Fill a Valid Profit And Loss Form

Fill a Valid Profit And Loss Form

Navigating through the complexities of business finances can be a daunting task, especially for those who are new to it or even for seasoned entrepreneurs looking to get a clearer picture of their business's financial health. Here, the Profit and Loss form, a vital document in the world of accounting and financial management, plays a crucial role. This essential tool is designed to provide a comprehensive overview of the company's revenues, costs, and expenses over a specific period. By meticulously detailing how a business's profits are generated and lost, it offers critical insights into operational efficiency, cost management, and the overall financial performance. Understanding the nuances and the major aspects of the Profit and Loss form can empower business owners and managers to make informed decisions that drive growth and sustainability in the competitive market landscape.

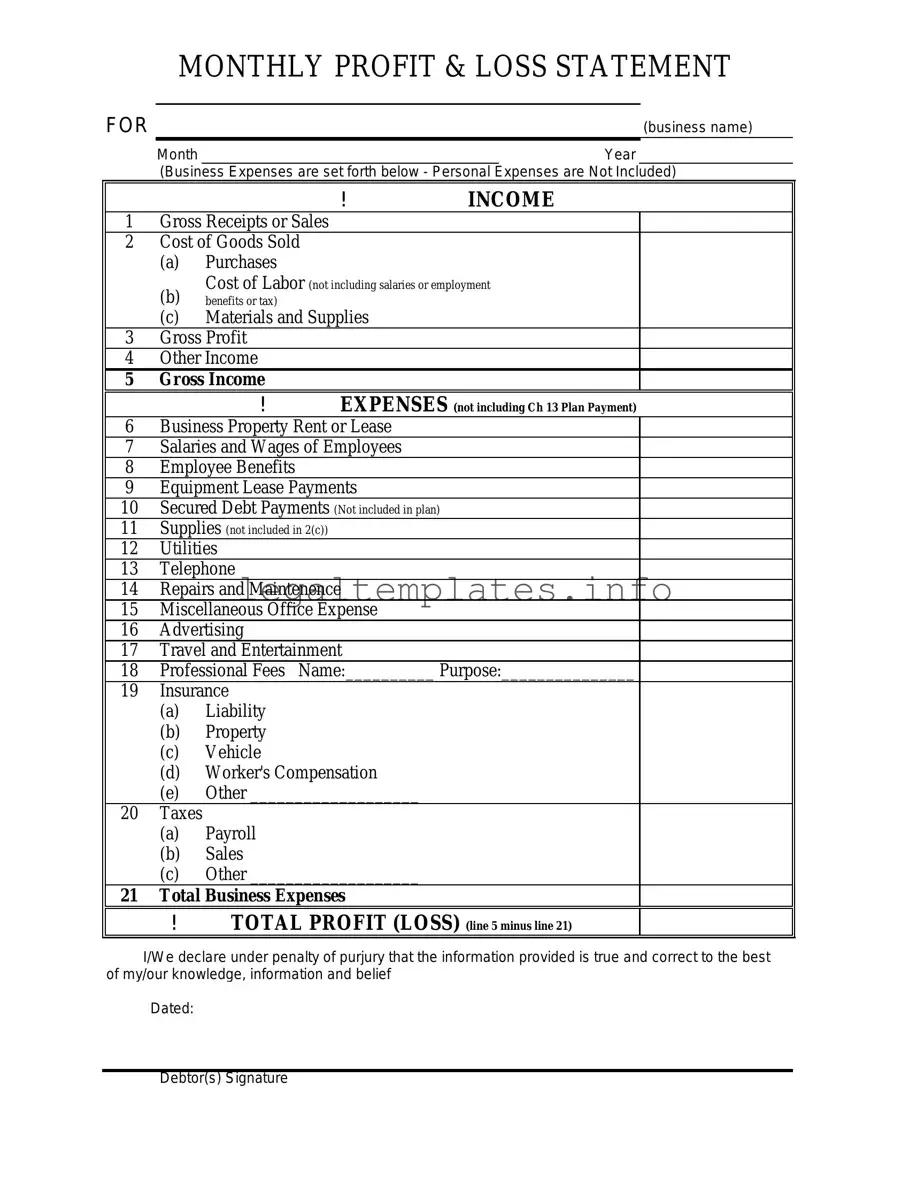

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Number | Description |

|---|---|

| 1 | A Profit and Loss (P&L) form is a financial statement that summarizes the revenues, costs, and expenses incurred during a specific period. |

| 2 | The standard period for a P&L statement is usually a fiscal quarter or year. |

| 3 | This form is also known as an income statement. |

| 4 | P&L statements are used by businesses to demonstrate their financial performance to investors, creditors, and other stakeholders. |

| 5 | The main components of a P&L statement include revenue, cost of goods sold (COGS), gross profit, operating expenses, and net income. |

| 6 | Gross profit is calculated by subtracting the cost of goods sold from total revenue. |

| 7 | Net income is determined by subtracting all expenses from the gross profit. |

| 8 | A positive net income indicates a profit, whereas a negative figure shows a loss. |

| 9 | State-specific P&L forms may be governed by local statutes that dictate specific reporting requirements or formats. |

| 10 | Electronic filing of P&L statements may be required by some jurisdictions, streamlining the process and improving accuracy. |

Filling out a Profit and Loss (P&L) form marks a crucial step for businesses in reporting their financial performance over a specific period. This form requires gathering detailed financial data and presenting it in a structured manner. This process not only aids in understanding a business's financial health but also is essential for tax purposes, securing loans, or attracting investors. The procedure demands accuracy and attention to detail. Below is a step-by-step guide to assist you in completing the P&L form accurately.

Once the form is accurately completed and reviewed, your business can use this critical document to assess its financial standing accurately, make informed decisions, and plan strategically for future growth. It's also a vital component of your business's financial transparency and compliance efforts. Whether for internal review, tax filing, or sharing with potential investors, a well-prepared Profit and Loss statement is indispensable in the world of business finance.

What is a Profit and Loss (P&L) form?

A Profit and Loss form, often referred to as an income statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period, usually a fiscal quarter or year. It provides a snapshot of a company's financial health, showing the net profit or loss after all operating expenses, including taxes and interest, have been subtracted from total revenue.

Why is a Profit and Loss form important?

This form is crucial for both the management of a company and its stakeholders as it highlights the company’s financial performance and profitability over time. For management, it serves as a tool for making informed business decisions. For investors and creditors, it's a reliable source of information to assess the financial health and viability of the company. It also aids in tax preparation, as it supports the calculation of taxable income.

Who needs to fill out a Profit and Loss form?

Generally, any business that seeks to track its operational success and financial health over a period needs to fill out a P&L form. This includes sole proprietors, partnerships, corporations, and limited liability companies. It is also essential for businesses seeking investments, loans, or lines of credit, as potential financiers will review this form to evaluate the company's financial stability and profitability.

What time period does the Profit and Loss form cover?

Typically, a P&L form is generated quarterly and annually. However, the time frame can be adjusted to meet specific needs or objectives, such as monthly reports for more frequent monitoring of financial performance or a custom period for comparative analysis or specific project assessments.

What are the key components of a Profit and Loss form?

The key components of a P&L form include revenue (or sales), cost of goods sold (COGS), gross profit, operating expenses, operating profit, other income and expenses, and net profit. These components collectively provide a detailed account of where revenue comes from, how it is spent, and what is left as profit.

How can one prepare a Profit and Loss form?

Preparing a P&L form involves collecting and categorizing all financial transactions within the reporting period. This process includes recording all revenue earned, subtracting the cost of goods sold to find the gross profit, then deducting operating expenses to reveal operating profit. Any other incomes or expenses must then be considered to calculate the net profit. Accuracy is crucial, and the use of accounting software or consultation with a financial professional might be beneficial.

Can a Profit and Loss form help in improving a business?

Yes, it can. By providing detailed insights into revenue streams and expense categories, a P&L form helps business owners identify areas of strength and pinpoint cost-saving opportunities. It also allows for the tracking of financial performance trends, assisting in strategic planning, budget adjustments, and decision-making processes aimed at enhancing profitability and ensuring sustainable growth.

One common mistake made when filling out the Profit and Loss form is not accurately categorizing expenses. Often, individuals might mix up operational costs with capital expenditures. Operational costs are the day-to-day expenses a business incurs to keep running, such as rent and utilities. Capital expenditures, on the other hand, are investments in assets that will benefit the business in the long term, like equipment or property. Misclassifying these can lead to a distorted financial picture, affecting the accuracy of the Profit and Loss statement.

Another frequent error is overestimating revenue. This mistake can occur when individuals record sales based on invoices issued rather than payments received, leading to a higher reported income. An accurate Profit and Loss statement relies on recognizing revenue only when it is earned and received, ensuring the financial health of a business is not overstated.

Failure to account for all expenses is also a critical mistake. It's easy to overlook or forget small, irregular expenses throughout the accounting period. However, every expense, no matter how minor, impacts the bottom line. Neglecting to record these expenses gives an inaccurate figure of net profit, potentially misleading stakeholders about the business's financial performance.

Incorrect time period reporting is a common pitfall as well. The Profit and Loss statement should reflect the financial activity within a specific, consistent period, whether monthly, quarterly, or annually. Mixing up dates or including transactions outside this timeframe disrupts the flow of financial information, making it challenging to track performance and trends accurately over time.

Last but not least, a significant oversight is not reviewing or double-checking the final figures. Errors in calculation or data entry can easily occur, leading to incorrect totals on the form. Taking the time to review the Profit and Loss statement can catch and correct these mistakes before they lead to incorrect assessments of a business's profitability and financial health.

When managing a business's finances, a Profit and Loss (P&L) form is crucial for understanding the company's earnings and expenditures over a specific period. However, to gain comprehensive insights into the financial health of a business, the P&L form is usually accompanied by several other important documents. These not only enhance the understanding of financial standings but also aid in making informed decisions for future business strategies.

Together, these documents form a comprehensive toolkit for financial management, providing a multi-dimensional view of a company's financial health. Accurate and up-to-date P&L forms, along with these supporting documents, empower business owners and managers to make strategic decisions based on solid financial data.

The Balance Sheet is one document that shares similarities with the Profit and Loss (P&L) form. While the P&L statement focuses on the income and expenses of a business over a period, the Balance Sheet provides a snapshot of the company's financial health at a specific point in time. It details the company's assets, liabilities, and shareholders' equity, offering a broader view of financial status. Both documents are essential for assessing the financial performance and position of a business, helping stakeholders make informed decisions.

The Cash Flow Statement is another document related to the P&L form. It tracks the flow of cash in and out of the business over a particular period, categorizing cash movements into operations, investing, and financing activities. Unlike the P&L, which operates on an accrual basis, reflecting earnings when they are earned and expenses when they are incurred, the Cash Flow Statement focuses on actual cash transactions. This distinction helps users understand the company's liquidity and cash management practices alongside its profitability.

A Statement of Retained Earnings also shares a connection with the P&L form. This document outlines the changes in retained earnings over a period, primarily influenced by net income (as reported on the P&L) and dividend payments. It bridges the gap between the P&L statement and the Balance Sheet by explaining how profits retained by the company affect its equity. By tracking how net income and dividends contribute to the retained earnings, stakeholders can gauge the firm's reinvestment strategy and financial robustness.

The Budget Report is often compared to the P&L form, although it serves a different function. While the P&L provides a historical record of income and expenses, the Budget Report is a forward-looking document that projects future financial performance based on various assumptions. Despite this difference, both are crucial for financial planning and control. By comparing actual figures in the P&L to the forecasts in the Budget Report, companies can assess their performance, adjust their strategies, and make informed financial decisions.

When approaching the task of filling out a Profit and Loss form, it's crucial to embrace a mix of accuracy, clarity, and caution. This financial document not only reflects the health of your business but also aids in strategic planning and assessment. Below you'll find a list of things you should do as well as a list of things you should avoid to ensure your Profit and Loss Statement stands as a true representation of your business's financial standing.

Things You Should Do

Ensure all income and expense categories are accurately represented, reflecting the true nature of your business operations.

Double-check all figures for accuracy. Simple arithmetic errors can significantly alter the appearance of your business's financial health.

Use historical financial statements for comparison, ensuring consistency in how income and expenses are reported and categorized.

Include all relevant income and expenses within the reporting period to provide a comprehensive overview of your financial activity.

Maintain documentation and receipts for all transactions to support the entries made in your Profit and Loss Statement.

Consider using accounting software to help automate and reduce errors in your financial reporting.

Seek professional advice when unsure about how to categorize income and expenses or if you encounter complex financial transactions.

Things You Shouldn't Do

Avoid guessing or estimating figures. Always use actual data to ensure accuracy in your reporting.

Don't overlook small expenses or sources of income; these can add up and significantly impact your Profit and Loss statement.

Resist the temptation to categorize non-operating income and expenses as regular operations to inflate or deflate your operational profitability.

Avoid using different accounting methods from one period to the next without a valid reason, as this can lead to inconsistencies and inaccuracies.

Don't rush through the process. Taking your time can help ensure every detail is correctly accounted for and reported.

Avoid keeping poor records throughout the year, which can make it difficult to accurately complete the Profit and Loss form when needed.

Do not forget to review and update the Profit and Loss statement periodically, not just at year-end, to keep a close eye on financial trends and health.

Understanding the Profit and Loss (P&L) form is vital for anyone running a business or involved in financial reporting. However, there are several misconceptions surrounding this financial statement that can lead to inaccuracies in how it's perceived and used. Below are seven common misconceptions and explanations to clarify each point.

Only for Large Businesses: A common misconception is that P&L forms are only necessary for large businesses. In reality, businesses of all sizes can benefit from P&L statements as they provide a clear overview of financial performance over a specific period, helping identify areas for improvement in both large and small operations.

Complicated to Prepare: Many people believe that preparing a P&L statement is complicated and requires extensive accounting knowledge. While it does require some basic understanding of financial principles, it's largely about tracking income and expenses accurately, a task that modern accounting software has made much more straightforward.

Only Concerns Revenue: It's a misconception that P&L statements only detail a company's revenue. They actually provide a more comprehensive view, including costs, expenses, and other financial activities, thereby offering a net profit or loss over the period.

Irrelevant for Non-Profit Organizations: Non-profit organizations might think P&L statements don't apply to them since their aim isn't to generate profit. However, these organizations still need to manage their finances effectively, track their sources of income versus expenses, and ensure they're operating within their budgetary confines, making P&L statements just as important for their financial health.

Annual Only Documents: Another common misconception is that P&L statements are only prepared annually. While annual statements are important for a comprehensive yearly overview, businesses often prepare monthly or quarterly P&L statements to keep a closer eye on financial trends and make timely adjustments.

Focus Solely on Past Performance: While P&L statements are historical documents, the misconception that they only focus on past performance overlooks their utility in planning for the future. Analyzing trends in these statements can provide valuable insight into how a business might perform under similar conditions, aiding in future decision-making.

Profit Equals Cash Available: Finally, it's a common mistake to equate net profit shown in a P&L statement with the amount of cash available to a business. Profit does not account for cash flow timing differences or reflect money designated for reinvestment or committed expenses. Understanding the distinction between profit and cash flow is critical for effective financial management.

Demystifying these misconceptions about the Profit and Loss form is crucial for anyone involved in a business's financial management. Accurate knowledge and application of P&L statements contribute to healthier business practices, informed decision-making, and ultimately, financial success.

The Profit and Loss (P&L) form is a crucial document that outlines a company's revenues, costs, and expenses during a specific period. This form helps in understanding the financial performance of a business. It's important to fill it out carefully and accurately for several reasons.

In summary, the Profit and Loss form is not just another piece of paperwork. It is an essential component of a business's financial practices. Its preparation should be approached with care and an understanding of its significance to the business's overall success.

Acord 130 - Companies must provide a narrative description of their business operations to help insurers understand the scope of coverage needed.

S Corp Abbreviation - Form 2553’s approval grants a corporation S status from the start of the tax year, changing how its financial activities are reported to the IRS.