenly marked "No" when it should be "Yes" (or vice versa), it may result in unexpected changes to the interest rate. This detail directly impacts the monthly payment amount and the overall cost of the loan.

Additionally, overlooking the expiration of the estimated closing costs is a frequent oversight. This part of the form communicates until when the estimated closing costs are valid. Missing this information can lead to surprises in closing costs if the closing date is delayed or extended past this period.

Incorrect entries in the "Cash to Close" section also occur frequently. This includes inaccuracies in down payment amounts, closing costs, and lender credits. Such mistakes can significantly affect the final amount the borrower needs to bring to closing, potentially causing delays or financial strain.

Last but not least, there's the confusion around the "Projected Payments" section, where borrowers sometimes misinterpret the breakdown of principal, interest, mortgage insurance, and estimated escrow. Misunderstanding how these components change over time can lead to incorrect assumptions about the long-term affordability of the loan.

When obtaining a mortgage, several forms and documents accompany the Loan Estimate form, creating a comprehensive package necessary for processing the loan application. These documents play integral roles, from providing detailed information about the property and borrower's financial status to outlining the terms and conditions of the loan. Below is a brief description of other common forms and documents used alongside the Loan Estimate.

Together with the Loan Estimate, these documents ensure that both borrower and lender have a clear, comprehensive understanding of the loan terms, property details, and financial arrangements. Ensuring accuracy and completeness of these documents is vital for a successful mortgage application process.

The Good Faith Estimate (GFE) form is closely related to the Loan Estimate form, as both serve the purpose of providing borrowers with a detailed breakdown of estimated closing costs and loan terms. The GFE, however, was the standard form before the Loan Estimate was introduced under the TILA-RESPA Integrated Disclosure (TRID) rules. Though no longer in use, it offered a similar initial overview of mortgage charges, aiming to facilitate comparison shopping among lenders.

The Closing Disclosure form shares significant similarities with the Loan Estimate, primarily in content and purpose, but is provided closer to the closing of the mortgage transaction. While the Loan Estimate gives an early estimate of loan terms and costs, the Closing Disclosure confirms the final costs, terms, and other critical details about the mortgage. This document is crucial for borrowers to review before the finalization of the loan, allowing them to verify that the terms have not changed unfavorably.

The HUD-1 Settlement Statement, though replaced by the Closing Disclosure form for most residential real estate transactions, used to serve a similar function by itemizing all charges imposed upon borrowers and sellers in connection with the settlement. The HUD-1 was primarily used in transactions not covered by the TRID rules, such as reverse mortgages or mortgages secured by mobile homes or dwellings not attached to real estate.

The Truth in Lending Act (TILA) disclosure is designed to inform borrowers of the costs and terms of credit, providing details like the annual percentage rate (APR), finance charge, amount financed, and total of payments. Although it shares the common goal of borrower enlightenment with the Loan Estimate, the TILA disclosure focuses more on the finance charges and APR rather than itemized closing costs.

The Mortgage Servicing Disclosure Statement outlines the servicer’s policy on transferring servicing rights for the loan. This disclosure, while not detailing loan costs or terms specifically, is akin to the Loan Estimate in its aim to inform borrowers about significant administrative aspects of their mortgage, such as whether their loan payments might be managed by a different company in the future.

The Annual Escrow Statement, although specific to the accounting of funds placed in escrow rather than loan costs or terms, shares a common theme with the Loan Estimate by detailing future housing-related expenses. It provides an annual account of escrow payments for property taxes, homeowners insurance, and other charges, helping borrowers manage and anticipate their housing-related spending.

The Initial Escrow Statement resembles the Loan Estimate by detailing the expected costs to be paid from the escrow account during the first year of the mortgage. It itemizes the insurance premiums, taxes, and other charges that the lender will pay on behalf of the borrower, thus ensuring that these crucial bills are paid on time and helping the borrower budget for these expenses.

The Appraisal Disclosure is related to the Loan Estimate as it informs the borrower of their right to receive a copy of any appraisal performed on the property and the purpose of the appraisal. While the Loan Estimate lists fees associated with obtaining an appraisal, the Appraisal Disclosure focuses specifically on the borrower's rights regarding its review and the role of the appraisal in lending decisions.

The Affiliated Business Arrangement (AfBA) Disclosure is required when a settlement service provider involved in a real estate transaction refers the consumer to an affiliate for another settlement service. Like the Loan Estimate, it aims to inform consumers about potential costs and relationships that could affect the transaction, ensuring transparency.

The Right to Rescind notice is primarily associated with refinances, home equity loans, or lines of credit on a person’s primary residence, providing borrowers a window to cancel the contract without penalty. Although distinct in purpose from the Loan Estimate, it plays a crucial role in informing borrowers of their rights and is a key document in promoting borrower awareness and protection in the lending process.

When filling out a Loan Estimate form, there are specific do's and don'ts that can help streamline the process and avoid common pitfalls. Here’s a list to guide you:

Remember, a Loan Estimate is an essential document that outlines the terms of your mortgage. Handling it with care can lead to a smoother mortgage application process.

Many people find the process of buying a home confusing, especially when it comes to understanding the Loan Estimate form. It's crucial to clear up common misconceptions about this form to make informed decisions. Here are six common misunderstandings:

Understanding these points about the Loan Estimate form can help you navigate the home buying process more effectively and potentially save money. It's always advisable to ask questions and discuss any concerns with your lender to ensure you fully understand your loan options and the associated costs.

Understanding the Loan Estimate form is crucial when you're considering a mortgage. Here are key takeaways to help you navigate this document:

It's essential to review the Loan Estimate carefully, ask questions, and compare offers to ensure you choose the best mortgage for your financial situation.

Affidavit of Custody - Mentions that revocation must be verified before an authorized official and delivered to the child's other parent and relevant court clerk.

Post Office Resignation Form - A vital tool for managing personnel changes, safeguarding employee rights, and privacy.