Fill a Valid Michigan Property Transfer Affidavit 2766 Form

Fill a Valid Michigan Property Transfer Affidavit 2766 Form

When a piece of property in Michigan changes ownership, a vital document known as the Michigan Property Transfer Affidavit 2766 form must be completed. This form serves as a critical part of the real estate transaction process, ensuring local tax assessing offices are informed of the transfer. The completion of this form triggers an assessment of the property's value, which could potentially alter the property tax obligations for the new owner. Timeliness is crucial, as the form must be filed within 45 days of the transfer to avoid any penalties. Furthermore, accurate completion of the form is essential to ensure that the new property owner is properly recorded in municipal records. This affidavit, while seemingly straightforward, plays a significant role in the conveyance of property, emphasizing the importance of understanding its requirements, the implications of the data provided, and the legal consequences of the property transfer within Michigan's regulatory framework.

Reset Form

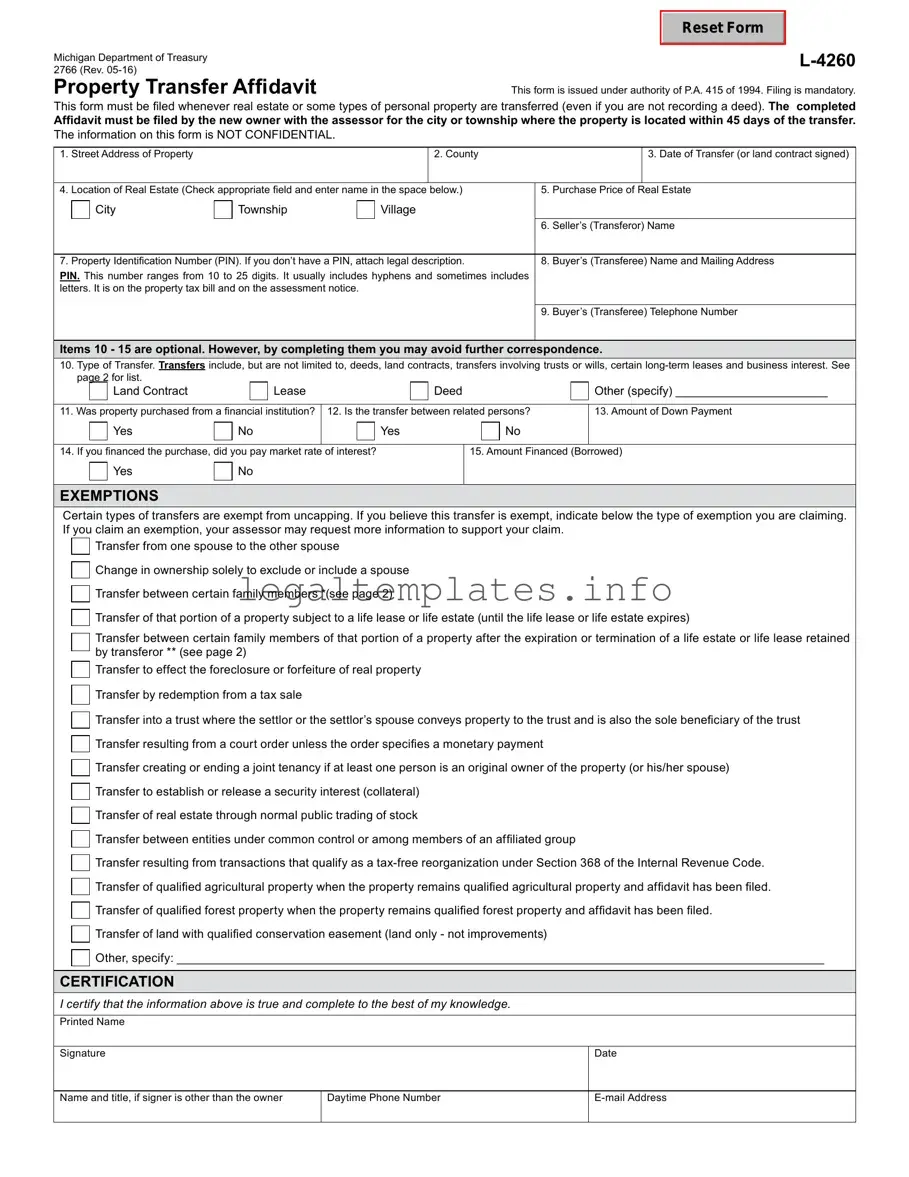

This form is issued under authority of P.A. 415 of 1994. Filing is mandatory.

This form must be filed whenever real estate or some types of personal property are transferred (even if you are not recording a deed). The completed

Affidavit must be filed by the new owner with the assessor for the city or township where the property is located within 45 days of the transfer. The information on this form is NOT CONFIDENTIAL.

1. |

Street Address of Property |

|

|

|

|

2. County |

|

|

3. Date of Transfer (or land contract signed) |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Location of Real Estate (Check appropriate field and enter name in the space |

below.) |

5. |

Purchase Price of |

Real Estate |

|||||

|

|

City |

|

Township |

|

Village |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

6. |

Seller’s (Transferor) Name |

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Property Identification Number (PIN). If you don’t have a PIN, attach legal description. |

8. |

Buyer’s (Transferee) Name and Mailing Address |

|||||||

PIN. This number ranges from 10 to 25 digits. It usually includes hyphens and sometimes includes |

|

|

|

|||||||

letters. It is on the property tax bill and on the assessment notice. |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Buyer’s (Transferee) Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

Items 10 - 15 are optional. However, by completing them you may avoid further correspondence.

10.Type of Transfer. Transfers include, but are not limited to, deeds, land contracts, transfers involving trusts or wills, certain

|

|

Land Contract |

|

|

|

Lease |

|

|

|

|

Deed |

|

Other (specify) _______________________ |

|||

|

|

|

|

|

||||||||||||

11. Was property purchased from a financial institution? |

12. Is the transfer between related persons? |

|

13. Amount of Down Payment |

|||||||||||||

|

|

Yes |

|

No |

|

|

Yes |

|

|

|

|

No |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|||||||||||

14. If you financed the purchase, did you pay market rate |

of interest? |

|

|

15. Amount Financed (Borrowed) |

||||||||||||

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXEMPTIONS

Certain types of transfers are exempt from uncapping. If you believe this transfer is exempt, indicate below the type of exemption you are claiming. If you claim an exemption, your assessor may request more information to support your claim.

Transfer from one spouse to the other spouse

Change in ownership solely to exclude or include a spouse

Transfer between certain family members *(see page 2)

Transfer of that portion of a property subject to a life lease or life estate (until the life lease or life estate expires)

Transfer between certain family members of that portion of a property after the expiration or termination of a life estate or life lease retained by transferor ** (see page 2)

Transfer to effect the foreclosure or forfeiture of real property

Transfer by redemption from a tax sale

Transfer into a trust where the settlor or the settlor’s spouse conveys property to the trust and is also the sole beneficiary of the trust Transfer resulting from a court order unless the order specifies a monetary payment

Transfer creating or ending a joint tenancy if at least one person is an original owner of the property (or his/her spouse)

Transfer to establish or release a security interest (collateral)

Transfer of real estate through normal public trading of stock

Transfer between entities under common control or among members of an affiliated group

Transfer resulting from transactions that qualify as a

Transfer of land with qualified conservation easement (land only - not improvements)

Other, specify: __________________________________________________________________________________________________

CErTIfICaTION

I certify that the information above is true and complete to the best of my knowledge.

Printed Name

Signature

Date

Name and title, if signer is other than the owner

Daytime Phone Number

2766, Page 2

Instructions:

This form must be filed when there is a transfer of real property or one of the following types of personal property:

•Buildings on leased land.

•Leasehold improvements, as defined in MCL Section 211.8(h).

•Leasehold estates, as defined in MCL Section 211.8(i) and (j).

Transfer of ownership means the conveyance of title to or a present interest in property, including the beneficial use of the property. For complete descriptions of qualifying transfers, please refer to MCL Section

Excerpts from Michigan Compiled Laws (MCL), Chapter 211

**Section 211.27a(7)(d): Beginning December 31, 2014, a transfer of that portion of residential real property that had been subject to a life estate or life lease retained by the transferor resulting from expiration or termination of that life estate or life lease, if the transferee is the transferor’s or transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the transfer. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subdivision. If a transferee fails to comply with a request by the department of treasury or assessor under this subdivision, that transferee is subject to a fine of $200.00.

*Section 211.27a(7)(u): Beginning December 31, 2014, a transfer of residential real property if the transferee is the transferor’s or the transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the conveyance. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subparagraph. If a transferee fails to comply with a request by the department of treasury or assessor under this subparagraph, that transferee is subject to a fine of $200.00.

Section 211.27a(10): “... the buyer, grantee, or other transferee of the property shall notify the appropriate assessing office in the local unit of government in which the property is located of the transfer of ownership of the property within 45 days of the transfer of ownership, on a form prescribed by the state tax commission that states the parties to the transfer, the date of the transfer, the actual consideration for the transfer, and the property’s parcel identification number or legal description.”

Section 211.27(5): “Except as otherwise provided in subsection (6), the purchase price paid in a transfer of property is not the presumptive true cash value of the property transferred. In determining the true cash value of transferred property, an assessing officer shall assess that property using the same valuation method used to value all other property of that same classification in the assessing jurisdiction.”

Penalties:

Section 211.27b(1): “If the buyer, grantee, or other transferee in the immediately preceding transfer of ownership of property does not notify the appropriate assessing office as required by section 27a(10), the property’s taxable value shall be adjusted under section 27a(3) and all of the following shall be levied:

(a)Any additional taxes that would have been levied if the transfer of ownership had been recorded as required under this act from the date of transfer.

(b)Interest and penalty from the date the tax would have been originally levied.

(c)For property classified under section 34c as either industrial real property or commercial real property, a penalty in the following amount:

(i)Except as otherwise provided in subparagraph (ii), if the sale price of the property transferred is $100,000,000.00 or less, $20.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $1,000.00.

(ii)If the sale price of the property transferred is more than $100,000,000.00, $20,000.00 after the 45 days have elapsed.

(d)For real property other than real property classified under section 34c as industrial real property or commercial real property, a penalty of $5.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $200.00.

| Fact | Description |

|---|---|

| Legal Requirement | The Michigan Property Transfer Affidavit Form 2766 must be filed whenever real estate or some types of personal property are transferred, even if no money changes hands. |

| Governing Law | This form is governed by the General Property Tax Act in Michigan. |

| Deadline for Filing | The affidavit needs to be filed within 45 days of the transfer to avoid penalties. |

| Filing Location | It is filed with the local assessor in the municipality where the property is located. |

| Purpose | The purpose of the form is to alert the assessor of a change in property ownership, which may affect the property's taxable value. |

| Penalty for Late Filing | A penalty of $5 per day (up to $200 maximum) is assessed for late filings. |

| Who Must File | The new owner or the owner’s designated representative must file the form. |

| Information Required | The form requires detailed information about the transfer, including the date of transfer, the parties involved, and the property's description. |

| No Fee for Filing | There is no fee for filing the Michigan Property Transfer Affidavit. |

When a property in Michigan changes hands, a crucial step in the process is completing the Property Transfer Affidavit (Form 2766). This document must be filed with the local assessor's office in the municipality where the property is located, within 45 days of the transfer. Failure to do so can lead to penalties. Filling out this form accurately is essential for ensuring the transfer is properly recorded and that property tax assessments reflect the new ownership. The process might seem complex at first glance, but by following a step-by-step approach, you can complete the form correctly and efficiently.

After submitting the Property Transfer Affidavit, the local assessor will review the information to ensure the property records are updated to reflect the new ownership and to adjust the property tax assessment as necessary. It’s a simple yet vital step in the property transfer process in Michigan, ensuring that both buyer and seller fulfill their legal obligations and that the property tax rolls are accurate.

What is a Michigan Property Transfer Affidavit 2766 form?

This form is a legal document required by the state of Michigan whenever there is a transfer of ownership in property. It informs the local assessing officer of the change, helping to ensure that property taxes are accurately assessed and updated in accordance with the transfer.

When is the Michigan Property Transfer Affidavit 2766 form due?

The completed form must be filed with the local assessor's office within 45 days of the transfer of property. If it is not filed within this timeframe, a penalty may be imposed.

Where can I find the Michigan Property Transfer Affidavit 2766 form?

It is available on the Michigan Department of Treasury's website. Additionally, you may also obtain it from your local assessor's office.

Who is responsible for filling out and submitting this form?

The responsibility typically falls on the buyer or the transferee of the property. However, the seller or transferor may complete it as part of the closing process on behalf of the buyer.

What information do I need to complete the form?

You will need to provide detailed information about the property transfer, including the date of transfer, the sale price, and the parties involved. Additionally, you'll need to describe the property and its location.

Is there a penalty for not filing the Michigan Property Transfer Affidavit 2766 form?

Yes, failure to file the form within the 45-day period may result in a penalty. The specific amount can vary, but it's often calculated based on the taxes assessed on the property.

Can I file this form online?

Whether you can file online depends on the local assessor's office. Some may accept electronic submissions, while others require a physical copy. It's best to check with the local office directly for their filing requirements.

What happens after I submit the form?

Once submitted, the local assessing officer will review the information to update the property's tax records. This may affect the property's tax assessments and taxable value.

Do I need to submit this form if I'm transferring property to a family member?

Yes, any transfer of property ownership, regardless of whether it's sold or transferred to a family member without a sale, requires filing this affidavit.

How do I know if my form has been processed?

The local assessor's office can provide an update on the status of your affidavit. Some offices may send a confirmation once the affidavit has been processed.

Filling out the Michigan Property Transfer Affidavit 2766 is a critical step in the property transfer process. However, mistakes are common, often stemming from a lack of understanding or oversight. One key error involves the incorrect listing of the property's legal description. This details not just the address but a legally recognized description of the property boundaries and identifiers, which can usually be found on the deed. A mismatch here can lead to significant delays or issues down the line. Therefore, precision is paramount.

Another frequent oversight is failing to accurately declare the transfer value. This figure isn’t just the sale price but encompasses the total value exchanged for the property. It might include personal property that's part of the deal or other considerations. An inaccurate value can raise red flags with tax authorities, potentially triggering audits or reassessments. Getting this number right the first time is crucial for a smooth transaction.

Not properly indicating the relationship between the buyer and the seller is yet another common mistake. This may seem like a minor detail, but it has significant tax implications. In Michigan, certain relationships between buyer and seller might qualify for exemptions or different tax treatments. If this portion is filled out incorrectly or skipped, parties might miss out on beneficial tax rules, leading to unnecessary expenditures.

Additionally, some people forget to sign and date the affidavit. While this oversight seems minor, the entire document becomes invalid without the signature of the seller or the legal agent. An unsigned affidavit can halt the entire transfer process, requiring parties to start over again, causing delays and possibly affecting the terms of the property transfer agreement.

Last but certainly not least, individuals often underestimate the importance of filing the affidavit within the required timeframe. Michigan law mandates that this document be filed within a specific period following the property transfer. Failure to comply with this timeline can result in penalties, including but not limited to, fines. It's vital for parties involved in the property transaction to be aware of these timelines to ensure compliance and a seamless transfer process.

When handling property transactions in Michigan, the Property Transfer Affidavit Form 2766 is a critical document that notifies the local assessor's office about the transfer of ownership. This form helps ensure the accuracy of public records and the assessment of property taxes. However, this affidavit is often not the only form needed to complete a property transaction smoothly. A number of other forms and documents usually accompany the Property Transfer Affidavit to comply fully with Michigan law and to protect the interests of all parties involved.

While the Property Transfer Affidavit Form 2766 is a starting point in property transactions, the addition of these documents can provide a comprehensive legal framework to ensure the transfer is conducted legally and efficiently. Each document plays a vital role in clarifying the terms of the transaction, protecting the rights of all parties involved, and fulfilling state requirements. For those navigating the complexities of property transfer, understanding and preparing these additional forms and documents is crucial to a successful and smooth transaction.

The Michigan Property Transfer Affidavit 2766 is a crucial document required in the process of transferring property ownership within the state of Michigan. It shares similarities with other forms and documents used in real estate transactions and property management across different jurisdictions. Each of these documents plays a vital role in ensuring the accuracy and legality of information regarding property ownership and transactions.

One similar document is the Warranty Deed. This legal instrument guarantees that the title being transferred is free and clear of liens or claims. Like the Michigan Property Transfer Affidavit 2766, it serves as a vital record that ensures the buyer is gaining full rights to the property. However, while the affidavit primarily asserts that a transfer has occurred and provides details about the new owner, the Warranty Deed goes further by offering guarantees about the property's title.

The Quitclaim Deed also shares similarities with the Michigan Property Transfer Affidavit 2766, as it is used in property transfers. However, unlike the affidavit that merely declares the fact of a transfer, the Quitclaim Deed actually effects the transfer of interest a seller (grantor) has in a property to a buyer (grantee) without any warranties regarding the quality of the title.

Another related document is the Grant Deed, used to transfer property while implying certain promises about the property’s title, but not as extensive as those guaranteed by a Warranty Deed. Like the Michigan Property Transfer Affidavit, it is integral to the real estate transfer process but focuses on the deed of transfer and the warranties involved rather than merely stating the transfer's occurrence and the parties involved.

The Deed of Trust is another document related to property transactions, acting as an instrument to secure a loan on a property. While the Michigan Property Transfer Affidavit records a transfer event and its particulars, the Deed of Trust involves a borrower, lender, and trustee, focusing on the legal framework for handling the property if the borrower fails to fulfill loan obligations.

Furthermore, the Declaration of Homestead is comparable because it involves property documentation, protecting a portion of a homeowner's equity from creditors. Although it doesn't facilitate the transfer of property like the Michigan Property Transfer Affidavit, it is crucial for property owners asserting protection under state law.

The Title Insurance Policy also relates closely, offering protection against losses from title defects, unlike the affidavit’s role in declaring a property transfer. This policy is rooted in a thorough examination of property records to safeguard against future claims or legal issues over ownership, which complements the transparency and record-keeping the affidavit contributes to.

Property Tax Assessment Forms, used by local governments to determine property taxes, share the feature of recording property details for official purposes. While these forms focus on valuation and tax implications rather than ownership transfer, they are essential records that, like the affidavit, ensure the proper authorities have accurate property information.

The HUD-1 Settlement Statement, used in real estate transactions to itemize services and fees charged to the buyer and seller, encapsulates financial details of a transfer, not dissimilar to how the Michigan Property Transfer Affidavit captures the factual details of the ownership change. Both documents are integral to the closing process, ensuring transparency and a clear record of the transaction.

Lastly, the Real Estate Transfer Tax Declaration Form, which is required in certain jurisdictions, involves declaring property value for tax purposes at the time of transfer, much like the Michigan Property Transfer Affidavit acknowledges a transfer and provides details about it. This form is essential for calculating any taxes due on the transaction, highlighting its importance in the financial aspects of property transfers.

Each of these documents, while differing in purpose and specifics, is intertwined with the process of transferring property ownership. They collectively ensure that property transactions are conducted fairly, transparently, and with due diligence, safeguarding the interests of all parties involved.

Filling out the Michigan Property Transfer Affidavit 2766 form is a crucial process that requires accuracy and attention to detail. The affidavit serves as a notification to the local assessor of a change in property ownership, which might affect property tax assessments. Ensuring the form is completed correctly and thoroughly can avert potential legal issues or delays in the transfer process. Below are essential dos and don'ts to guide you through completing the form effectively.

Dos:When dealing with the Michigan Property Transfer Affidavit 2766 form, several misconceptions can lead to confusion and mishandling of property transfers. Understanding and clarifying these misconceptions is crucial for property owners, buyers, and professionals involved in real estate transactions.

It's only for sellers: A common misconception is that the Property Transfer Affidavit is solely the responsibility of the seller. In reality, both the seller and the buyer have interests in ensuring that this form is correctly filled out and submitted. It serves to update the local assessor's records to reflect the new ownership and ensure that tax assessments are sent to the correct person.

Filing is optional: Some people believe that filing the Property Transfer Affidavit is optional. This is incorrect. In Michigan, the law requires that this affidavit be filed with the local assessor's office within 45 days of the property transfer. Failure to do so can result in penalties and interest charges.

No deadline consequences: Another misconception is that missing the 45-day filing deadline has no significant consequences. However, failing to file on time can lead to a penalty of $5 per day, up to $200. Additionally, it can complicate property tax assessments and exemptions.

Only needed for sales: It's often thought that the affidavit is only needed when a property is sold. But, in truth, this form is required for any transfer of ownership, whether by sale, inheritance, or gift, among other scenarios. It ensures that all transfers are properly documented and assessed for tax purposes.

Electronic filing is accepted everywhere: While electronic filing is becoming more common, not all municipalities in Michigan accept electronic submissions of the Property Transfer Affidavit. It's important to check with the local assessor's office to determine the accepted methods of submission.

It's only about property taxes: While a primary purpose of the form is to aid in the proper assessment of property taxes, it also plays a role in updating public records regarding property ownership. This can affect voting districts, school district boundaries, and eligibility for local services.

Professional help isn't necessary: Many individuals believe they can manage the filing of the Property Transfer Affidavit without any assistance. While it's possible to do so, understanding the nuances and implications of the information provided on the form can be challenging. Getting help from a professional can ensure accuracy and compliance, preventing potential issues down the road.

Clearing up these misconceptions is essential for a smooth property transfer process. Property buyers, sellers, and heirs should familiarize themselves with the requirements and ramifications of the Michigan Property Transfer Affidavit 2766 form to ensure compliance and avoid unnecessary complications.

When dealing with the transfer of property ownership in Michigan, the Property Transfer Affidavit Form 2766 plays a crucial role. Here are six key takeaways to understand when filling out and using this form:

Completing and submitting the Michigan Property Transfer Affidavit Form 2766 accurately and promptly is crucial for a smooth transition of property ownership and ensuring compliance with local tax laws. Always check the latest requirements and guidelines provided by the local assessor's office.

How to Upgrade Other Than Honorable Discharge - Filling out the DD Form 149 requires detailed explanations and any available evidence of the error.

What Is I9 Form - The precise retention period for the I-9 form depends on how long an employee remains employed and the date the form was completed.

14653 - Filing this form could lead to a balance due notice or refund if the reported tax or interest calculations differ from IRS determinations.