Fillable Promissory Note for a Car Document

Fillable Promissory Note for a Car Document

When acquiring a vehicle, the financial transactions involved can often become complex and require clear agreements between buyer and seller. This is where a Promissory Note for a Car becomes invaluable. Serving as a legally binding agreement, it outlines the buyer's promise to pay the seller a specified amount of money over a certain period. The form not only specifies the loan amount but also details interest rates, repayment schedule, and the consequences of non-payment, ensuring both parties have a clear understanding of the terms. It provides a layer of security for the seller and a structured payment plan for the buyer, minimizing misunderstandings and establishing a formal record of the transaction. Tailored to accommodate both parties' needs, this form can adapt to various scenarios, making it a crucial document in private vehicle transactions.

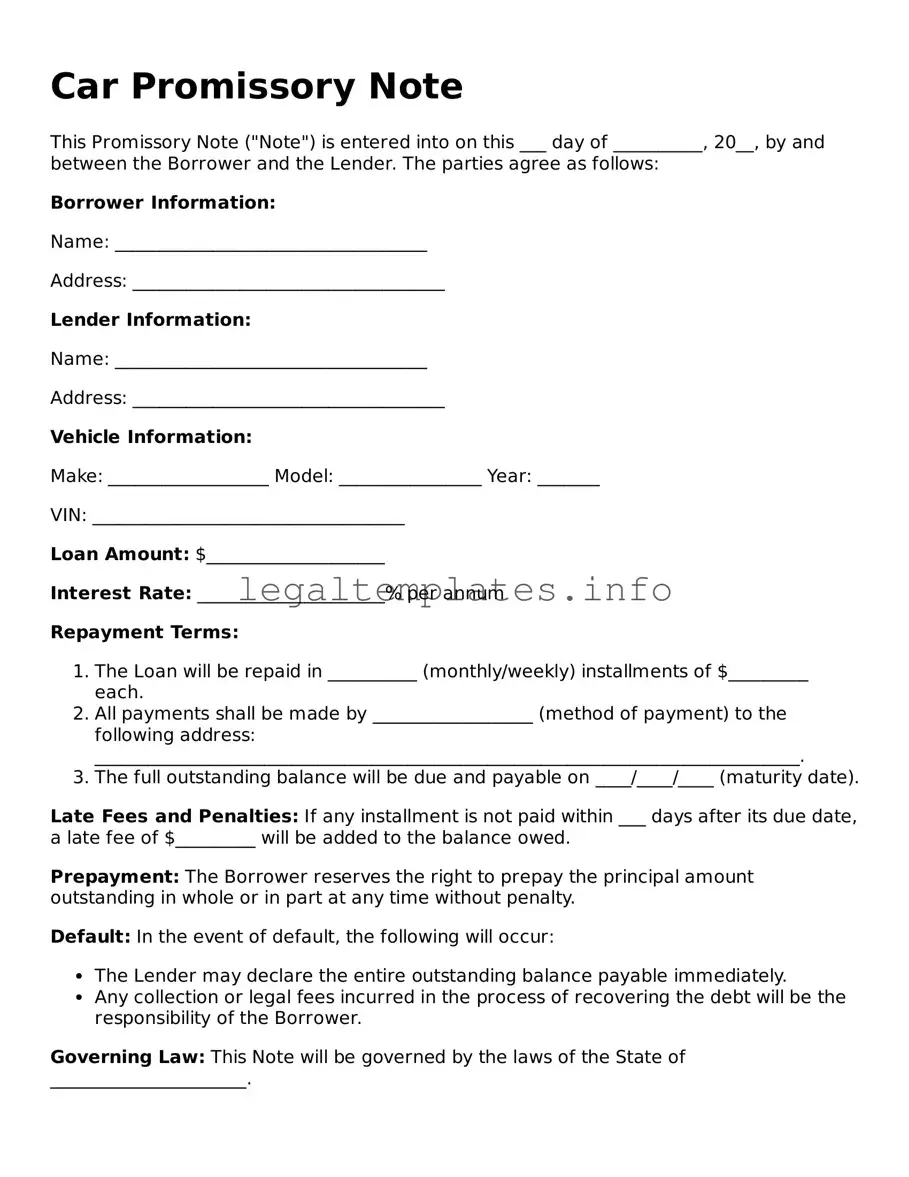

Car Promissory Note

This Promissory Note ("Note") is entered into on this ___ day of __________, 20__, by and between the Borrower and the Lender. The parties agree as follows:

Borrower Information:

Name: ___________________________________

Address: ___________________________________

Lender Information:

Name: ___________________________________

Address: ___________________________________

Vehicle Information:

Make: __________________ Model: ________________ Year: _______

VIN: ___________________________________

Loan Amount: $____________________

Interest Rate: _____________________% per annum

Repayment Terms:

Late Fees and Penalties: If any installment is not paid within ___ days after its due date, a late fee of $_________ will be added to the balance owed.

Prepayment: The Borrower reserves the right to prepay the principal amount outstanding in whole or in part at any time without penalty.

Default: In the event of default, the following will occur:

Governing Law: This Note will be governed by the laws of the State of ______________________.

Signatures: The parties hereby agree to the terms and conditions set forth in this Promissory Note:

Borrower's Signature: _______________________________ Date: ____/____/____

Lender's Signature: ________________________________ Date: ____/____/____

| Fact Number | Detail |

|---|---|

| 1 | A Promissory Note for a Car outlines the terms under which money is borrowed to purchase a vehicle. |

| 2 | It includes important details such as loan amount, interest rate, payment schedule, and default consequences. |

| 3 | The note is legally binding and holds the borrower responsible for repaying the loan under the agreed terms. |

| 4 | Different states may have specific laws governing promissory notes, affecting the document's content and enforcement. |

| 5 | Securing the loan with the car as collateral provides lenders with a form of security, allowing for repossession if payments are not made. |

When preparing to purchase a car through a private sale, using a Promissory Note can be an effective way to outline the payment agreement between the buyer and seller. This document provides a clear and legally binding contract that details the loan amount, interest rate, repayment schedule, and what occurs in the event of a default. Filling out the Promissory Note accurately is crucial for both parties to ensure that the agreement is understood and enforceable.

Here are the steps you need to follow to fill out the Promissory Note for a Car form:

After completing these steps, ensure that both parties receive a copy of the Promissory Note for their records. This form will serve as an essential record of the agreement and can help protect the interests of both the buyer and seller throughout the term of the loan.

What is a Promissory Note for a Car?

A Promissory Note for a Car is a written agreement between a seller and a buyer where the buyer promises to pay a specified amount of money over a set period to the seller for the purchase of a car. This document outlines the loan's terms, including repayment schedule, interest rate, and what happens if the buyer fails to make payments.

Do I need a Promissory Note to sell or buy a car?

While not always legally required, having a Promissory Note is strongly recommended in private car sales where the buyer intends to make payments over time. It provides a clear record of the agreement and helps protect both parties if there are any disputes or misunderstandings later on.

What should be included in a Promissory Note for a Car?

A comprehensive Promissory Note for a Car should include the full names and addresses of both the seller and the buyer, the total sale price, payment amounts and schedule, interest rate, late payment policies, and the consequences of default. It should also describe the car, including make, model, year, and VIN.

How is the interest rate determined in a Promissory Note for a Car?

The interest rate is a negotiated part of the sales agreement between the buyer and seller. It should be competitive but fair, considering current market rates and the buyer's creditworthiness. Laws in some states may cap the maximum allowable interest rate.

What happens if the buyer misses a payment?

The specific consequences of missing a payment are detailed in the Promissory Note itself. Generally, there might be a grace period followed by late fees. If missed payments continue, it could lead to default, where the seller might have the right to repossess the car or seek other forms of legal remedy.

Can the buyer pay off the Promissory Note early?

Yes, buyers are usually allowed to pay off the remaining balance of a Promissory Note early. The terms of any prepayment penalty or the absence of one should be clearly stated in the agreement.

Is a witness or notary required for a Promissory Note for a Car to be valid?

Legal requirements vary by state. While a witness or notary is not always required for the note to be valid, having the document notarized or witnessed can add a level of protection and authenticity, making it easier to enforce in court if necessary.

What should I do if I lose the original Promissory Note?

If the original Promissory Note is lost, parties should try to agree on a signed written statement that details the loss and reaffirms the obligations under the original terms. It’s also wise to check local laws or consult with a legal professional on the best steps to take.

Can modifications be made to a Promissory Note after it has been signed?

Yes, modifications can be made, but they must be agreed upon by both the buyer and seller, documented in writing, and appended to the original Promissory Note. For transparency and legal protection, any changes should be clearly detailed, agreed to by both parties, and signed.

When people fill out a Promissory Note for a car, they often overlook the importance of accuracy and detail. One common mistake is the omission of critical information, such as the full legal names of the parties involved or the vehicle identification number (VIN). This lack of detail can lead to confusion and disputes down the line, especially if questions arise about the identities of the parties or the exact vehicle being financed.

Another error is neglecting to specify the loan terms clearly. The note should detail the loan amount, interest rate, repayment schedule, and any late fees. Failure to clearly spell out these terms can result in misunderstandings, making it difficult for the lender to enforce the agreement or for the borrower to follow through with payments as intended.

Additionally, individuals often forget to include the ramifications of default within the document. It is crucial to outline what constitutes a default and the subsequent steps that will be taken, such as repossession of the car. Without this information, enforcing penalties or taking action to recover the vehicle becomes complicated.

Signatures are sometimes overlooked, which is a significant oversight. Both the lender and borrower must sign the promissory note for it to be legally binding. A promissory note without the necessary signatures holds little weight in a legal context, diminishing its enforceability.

Another area prone to error is not respecting state laws that govern promissory notes and vehicle loans. Each state has unique requirements and regulations, including those related to interest rates (usury laws) and necessary disclosures. Ignoring these laws can render a promissory note invalid or unenforceable.

Last but not least, parties often fail to keep a record of payments made towards the promissory note. This oversight can lead to disputes over how much has been paid versus how much is still owed. Keeping a detailed log of payments protects both parties and ensures transparency throughout the repayment process.

When you're in the process of buying or selling a car with a personal loan, using a Promissory Note for a Car is standard practice. This document outlines the loan details, repayment schedule, interest rate, and any collateral involved, which in this case is usually the car itself. However, to complete the transaction smoothly and ensure all legal aspects are covered, other forms and documents are often used in conjunction with the Promissory Note. Here are four of those key documents:

Together with the Promissory Note for a Car, these documents form a comprehensive package that protects the interests of both the buyer and the seller, ensuring a legal and transparent transaction. Each document serves its purpose, from establishing the terms of the loan to fulfilling legal requirements for transferring ownership and ensuring the vehicle is legally allowed on the road. Using these forms properly is essential for a smooth and lawful car buying or selling experience.

A Loan Agreement is quite similar to a Promissory Note for a Car, as it outlines the terms under which money is lent. The key difference lies in the detail and scope provided in a Loan Agreement, which elaborates on the responsibilities of each party in greater depth than the more streamlined Promissory Note. This includes specifics on repayment schedules, interest rates, and what happens in case of default.

A Mortgage Agreement also shares characteristics with a Promissory Note for a Car, especially in that both are secured forms of lending. A Mortgage Agreement is secured against real estate property, while a Promissory Note for a Car is secured against the vehicle. Both documents detail repayment terms and what occurs if the borrower defaults, highlighting the collateral involved.

A Bill of Sale for a car is closely related to a Promissory Note for a Car but serves a different purpose. The Bill of Sale proves ownership and transfer of property, while the Promissory Note secures the promise to pay for the car. Despite their differences, they are often used together in car transactions to ensure full legal coverage of the purchase and financing.

An IOU (I Owe You) document, though less formal, is related to a Promissory Note for a Car by representing an acknowledgment of debt. However, an IOU is typically a simple agreement without detailed repayment terms, interest, or collateral, making it less secure and enforceable than a Promissory Note for a Car.

A Lease Agreement, while generally used for rental properties, shares the principle of regular payments outlined in a Promissory Note for a Car. In both cases, there are explicit terms defining the payment schedule, though a Lease Agreement focuses on the use of property, while a Promissory Note is concerned with the repayment of a loan.

The Security Agreement is connected to a Promissory Note for a Car through its focus on collateral. It secures an interest in the collateral (the car) to ensure the debt is repaid. The Security Agreement complements a Promissory Note by providing legal grounding for repossession if the borrower defaults.

A Credit Card Agreement is another financial document that, like a Promissory Note for a Car, involves credit terms. This agreement outlines the terms of credit use between a cardholder and the issuer, including repayment obligations. Both types of agreements require the borrower to repay the borrowed amount under agreed-upon terms.

A Student Loan Agreement bears similarities to a Promissory Note for a Car, with both entailing the borrowing of money that must be repaid with interest. Each document specifies the amount loaned, the interest rate applied, and the repayment schedule, emphasizing the borrower's commitment to repay the borrowed funds.

An Employment Contract, though not a lending agreement, involves principles of agreement similar to those in a Promissory Note. It signifies a mutual agreement: services for compensation, with specific terms and conditions outlined. While it doesn’t revolve around a loan, it represents a formal agreement between two parties with outlined obligations.

Finally, a Personal Guaranty ties to a Promissory Note for a Car, as it involves a third party agreeing to fulfill the payment obligations if the original borrower defaults. Used alongside promissory notes to secure loans, a Personal Guaranty ensures an additional level of security for the lender, indemnicating them against possible losses.

Filling out a Promissory Note for a car involves a detailed process that requires attention to ensure that the agreement is clear, accurate, and legally binding. Here are some guidelines to follow that highlight both advisable and inadvisable practices:

When it comes to drafting a Promissory Note for a car, there are several misconceptions that can create confusion. A Promissory Note serves as a legal agreement between a borrower and lender, detailing the loan's terms for the purchase of a car. Understanding the facts can help ensure all parties are fully informed about their obligations and rights.

Dispelling these misconceptions is essential for anyone involved in a car transaction through a Promissory Note. It ensures that all parties enter the agreement with clear expectations and understanding, thereby minimizing potential conflicts and legal complications in the future.

When considering the utilization of a Promissory Note for the purchase of a car, it's imperative to understand its purpose and the implications it holds for both the borrower and the lender. This document not only formalizes the loan agreement but also serves as a legal instrument that ensures the repayment of the loan under the terms agreed upon. Here are nine key takeaways to keep in mind:

Understanding these key elements can significantly impact the effectiveness and enforcement of a Promissory Note for a Car. For both parties involved, it ensures transparency, sets clear expectations, and helps protect their respective rights should issues arise.

Release of Promissory Note Sample - It confirms the closure of the borrower’s obligation, officially terminating the promissory note’s effect.