Fill a Valid Mortgage Statement Form

Fill a Valid Mortgage Statement Form

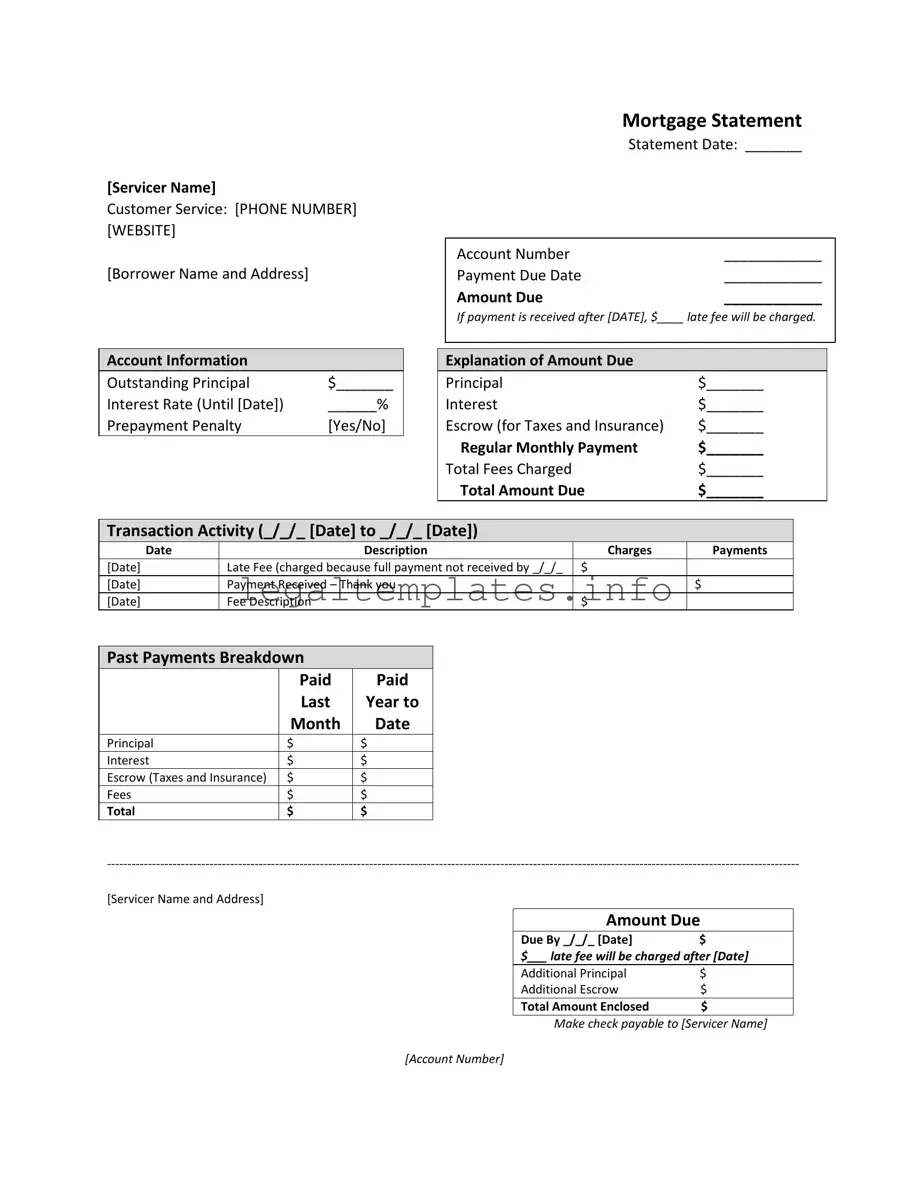

Understanding the Mortgage Statement form is crucial for anyone with a mortgage. It provides detailed information about your loan, including the name and contact details of your servicer, your account number, and crucial dates like when your next payment is due. Importantly, it outlines any late fees that apply if your payment isn't received by a specified date. The statement breaks down your payment into principal, interest, and, if applicable, escrow amounts for taxes and insurance, offering a clear overview of where your money is going. It also lists the total fees charged and the total amount due, ensuring you know exactly what you owe. Beyond just a summary of charges, the Mortgage Statement gives a transaction activity record, showing charges, payments, and any fees incurred over a reporting period. It even details past payment performance, comparing what was paid this year against the last, across principal, interest, escrow (for taxes and insurance), and fees. The form ends with crucial messages about the implications of partial payments, the seriousness of delinquency, and a reminder for those facing financial difficulties that help is available. This comprehensive document is designed to keep borrowers fully informed about their mortgage status, helping them manage their loans effectively and avoid any surprises.

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

| Fact | Description |

|---|---|

| Statement Structure | Includes information such as servicer's contact details, borrower's name and address, statement date, account number, payment due date, and amount due. Also, specifies if a late fee applies for payments received after a certain date. |

| Account Information | Details the outstanding principal, interest rate applicable until a specific date, and whether there's a prepayment penalty. |

| Explanation of Amount Due | Breaks down the total amount due into principal, interest, escrow (for taxes and insurance), regular monthly payment, total fees charged, and the cumulative total amount due. |

| Transaction Activity | Chronologically lists all transactions made within a specified period, including dates, descriptions, charges, payments, and late fees if applicable. |

| Important Messages | Advises on the handling of partial payments, delinquency notices including the consequences of failing to make timely payments, and provides information on obtaining mortgage counseling or assistance if experiencing financial difficulty. |

Filling out a mortgage statement form is a crucial step for maintaining clarity and accuracy in your financial dealings with your mortgage servicer. This document typically provides detailed information about your mortgage payments, including the principal, interest, escrow amounts, and any fees charged. To ensure that this form is filled out correctly, follow these instructions carefully.

Once you've filled out the mortgage statement form accordingly, make sure to review each section for accuracy. This form is a valuable document for both you and your servicer, serving as a record of your payments and assisting in the management of your mortgage. Timely and accurate completion and submission of your mortgage statement will help you maintain a good relationship with your servicer and keep your mortgage account in good standing.

What is a Mortgage Statement?

A Mortgage Statement is a document provided by your mortgage servicer that gives you information about your mortgage, including the outstanding principal, interest rate, payment due date, and amounts due for principal, interest, escrow, fees, and any late charges. It helps you understand how your payments are applied and tracks the activity on your account.

How can I find out what my payment due date is?

Your payment due date is clearly listed at the top section of your mortgage statement. It is the date by which your next payment must be made to avoid any late fees. Make sure to check the statement date and the due date to keep your payments on track.

What happens if I make a payment after the due date?

If a payment is received after the due date specified on your mortgage statement, you will be charged a late fee. The amount of this fee and the date after which it will be charged are both listed on the statement. To avoid this charge, ensure your payment reaches your servicer before the late fee applies.

What does “Escrow” mean on my Mortgage Statement?

"Escrow" on your Mortgage Statement refers to the funds collected by your servicer each month to pay for taxes and insurance on your behalf. These amounts are kept in an escrow account and are then used to pay your property taxes and homeowners insurance, ensuring these bills are paid on time.

What is a Prepayment Penalty?

A Prepayment Penalty is a fee that might be charged if you pay off your mortgage early. Your Mortgage Statement will indicate whether a prepayment penalty applies to your loan (Yes/No), allowing you to understand the financial implications of paying your mortgage off before its maturity date.

Why might I see a "Delinquency Notice" on my Mortgage Statement?

A "Delinquency Notice" appears when you are late on your mortgage payments. This notice serves as a warning that failure to bring your loan current may result in additional fees and even foreclosure. It includes information on how many days you are delinquent and the total amount due to bring your loan current, emphasizing the seriousness of making timely payments.

What should I do if I’m experiencing financial difficulty?

If you are experiencing financial difficulty and struggling to keep up with your mortgage payments, your Mortgage Statement includes information on how to seek mortgage counseling or assistance. It's important to act quickly to explore potential options and solutions that might be available to you to avoid delinquency and potential foreclosure.

One common mistake when filling out the Mortgage Statement form is inaccurately entering the Borrower Name and Address. This crucial information links the mortgage to the correct person and property. Entering incorrect details can lead to misdirected statements or legal notices.

Another error involves the Statement Date and Payment Due Date. People occasionally misinterpret these dates or enter them mistakenly, leading to confusion about when payments are due, potentially causing late payments and unnecessary fees.

The section asking for the Amount Due and details if the payment is received after a certain date is often misunderstood. Some fail to realize the significance of the specified date, risking a late fee by missing the deadline. This misunderstanding can be costly over time.

On the form, the Account Information segment, including the Outstanding Principal, Interest Rate, and Prepayment Penalty, is sometimes completed without accurate comprehension. Misinterpreting these figures can lead to incorrect assumptions about the loan's terms and one's financial obligations.

Errors in the Explanation of Amount Due section, incorporating principal, interest, and escrow, occur when individuals overlook the detailed breakdown of their total monthly payment. This oversight can result in misunderstandings about how payments are allocated and the importance of each component.

Within the Transaction Activity log, a frequent mistake is not accurately recording transactions, like payments and fees. This can create discrepancies in records, making it difficult to manage or dispute account statements.

The Past Payments Breakdown section, intended to provide a historical snapshot of mortgage payments, suffers from inaccuracies when individuals fail to correctly categorize payments into principal, interest, escrow, and fees. These errors can distort one’s understanding of how much of the loan has been paid off over time.

In documenting the Amount Due at the end of the form, including any late fees after the specified date, people often misread or miscalculate the total amount owed. This mistake can result in underpayments or overpayments.

Under the section for Important Messages, overlooking notes about partial payments and delinquency notices is a significant error. Not understanding the terms regarding partial payments and the consequences of delinquency can have serious implications for one's financial status and credit health.

Lastly, ignoring the instructions for Experiencing Financial Difficulty can be a critical oversight. This section provides essential information on seeking mortgage counseling or assistance, and overlooking it can mean missing out on potentially helpful resources to navigate financial challenges.

When you're dealing with mortgage-related paperwork, the Mortgage Statement is a pivotal document that captures the essentials about your loan, such as the outstanding principal, interest rate, and payment due dates. It gives a snapshot of your loan's health and is one part of a larger ecosystem of documents that support and explain various aspects of mortgage management and property ownership. Apart from the Mortgage Statement, there are several other key documents and forms that often come into play. These documents serve various purposes, from outlining the terms of the loan to ensuring that the property remains adequately insured.

Understanding these documents is essential for anyone navigating the process of obtaining and maintaining a mortgage. Each plays a unique role in ensuring that borrowers and lenders have a clear, shared understanding of the loan's terms, the property's status, and their respective rights and obligations. With these documents in hand, borrowers can better manage their property and their financial responsibilities toward it.

The Loan Amortization Schedule is a document that shares similarities with the Mortgage Statement, particularly in the way it breaks down the borrower's payments over the loan's lifecycle. Like the Mortgage Statement, the Amortization Schedule outlines the portion of each payment attributed to the principal versus interest, and often includes information about taxes and insurance if those are escrowed. However, it provides a more comprehensive look forward, presenting the entire payment schedule from inception to the final payment, allowing borrowers to see how each payment reduces their principal balance over time and how much interest they are paying throughout the loan period.

An Account Statement from a bank or credit union parallels the Mortgage Statement in its function of updating customers on the status of their account for a specific period. It lists transactions, including deposits and withdrawals, similar to how a Mortgage Statement lists payment activity and any fees charged. The primary difference lies in the nature of the accounts: one covers banking transactions, while the Mortgage Statement specifically details the progress and performance of a mortgage loan, including payments made towards the principal, interest, and any escrow accounts for taxes and insurance.

The Property Tax Bill also shares characteristics with a Mortgage Statement, mainly due to the inclusion of escrow information on many Mortgage Statements. Both documents inform the borrower of the amounts due for property-related expenses, though the Property Tax Bill exclusively focuses on taxes owed to the local government. Where they overlap is in their mutual concern for property costs—many mortgage statements include an escrow portion specifically for covering expenses such as the property taxes and homeowner’s insurance, providing a summary of these expenses alongside the loan's payment information.

The Year-End Tax Statement, or Form 1098, which lenders send to borrowers, has a crucial connection to the Mortgage Statement. It summarizes the total interest and property taxes paid over the year and can include mortgage insurance premiums if applicable. Like the Mortgage Statement, it offers a breakdown of costs associated with the mortgage, albeit on an annual basis for tax purposes. Borrowers use it to claim potential tax deductions for interest paid. While the Mortgage Statement provides monthly or periodic snapshots, the Year-End Tax Statement aggregates this financial information for the entire year, highlighting the borrower's total expenditures on interest and taxes.

When filling out your Mortgage Statement form, it's important to approach the task with accuracy and attentiveness. Below are some tips on what you should and shouldn't do to help guide you through the process:

Do:By following these guidelines, you can help ensure that your Mortgage Statement is accurately completed, thus avoiding potential issues with your mortgage payments. Remember, taking the time to fill out the form correctly can save you time and prevent unnecessary stress in the future.

When it comes to understanding mortgage statements, several misconceptions can lead borrowers astray. Here are eight common misunderstandings and the truths behind them:

Truth: Even a payment received just after the due date can result in a late fee, and if consistently late, it can affect your credit score.

Truth: The statement provides a comprehensive view, including the outstanding principal, interest rate, and a breakdown of the most recent payment, including principal, interest, and escrow.

Truth: The interest rate shown is applicable until the next adjustment date; for adjustable-rate mortgages, this can change over time.

Truth: The statement reflects current details such as the outstanding balance and the amount due for the upcoming payment cycle, not the lifetime cost of the loan.

Truth: While you can make additional payments towards the principal, the mortgage statement will outline how partial payments are held in a suspense account until the full payment amount is met, at which point they are applied to the mortgage.

Truth: Fees such as late charges are part of the loan agreement; disputing them without valid grounds can be more challenging than expected.

Truth: An escrow account for taxes and insurance is typically required as part of your mortgage to ensure these expenses are paid on time.

Truth: While the mortgage statement may offer guidance or suggestions, especially regarding financial hardship, it does not constitute legal advice. Consulting with a financial advisor or attorney is recommended for personalized advice.

Understanding the details of a mortgage statement is crucial for managing your loan effectively and avoiding potential financial pitfalls. By dispelling these misconceptions, borrowers can make more informed decisions about their home finance needs.

Filling out and using the Mortgage Statement form correctly is crucial for both servicers and borrowers in ensuring clear communication and avoiding any misunderstandings. Here are key takeaways to consider:

This comprehensive understanding of the Mortgage Statement form enables borrowers to manage their mortgage responsibilities effectively, while servicers can ensure accurate and transparent communication with their clients.

Create Gift Certificate - Preparing a Gift Letter form is a straightforward process, but it must be done carefully to ensure all legal requirements are met.

Biopsychosocial Template - Includes an assessment of your ability to concentrate and complete tasks, relevant for ADHD or cognitive disorder considerations.

How to Check Your Pay Stub - It assists in the calculation of an accurate gross income for tax purposes.