Fillable Promissory Note Document

Fillable Promissory Note Document

When it comes to formalizing the agreement of a loan, whether between individuals or between a borrower and a lender, the Promissory Note form plays a pivotal role. This document, simple yet legally binding, outlines the promise by the borrower to repay a specific sum of money to the lender within a set timeframe. It details interest rates, repayment schedule, and the consequences of failing to repay the loan. Its significance cannot be overstated, as it provides clear terms and conditions, protecting both parties involved. Serving as a legally enforceable agreement, it ensures that the lender has a written commitment from the borrower to make good on the loan, making it an essential tool in both personal and business finance. Understanding the components and importance of this form is crucial for anyone considering lending or borrowing money, as it lays the groundwork for a transparent and secure transaction.

Promissory Note

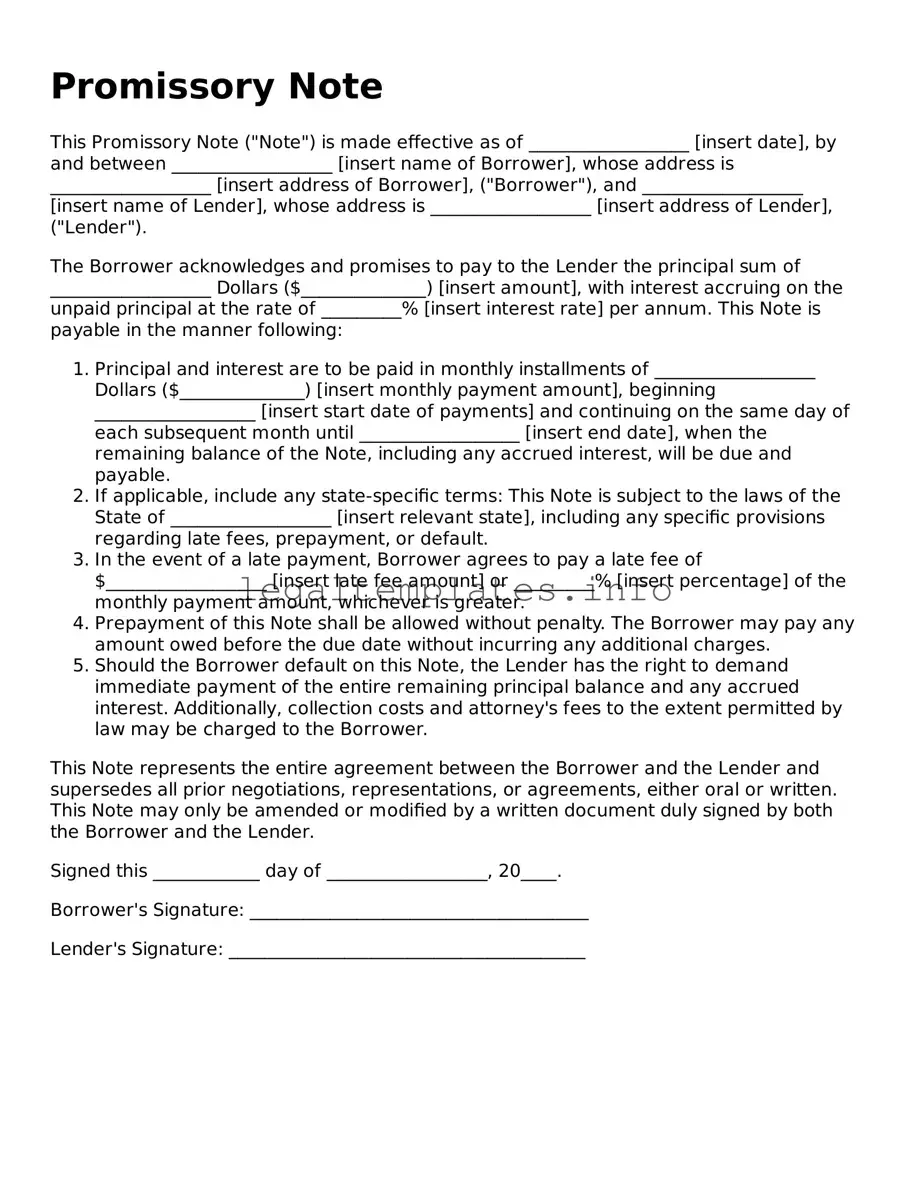

This Promissory Note ("Note") is made effective as of __________________ [insert date], by and between __________________ [insert name of Borrower], whose address is __________________ [insert address of Borrower], ("Borrower"), and __________________ [insert name of Lender], whose address is __________________ [insert address of Lender], ("Lender").

The Borrower acknowledges and promises to pay to the Lender the principal sum of __________________ Dollars ($______________) [insert amount], with interest accruing on the unpaid principal at the rate of _________% [insert interest rate] per annum. This Note is payable in the manner following:

This Note represents the entire agreement between the Borrower and the Lender and supersedes all prior negotiations, representations, or agreements, either oral or written. This Note may only be amended or modified by a written document duly signed by both the Borrower and the Lender.

Signed this ____________ day of __________________, 20____.

Borrower's Signature: ______________________________________

Lender's Signature: ________________________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a financial instrument that contains a written promise by one party (the issuer or maker) to pay another party (the payee) a definite sum of money, either on demand or at a specified future date. |

| Key Components | Typically, a promissory note includes the principal amount, interest rate, maturity date, date and place of issuance, and the issuer's signature. |

| Legal Enforceability | In the United States, a promissory note is a legally binding document. Failure to meet the obligations as outlined in the note can lead to legal consequences. |

| State-specific Forms and Governing Laws | While the general principles are similar, specific requirements for promissory notes, including interest rates and enforcement measures, can vary by state. Each state’s laws govern the execution and enforcement of promissory notes within that jurisdiction. |

| Types and Uses | Promissory notes can be secured or unsecured, invoking different levels of risk for the payee. They are used in a variety of financial transactions, including personal loans, business loans, and real estate transactions. |

Filling out a promissory note is a straightforward process, but requires attention to detail to ensure that all the terms are understood and agreed upon by both parties involved. This form constitutes a legal agreement regarding the repayment of a loan between a borrower and a lender. The next steps will walk you through the necessary information and documentation needed to accurately complete this form. Following these steps carefully will establish a clear understanding and commitment from both the lender and the borrower, laying out the loan amount, repayment schedule, interest rate, and what should occur if the borrower fails to make timely payments.

By following these steps, both parties will have a clear, legally binding document outlining the terms of the loan. This process not only formalizes the agreement but also serves to protect the interests of both the lender and the borrower. Completing a promissory note with accuracy and clarity is essential to ensuring that the loan process is successful and free from potential legal complications.

What is a Promissory Note?

A promissory note is a legal document in which one party agrees to pay a specified sum of money to another party under agreed-upon terms. This document outlines the loan amount, interest rate, repayment schedule, and any other conditions related to the financial agreement.

Who needs to sign the Promissory Note?

Both the borrower and the lender must sign the promissory note. The borrower's signature acknowledges their commitment to repay the borrowed amount under the terms specified in the note. The lender's signature confirms their agreement to the terms and their promise to lend the specified sum of money.

Can the terms of a Promissory Note be modified?

Yes, the terms of a promissory note can be modified, but any alterations must be agreed upon by both the lender and the borrower. Such modifications should be documented in writing, and both parties should append their signatures to the amended document to ensure its validity.

What happens if the Promissory Note is not repaid?

If the promissory note is not repaid according to the agreed-upon terms, the lender has the right to take legal action to recover the owed amount. Depending on the stipulations of the note and applicable state laws, this might involve the seizure of collateral, wage garnishment, or other enforcements to recover the debt.

Filling out a promissory note requires careful attention to detail, yet many people overlook important aspects. One common mistake is not specifying exact repayment terms. This includes the loan's interest rate and the repayment schedule. Without clear terms, misunderstandings and legal conflicts can arise over how and when the loan should be repaid.

Another error often made is neglecting to include the full legal names of all parties involved. For clarity and legal enforcement, it's crucial that each party's legal name is accurately recorded on the document. Using nicknames or incomplete names can lead to complications if the note needs to be enforced.

Many individuals forget to document the loan's purpose. Although it might seem unnecessary, recording why the loan is being given can be important, especially for tax or legal reasons. This small step can provide clarity and prevent potential disputes in the future.

Not specifying the collateral, if any, is another oversight. When a loan is secured with collateral, failing to clearly describe this collateral in the promissory note can weaken the lender's position if they need to seek repayment through seizing the collateral.

A significant number of people also fail to consider the need for a witness or notarization. While not always legally required, having the note witnessed or notarized can add a layer of verification and authenticity, which can be especially helpful if disputes arise.

Some people incorrectly believe that a promissory note doesn't need to be detailed if the parties know each other well. This assumption can lead to vague terms and conditions, which are not helpful if the agreement needs to be reviewed by a third party or enforced.

Omitting the governing law clause is yet another frequent mistake. This clause indicates under which state's laws the note will be interpreted. Without this, there can be uncertainty and legal challenges if there's a disagreement.

Failure to plan for the worst-case scenarios, such as late payments or default, is common. Terms should include late fees and the actions that will be taken in case of non-payment. This oversight can leave the lender in a difficult position if the borrower doesn't fulfill their obligations.

Residents of certain states sometimes overlook state-specific legal requirements. Laws can vary significantly from state to state, and what's optional in one might be compulsory in another. This can make the enforcement of the note problematic if it does not meet local legal standards.

Lastly, a common error is not keeping a copy of the signed document. Both parties should have a copy of the fully executed promissory note. Without this, proving the terms agreed upon can become a complex process if one party challenges the agreement.

A Promissory Note is a critical document used in various financial transactions, essentially serving as a written promise to pay a specified sum of money to a person at a predetermined time or on demand. While a Promissory Note can stand alone, it often works in conjunction with several other documents to ensure a comprehensive approach to the transaction. Each of these documents plays a vital role in clarifying the terms, securing the loan, and providing legal protections for all parties involved. Below is a list of documents often used alongside the Promissory Note.

In any financial transaction, comprehending each document’s role not only clarifies the obligations of all parties but also fortifies the legal standing of the agreement. Using these documents in tandem with a Promissory Note ensures a secure and enforceable arrangement, minimizing misunderstandings and potential disputes down the line. As always, it's advisable to consult with a legal professional to fully understand the implications of these documents and how they interact within the specific context of a loan agreement.

A promissory note, a written promise to pay a specified amount of money to a person at a specified time, bears similarity to various other financial and legal documents. One such similar document is a loan agreement. A loan agreement is more comprehensive than a promissory note, detailing the obligations and rights of the borrower and the lender. It often includes terms about the loan's interest rate, repayment schedule, and consequences of default, making it a detailed contract for borrowing money. While a promissory note signifies the borrower's promise to repay the loan, a loan agreement lays out the broader terms and conditions of the loan arrangement.

Mortgages share characteristics with promissory notes, primarily because a mortgage is essentially secured by real property as collateral against the loan. The promissory note indicates the borrower's promise to repay, whereas the mortgage document secures the loan and outlines the rights of the lender to take possession of the property if the borrower fails to make payments. Both documents work in tandem during property financing, signifying the financial obligation and the legal ramifications of not adhering to that obligation.

Another document similar to a promissory note is an IOU (I Owe You). An IOU is a simple acknowledgment of debt, though less formal and detailed. While an IOU merely states that one party owes another a specific sum of money, a promissory note provides detailed information about the debt, including repayment terms, interest rate, and the due date. The key difference lies in the level of detail and formality, with promissory notes being more formal and enforceable legal documents.

Debentures are similar to promissory notes in that they represent a loan made by an investor to a corporation. However, debentures are typically used by corporations to raise capital and often contain terms regarding the interest payments, repayment schedule, and collateral (if secured). Unlike promissory notes, which are usually more straightforward and involve personal loans, debentures are more complex and often used for larger, corporate financing.

Bonds, like promissory notes, are formal debt instruments that entities use to raise funds. Bonds obligate the issuer to pay back the face value of the bond to the investor at a specified maturity date, along with periodic interest payments. While promissory notes typically involve individual lenders and borrowers, bonds are often issued by corporations or government entities and tend to involve larger sums of money and longer repayment periods. Both serve as tools for financing, with each offering a written promise to repay the borrowed amount under agreed terms.

A line of credit agreement is another document that shares similarities with a promissory note, especially regarding the promise to repay borrowed funds. However, a line of credit agreement offers a maximum credit amount that the borrower can draw upon, not necessarily drawing the entire amount upfront. This flexibility is different from a promissory note, which usually involves a lump-sum loan that comes with specific repayment terms. While both documents obligate repayment, a line of credit offers more flexibility in the borrowing and repayment structure.

Installment contracts, commonly used for the purchase of goods over time, also resemble promissory notes. In both cases, the buyer promises to pay the seller a certain amount, either in lump sum or over a scheduled period, for goods or services. While a promissory note can be part of an installment plan, installment contracts focus more on the transaction of goods or services rather than just the borrowing of money. The terms of repayment are key in both documents, but their purposes diverge according to the nature of the transaction.

Personal guarantees can complement a promissory note, especially in securing loans. A personal guarantee is a separate agreement whereby an individual (the guarantor) agrees to fulfill the financial obligations of the borrower in case of default. While the promissory note records the borrower's promise to repay the lender, a personal guarantee ensures that another party can be held responsible for the debt, offering additional security to the lender. Both documents are used to strengthen the promise of repayment.

Last but not least, student loan agreements bear resemblance to promissory notes. Both documents entail a promise to repay borrowed money under specified conditions. While a promissory note can be used for various types of loans, student loan agreements are specifically designed for financing education and often include terms related to deferment, interest rates, and repayment plans tailored to the student's future earning potential. Even though they serve different purposes, at their core, both aim to document and enforce a repayment obligation.

When filling out a Promissory Note form, it is crucial to handle the process thoughtfully and meticulously. A promissory note is a legal document in which one party promises to pay another party a certain amount of money within a specified timeframe. To ensure clarity, legality, and enforceability, paying attention to how you complete the document is essential. Below are some recommendations to consider:

Adhering to these guidelines will help in creating a comprehensive and legally binding Promissory Note that protects the interests of all involved parties. Remember, the goal is to ensure the agreement is clear, fair, and enforceable, minimizing the potential for future disputes.

When it comes to understanding promissory notes, many people hold onto widely spread misconceptions. Let's clear up some of these misunderstandings to ensure everyone can approach these financial documents with confidence and clarity.

Promissory notes are legally binding only if notarized. This is a common misconception. In reality, while notarization can add a layer of authenticity and fraud prevention, a promissory note is legally binding when it contains the necessary elements and is signed by the parties involved, notarized or not.

All promissory notes are the same. Far from it, promissory notes can vary significantly depending on their purpose, terms, and the jurisdiction they are executed in. They can range from simple to complex, detailing different repayment structures, interest rates, and conditions.

Only financial institutions can issue them. This is not the case. Individuals can indeed issue promissory notes. This happens often in personal loans between family members or friends, where a promissory note secures the loan.

Verbal agreements are just as good as written promissory notes. While oral contracts can be enforceable, a written promissory note provides a clear, tangible record of the agreement and its terms, offering much stronger legal protection for both parties.

Promissory notes serve the same purpose as IOUs. Although both document a debt, a promissory note is more formal and contains comprehensive details about the loan’s terms, repayment schedule, interest, and consequences of non-payment.

No need to worry about a promissory note if you trust the other party. Trust is commendable, but circumstances can change. A written promissory note ensures clarity and protection for both parties, regardless of their relationship.

If the lender loses the note, the debt is forgiven. Losing the physical note doesn't erase the debtor’s obligation to repay. The lender can take legal steps to enforce the debt or have the promissory note replaced.

Promissory notes are only for loans. While loans are a common use, promissory notes can also be used for other types of financial transactions that require a promise to pay a certain amount, under specific conditions, such as installment payments for goods or services.

Understanding these truths about promissory notes can help individuals and businesses manage their financial agreements more effectively, ensuring both clarity and legal security in their transactions.

When entering into an agreement that involves borrowing or lending money, it's crucial to understand the role and significance of a promissory note. This legal document not only lays the groundwork for the transaction but also serves as a binding commitment from the borrower to repay the lender under specific terms. Here are four key takeaways regarding filling out and using a promissory note form:

Understanding these key points ensures that both lenders and borrowers recognize the seriousness and legal implications of a promissory note. This document is not a mere formality but a crucial part of the lending process that protects the interests of all parties involved.

Set Up March Madness Bracket - An engaging form designed for fans to track, predict, and debate outcomes in the NCAA playoffs.

Puppy Health Record - Supports optimal pet care through detailed records of coat color and any unique markings, important for identification and registration purposes.