Fillable Owner Financing Contract Document

Fillable Owner Financing Contract Document

Navigating through the maze of real estate transactions can be daunting, especially when traditional lending options do not align with the buyer's or seller's circumstances. In such cases, an Owner Financing Contract emerges as a beacon of possibility, offering an alternative route to homeownership for buyers who might not qualify for conventional bank loans. This unique arrangement allows the seller to act as the lender, providing a loan to the buyer for the purchase of the property. The form itself is pivotal, encompassing the terms of the agreement, including the purchase price, interest rate, payment schedule, and what should happen if the buyer defaults. Its complexity ensures that both parties are clear about their rights and responsibilities, laying a foundation for a financial understanding that might otherwise seem unattainable. Beyond merely a document, the Owner Financing Contract is a testament to the adaptability of real estate transactions, designed to cater to a broader spectrum of financial scenarios while securing the interests of both buyer and seller. In an economic landscape where flexibility can be just as crucial as stability, this form serves as a critical tool, empowering individuals to navigate their path to property ownership.

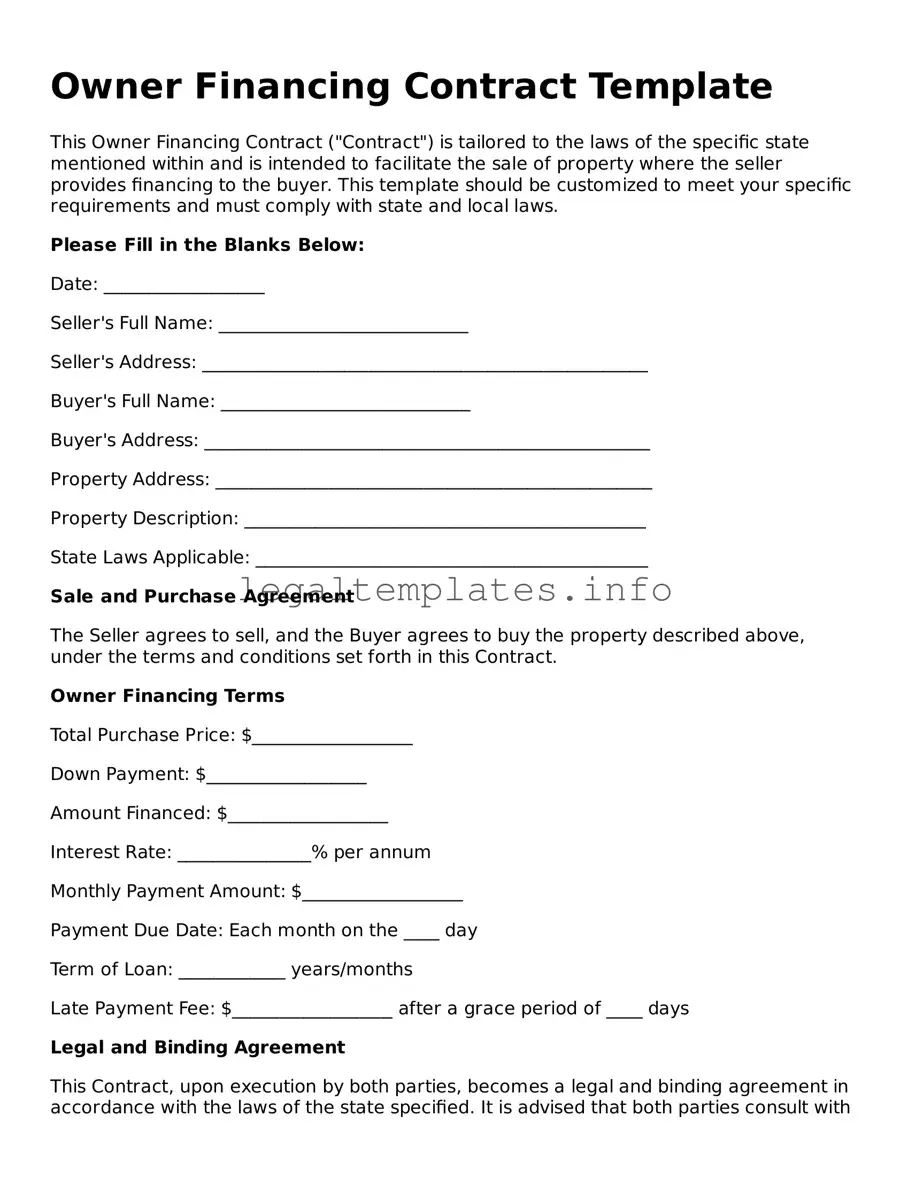

Owner Financing Contract Template

This Owner Financing Contract ("Contract") is tailored to the laws of the specific state mentioned within and is intended to facilitate the sale of property where the seller provides financing to the buyer. This template should be customized to meet your specific requirements and must comply with state and local laws.

Please Fill in the Blanks Below:

Date: __________________

Seller's Full Name: ____________________________

Seller's Address: __________________________________________________

Buyer's Full Name: ____________________________

Buyer's Address: __________________________________________________

Property Address: _________________________________________________

Property Description: _____________________________________________

State Laws Applicable: ____________________________________________

Sale and Purchase Agreement

The Seller agrees to sell, and the Buyer agrees to buy the property described above, under the terms and conditions set forth in this Contract.

Owner Financing Terms

Total Purchase Price: $__________________

Down Payment: $__________________

Amount Financed: $__________________

Interest Rate: _______________% per annum

Monthly Payment Amount: $__________________

Payment Due Date: Each month on the ____ day

Term of Loan: ____________ years/months

Late Payment Fee: $__________________ after a grace period of ____ days

Legal and Binding Agreement

This Contract, upon execution by both parties, becomes a legal and binding agreement in accordance with the laws of the state specified. It is advised that both parties consult with a legal professional before signing.

Closing and Possession Dates

Closing Date: __________________

Possession Date: __________________

Signatures

Both parties affirm that all information provided in this Contract is true and accurate to the best of their knowledge and belief. Furthermore, they agree to abide by all the terms and conditions outlined herein.

______________________ ______________________

Seller's Signature Buyer's Signature

Date: __________________ Date: __________________

Notarization (If Applicable)

This section is to be completed by a notary public if required by the laws of the state governing this Contract.

State of __________________

County of _________________

On __________________ before me, __________________________________, personally appeared _________________________________, personally known to me (or proved to me on the basis of satisfactory evidence) to be the person(s) whose name(s) is/are subscribed to the within instrument, and acknowledged that they executed the same in their authorized capacity(ies), and that by their signature(s) on the instrument, the person(s), or the entity upon behalf of which the person(s) acted, executed the instrument.

WITNESS my hand and official seal.

Signature ____________________

(Seal)

| Fact Number | Description |

|---|---|

| 1 | Owner financing contracts allow property sellers to act as the lender to the buyer. |

| 2 | These contracts can enable buyers to purchase a home without a traditional mortgage. |

| 3 | Interest rates on these contracts can be negotiated between buyer and seller, offering flexibility. |

| 4 | Payments in owner financing often result in a balloon payment at the end of the term unless refinanced. |

| 5 | The contract outlines specifics such as payment schedule, interest rate, and what happens in case of default. |

| 6 | State laws govern the creation and enforcement of owner financing contracts, making them vary widely. |

| 7 | Potential buyers typically need a down payment, which is negotiable with the seller. |

| 8 | Owner financing can provide sellers with steady income but also comes with the risk of buyer default. |

Embarking on owner financing as a path to home ownership represents a significant step for both the buyer and the seller. It bypasses traditional lending institutions, making the contract pivotal to safeguarding the interests of both parties involved. The document outlines the terms, from the purchase price to the payment schedule, ensuring clarity and legal standing. Before getting started, it's crucial to gather necessary information such as property details, loan terms, and personal identification for both buyer and seller. Completing the Owner Financing Contract diligently ensures a smooth transaction and a clear agreement on what lies ahead for both parties.

Steps to Fill Out the Owner Financing Contract Form

After completing the Owner Financing Contract form, both parties should review the document thoroughly to ensure all the information is accurate and reflects their agreement fully. Obtaining professional legal advice to review the contract before signing is advisable to guarantee that the rights and responsibilities of both the buyer and the seller are protected. Once signed, this document becomes a legally binding contract, guiding the ownership transfer process and securing the agreed-upon financial terms.

What is an Owner Financing Contract?

An Owner Financing Contract is a legal agreement where the seller of a property provides the financing to the buyer directly, instead of the buyer obtaining a loan from a bank. This contract outlines the sale's terms, including the purchase price, interest rate, payment schedule, and other conditions related to the property’s sale and purchase. It enables buyers, who might not qualify for traditional financing, to purchase a property and sellers to expedite the sale.

Why would someone use an Owner Financing Contract?

There are several reasons why both buyers and sellers might find an Owner Financing Contract appealing. For buyers, it can be a viable option if they have difficulty securing a loan from a bank due to credit issues or other financial obstacles. For sellers, offering owner financing can help attract a broader pool of potential buyers and possibly secure a faster sale. It also allows the seller to potentially earn interest on the loan provided to the buyer.

What should be included in an Owner Financing Contract?

A comprehensive Owner Financing Contract should include the full names and contact information of both buyer and seller, a detailed description of the property being sold, the sale price, down payment, interest rate, repayment schedule (including the duration of the loan and frequency of payments), and any other conditions or terms of the sale. It might also address responsibilities for property taxes, insurance, and maintenance. Legal clauses such as default terms, remedies, and rights to acceleration should be clearly stated to protect both parties.

How does an Owner Financing Contract protect both the seller and the buyer?

This contract protects the seller by including a security agreement, where the property acts as collateral for the financing. If the buyer defaults on payments, the seller can foreclose on the property to recover their investment. For the buyer, the contract guarantees the seller’s commitment to the agreed-upon terms, such as the interest rate and payment schedule, providing a clear path to homeownership without the immediate need for traditional financing.

Can an Owner Financing Contract be modified after it’s signed?

Yes, an Owner Financing Contract can be modified, but any changes require the agreement of both parties involved. Amendments should be made in writing and attached to the original agreement to ensure clarity and enforceability. This flexibility allows both buyer and seller to adjust terms if financial circumstances change, as long as both agree to the modifications.

Filling out an Owner Financing Contract form is a crucial step in the process of buying or selling property with owner financing, a method where the seller acts as the lender. One common mistake people make is not clearly identifying the property. It's essential to include all relevant details like the address, legal description, and any identifiers that uniquely describe the property. Without this information, the contract might not be enforceable or could lead to disputes about which property is subject to the sale.

Another mistake is neglecting to specify the terms of the loan. This should include the loan amount, interest rate, repayment schedule, and maturity date. Failing to detail these terms can lead to misunderstandings or disagreements in the future. Both the buyer and seller should have a clear understanding of their financial obligations and rights under the contract.

Often, individuals overlook the importance of outlining the responsibilities for property taxes, insurance, and maintenance. It's vital to establish who will be responsible for these costs. Without clearly stating these responsibilities, there can be confusion and potential legal issues if one party assumes the other is handling these important financial obligations.

Not specifying what constitutes a default under the contract is a critical error as well. The contract should clearly state what actions or failures to act will be considered a default, and what the consequences will be. This might include late payments, failure to maintain property insurance, or other breaches of the contract. Clear default terms ensure that both parties understand the seriousness of the obligations undertaken.

Finally, a significant mistake is not having the contract reviewed by a legal professional. While it might seem like a straightforward process, owner financing is a complex legal arrangement. A legal professional can help identify potential issues, ensure the contract complies with state laws, and protect the interests of both parties. Skipping this step can lead to problems down the line, including the contract being declared invalid or unenforceable.

When engaging in an owner financing agreement, parties use various forms and documents to ensure the transaction is accurately recorded and legally binding. An Owner Financing Contract is a pivotal document that outlines the sale of a property under terms directly negotiated between the buyer and seller, eliminating financial institutions from the process. To complement this contract, other essential documents provide additional legal protections, clarify terms and conditions, and comply with local and federal regulations. Below is a description of up to nine forms and documents frequently used alongside an Owner Financing Contract.

In conclusion, while the Owner Financing Contract is the cornerstone of any owner-financed transaction, the accompanying documents play vital roles in ensuring the process is transparent, fair, and legally sound. They protect the interests of all parties involved, provide clear expectations for the repayment plan, and help navigate the complexities of real estate transactions without traditional financing. Parties entering into such agreements should consider consulting with legal and financial professionals to ensure all documents are correctly executed and filed.

The Owner Financing Contract form shares similarities with a Mortgage Agreement in several key ways. Both documents outline the terms under which financing is provided for the purchase of real estate. They detail the loan amount, interest rate, repayment schedule, and the consequences of default. The main difference lies in the lender's identity: a financial institution in the case of a Mortgage Agreement, versus the property seller with an Owner Financing Contract.

Another document akin to the Owner Financing Contract is the Land Contract. Both serve as alternatives to traditional financing for the purchase of property. A Land Contract, like an Owner Financing Contract, involves payments made directly to the seller over time. However, the buyer typically does not receive the title to the property until the full purchase price has been paid. This key distinction affects the buyer's rights to the property during the term of the agreement.

A Promissory Note also bears resemblance to an Owner Financing Contract but is generally simpler. It's a promise to pay a specified sum to a specified person within a set timeframe, including details like interest and repayment terms. While a Promissory Note can be used in owner financing transactions, it doesn't include many of the protections or detailed obligations about the property itself found in an Owner Financing Contract, such as insurance requirements or maintenance obligations.

The Deed of Trust is another document related to the Owner Financing Contract. It is used in some states in place of a traditional mortgage. In both cases, the title to the property is held in trust until the loan is fully repaid. However, with a Deed of Trust, a third party—the trustee—holds the actual title to the property, whereas with owner financing, the seller may retain legal title until the debt is satisfied, depending on the specific terms of the contract.

Lastly, the Lease Agreement with Option to Purchase shares elements with the Owner Financing Contract but caters to a different need. This document allows a tenant the option—or the right, under certain conditions—to buy the property they are renting. It differs fundamentally in that it first establishes a landlord-tenant relationship, providing the tenant an option to purchase at a later date rather than creating an immediate buyer-seller relationship with a path to ownership through financing directly from the seller.

Filling out an Owner Financing Contract requires careful attention to detail and precision. Adhering to a set of do's and don'ts can guide you through the process smoothly, ensuring both parties enter into a fair and legally-binding agreement. Below are key practices to follow and pitfalls to avoid.

Do's:When people think about owner financing contracts, several misconceptions often arise. Understanding these common misunderstandings can help both buyers and sellers navigate the process of owner financing with more clarity and confidence.

Owner financing is only for buyers with bad credit. Many believe that the only time a buyer opts for owner financing is when they have poor credit. However, this isn't always the case. Some buyers choose owner financing to avoid traditional lending delays, to negotiate more flexible terms, or because they plan to make significant improvements to the property before obtaining a conventional loan.

Owner financing contracts are not legally binding. This misconception could lead to a lot of confusion and potential legal issues. Owner financing contracts, when properly executed, are fully enforceable legal agreements. They should outline all terms of the sale, including payment schedule, interest rate, and consequences of default, just like any other mortgage agreement.

The seller always benefits more than the buyer in owner financing. The benefits of owner financing can actually go both ways. Sellers get a steady income stream and can potentially sell their property faster. Buyers may benefit from more flexible qualifying criteria and quicker closing times. The situation and terms agreed upon dictate who benefits more.

There are no closing costs in owner financing. While closing costs in an owner-financed deal might be lower than with a traditional mortgage, they do not disappear. Both parties might still need to pay for appraisals, legal fees, and property inspections. These costs should be negotiated and spelled out in the contract.

Owner financing doesn't require a down payment. Many people think that owner financing means you can skip the down payment. However, most sellers will require one to secure the deal, protect their investment, and ensure the buyer is committed. The amount is negotiable but is typically similar to or lower than traditional bank requirements.

Understanding these misconceptions can help parties involved in an owner financing agreement make informed decisions. Like any real estate transaction, proper legal advice and thorough documentation are key to a successful and mutually beneficial arrangement.

Understanding the nuances of an Owner Financing Contract can significantly impact both the buyer and seller's financial and legal standing. Here, key takeaways have been identified to help navigate the complexities of filling out and using the Owner Financing Contract form efficiently.

Owner financing can offer unique advantages to both buyers and sellers, such as flexibility in financing and potential tax benefits. However, entering into an Owner Financing Contract requires careful consideration and attention to detail. By keeping these key takeaways in mind, parties can better navigate the process, leading to a successful and mutually beneficial transaction.

Purchase Agreement Addendum - Allows for the extension of closing dates, adjustments in purchase price, or repair agreements post-inspection.

How to Fire a Realtor Example Letter - An efficient way to handle the formal ending of a property purchase, respecting the terms outlined in the initial agreement.